13/07/2022

When navigating the world of car insurance in the UK, you'll typically encounter three main tiers of cover: Third Party Only, Third Party, Fire and Theft, and Fully Comprehensive. While many drivers opt for the cheapest (Third Party Only) or the most extensive (Fully Comprehensive), the middle ground of Third Party, Fire and Theft (TPFT) often gets overlooked. But is this mid-tier policy a sensible choice for your automotive protection? Let's delve into what TPFT insurance entails and whether it aligns with your needs.

Understanding Third Party, Fire and Theft (TPFT) Cover

Third Party, Fire and Theft insurance acts as a middle-ground option, offering more protection than basic Third Party Only cover, but less than a Fully Comprehensive policy. So, what exactly does it shield you against?

What's Included in a TPFT Policy?

A TPFT policy typically covers the following:

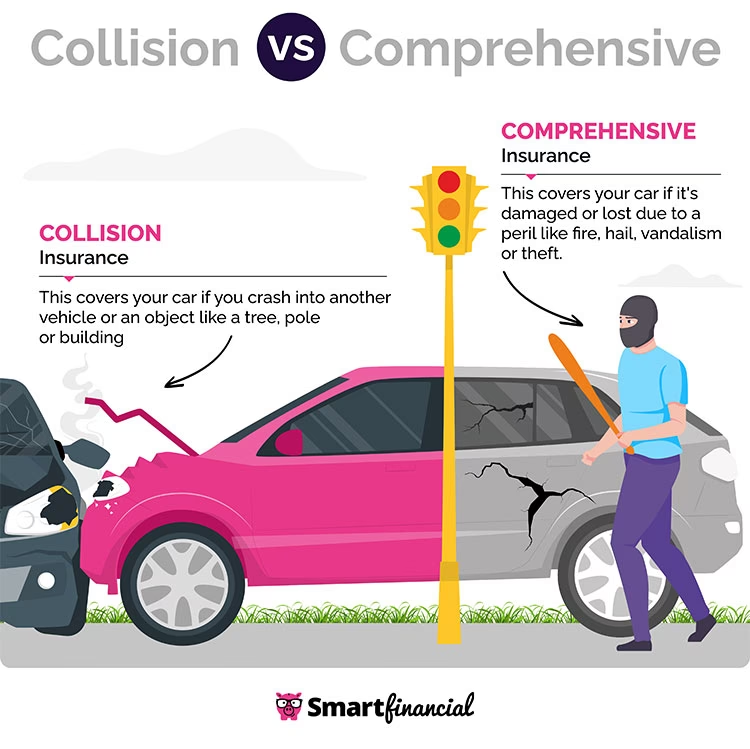

- Third-Party Liability: This is the legally mandated cover in the UK. It protects you financially if you cause injury or damage to another person, their vehicle, or their property during an accident. Your insurer will cover the costs of their repairs or medical expenses, up to a certain limit.

- Fire Damage: If your car is damaged or destroyed by fire, a TPFT policy will help cover the costs of repair or replacement. This includes fires originating within the vehicle or those caused by external sources impacting your car.

- Theft: If your car is stolen, this policy will compensate you for its loss. The payout will be based on the vehicle's value as stated in your policy.

What's Not Covered by TPFT?

It's crucial to understand the limitations of TPFT cover. It generally does not cover:

- Damage to Your Own Car (if you're at fault): If you cause an accident and damage your own vehicle, TPFT will not pay for the repairs. This is a significant difference compared to Fully Comprehensive insurance.

- Vandalism: Damage caused by vandalism is typically not covered unless it's directly linked to an attempted theft.

- Accidental Damage (not fire or theft): Any other accidental damage to your vehicle, such as damage from a collision you caused, falling objects, or weather events, will not be covered.

- Mechanical Breakdowns: Engine failure or other mechanical issues are usually excluded.

- Wear and Tear: Damage resulting from the natural ageing process of the vehicle is not covered.

- Personal Belongings: Items stolen from within your car are generally not covered under a standard TPFT policy.

- Catalytic Converter Theft: While attempted theft might be covered, the actual replacement of a stolen catalytic converter is often excluded and may require a specialist policy.

Is TPFT Right for You?

The decision to opt for TPFT insurance depends on several factors:

Factors to Consider:

- Vehicle Age and Value: TPFT is often a good choice for older or lower-value vehicles. If your car is not worth a significant amount, the cost of Fully Comprehensive insurance might outweigh the benefits.

- Your Driving Habits and Location: If you live in an area with a high rate of car theft or arson, the fire and theft protection offered by TPFT can provide valuable peace of mind.

- Your Financial Situation: If you have savings that could cover minor accidental damage to your own car, TPFT might be a more cost-effective option. However, if you'd struggle to afford major repairs or a replacement vehicle, more comprehensive cover might be advisable.

- Outstanding Finance: If you have a car loan, your finance provider may insist on Fully Comprehensive cover until the loan is repaid.

When Might You Consider Dropping TPFT?

- When the Premium Exceeds the Car's Value: If the annual cost of your TPFT insurance is more than the market value of your car, it's probably not financially sensible.

- When You Have Substantial Savings: If you have a significant emergency fund that could comfortably cover the cost of repairing or replacing your vehicle in the event of fire or theft, you might consider reducing your cover.

- When Your Risk Profile Changes: If you move to an area with a much lower crime rate or your car becomes significantly older and less desirable to thieves, you might re-evaluate your need for TPFT.

Comparing TPFT with Other Policies

TPFT vs. Third Party Only

The primary difference is the added protection for fire and theft that TPFT offers. Third Party Only only covers damage you cause to others. TPFT, therefore, provides a greater level of security for your own vehicle against these specific perils, usually at a slightly higher premium.

TPFT vs. Fully Comprehensive

Fully Comprehensive insurance is the most extensive. It covers everything TPFT does, plus accidental damage to your own vehicle, regardless of fault, as well as often including extras like windscreen cover, breakdown assistance, and personal belongings cover. Consequently, Fully Comprehensive policies are typically the most expensive.

| Feature | Third Party Only | Third Party, Fire & Theft | Fully Comprehensive |

|---|---|---|---|

| Damage to others' property/vehicles | ✅ | ✅ | ✅ |

| Injury to third parties | ✅ | ✅ | ✅ |

| Fire damage to your car | ❌ | ✅ | ✅ |

| Theft of your car | ❌ | ✅ | ✅ |

| Accidental damage to your car (your fault) | ❌ | ❌ | ✅ |

| Accidental damage to your car (other's fault) | ❌ (claim against other driver) | ❌ (claim against other driver) | ✅ |

| Windscreen Cover | Usually ❌ | Often ❌ (or optional) | Often ✅ (or optional) |

| Typical Cost | Lowest | Mid-range | Highest |

Getting a Quote for TPFT

To find the best TPFT policy for your needs, follow these steps:

- Research Providers: Look for reputable insurance companies with good customer reviews.

- Gather Information: Have your vehicle details (make, model, age, condition), driving history, and personal information ready.

- Get Multiple Quotes: Contact several insurers, either online, by phone, or in person.

- Compare Policies: Carefully analyse the coverage, exclusions, excesses, and premiums offered by each insurer.

- Purchase Your Policy: Once you've found the right fit, complete the application process.

Frequently Asked Questions

Does TPFT cover rental cars?

Yes, TPFT policies often cover rental cars for a limited period (typically up to 21 days) while your own vehicle is being repaired due to fire or theft. However, it's essential to check the specific terms and conditions of your policy and the rental agreement.

Does TPFT cover engine failure?

No, TPFT insurance generally does not cover mechanical breakdowns or engine failure. This type of issue is usually covered by a separate mechanical breakdown insurance policy or, in some cases, by a warranty.

Does TPFT cover windshield damage?

While TPFT policies might offer some limited coverage for windshield damage if it's a direct result of a fire or attempted theft, it's not guaranteed. Comprehensive policies are more likely to include specific benefits for windscreen repairs or replacements.

Is TPFT necessary?

TPFT is not legally required in the UK, but it can be a prudent choice depending on your circumstances. If your car is older, you live in a high-risk area for theft or fire, or you want more protection than Third Party Only without the full cost of comprehensive cover, then it could be a valuable option.

Is TPFT worth the price?

For many drivers, TPFT offers a good balance of protection and cost. It provides peace of mind against two significant risks – fire and theft – for your own vehicle, which basic Third Party Only cover lacks. Whether it's 'worth the price' is subjective and depends on your individual risk assessment and budget.

Ultimately, understanding the nuances of Third Party, Fire and Theft insurance is key to making an informed decision about protecting your vehicle. Always read your policy documents carefully to ensure you have the cover that best suits your needs.

If you want to read more articles similar to Third Party, Fire and Theft Insurance: Is It Worth It?, you can visit the Insurance category.