21/04/2015

Imagine the scenario: you've been involved in an accident, perhaps a minor bump or something more significant, and now you're awaiting the verdict from your insurance company. Then comes the call, and the words 'your car is a write-off' echo in your ears. For many motorists, these words can be confusing, even alarming. What exactly does it mean for your beloved vehicle to be declared a 'write-off', and what are the immediate and long-term consequences for you as the owner? In the UK, understanding car write-offs is crucial, not only for navigating the immediate aftermath of an incident but also for making informed decisions about buying or selling a vehicle that may have been previously damaged.

At its core, a car write-off, officially known as a 'total loss', occurs when an insurance company decides that the cost of repairing a damaged vehicle outweighs its market value, or if the vehicle is deemed unsafe to repair. It's not necessarily about the severity of the damage alone, but rather an economic decision based on a complex calculation involving repair costs, salvage value, and the car's pre-accident market worth. This guide aims to demystify the process, explain the different categories of write-offs in the UK, and provide you with the essential knowledge needed to navigate this often-complex aspect of car ownership.

- What Exactly is a Car Write-Off?

- The UK's Write-Off Categories: A Detailed Look

- Why Do Insurers Write Off Cars?

- What Happens After Your Car is Written Off?

- Buying a Written-Off Car: Proceed with Caution

- Selling a Written-Off Car

- Re-registering and Insuring a Written-Off Vehicle (Cat S & N)

- Frequently Asked Questions About Car Write-Offs

- Conclusion

What Exactly is a Car Write-Off?

When an insurer declares a car a 'write-off', it means the vehicle is considered a total loss. This decision is primarily driven by economics. The insurer calculates the estimated cost of repairs, including parts, labour, and any associated expenses like courtesy cars or recovery. They then compare this figure to the car's market value just before the incident. If the repair cost exceeds a certain percentage (often 50-70%, though this varies by insurer and policy) of the car's market value, or if the car is deemed irreparable or unsafe, it will be written off. This doesn't always mean the car is completely destroyed; sometimes, seemingly minor damage can lead to a write-off if the parts are expensive or the repair process is intricate.

The overarching goal for the insurer is to limit their financial exposure. Rather than paying a substantial sum for repairs that might approach or even exceed the car's worth, they opt to pay out the vehicle's pre-accident market value to the policyholder, taking ownership of the damaged vehicle themselves. This process ensures that the insurer manages costs effectively, and the policyholder receives compensation based on the car's value.

The UK's Write-Off Categories: A Detailed Look

In the UK, write-offs are classified into specific categories by the Association of British Insurers (ABI) to indicate the extent of the damage and whether the vehicle can return to the road. These categories were updated in October 2017, replacing the older Category C and D with Category S and N. It's vital to understand these classifications as they dictate the car's future and potential legality on the road.

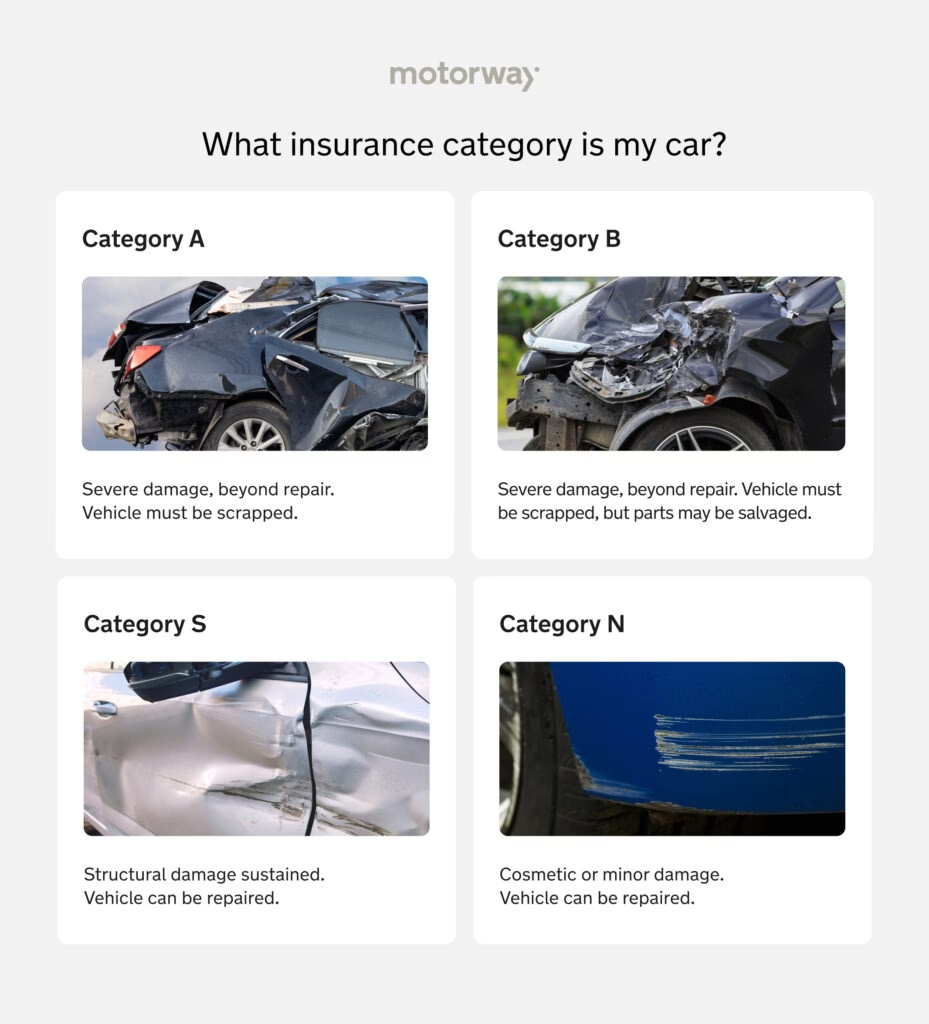

Category A: Scrap

Category A is the most severe classification. These vehicles are deemed to be so severely damaged that they are beyond repair, and there are no salvageable parts. They pose a significant safety risk and must be crushed, with no parts allowed to be removed or sold, other than scrap metal. These cars are never allowed back on the road, and their Vehicle Registration Document (V5C) will be cancelled.

Category B: Break

Vehicles in Category B are also extensively damaged and cannot be repaired to a roadworthy condition. However, unlike Category A, some parts from a Cat B vehicle can be safely removed and salvaged for use in other vehicles. The chassis and body shell must be crushed, ensuring the vehicle itself never returns to the road. The V5C will be cancelled, and the car effectively ceases to exist as a whole vehicle.

Category S: Structurally Damaged Repairable

This category, introduced in 2017, replaced the old Category C. A Cat S vehicle has suffered significant structural damage, meaning the vehicle's chassis or other load-bearing components have been affected. While it is repairable, the repairs must address these structural issues. Once professionally repaired to a safe standard, a Cat S vehicle can legally return to the road. However, the Cat S marker will remain permanently on its HPI check and V5C document, indicating its history. It's crucial that any structural repairs are carried out by qualified professionals.

Category N: Non-Structurally Damaged Repairable

Also introduced in 2017, Cat N replaced the old Category D. A Cat N vehicle has suffered non-structural damage, which could include cosmetic damage (e.g., dents, scratches), mechanical faults, or damage to electrical components. While the damage is not to the vehicle's structural frame, it is still deemed uneconomical for the insurer to repair. Like Cat S, a Cat N car can be repaired and returned to the road, but the Cat N marker will remain on its history. These vehicles typically require less complex repairs than Cat S cars, but all necessary work must still be completed to ensure roadworthiness.

Here's a quick comparison of the categories:

| Category | Damage Type | Repairable? | Can return to road? | Parts Salvageable? |

|---|---|---|---|---|

| A (Scrap) | Severe, beyond repair | No | Never | No |

| B (Break) | Extensive, beyond repair | No (vehicle) | Never | Yes (parts) |

| S (Structural) | Significant structural | Yes (professionally) | Yes | N/A (whole vehicle) |

| N (Non-Structural) | Non-structural, cosmetic/mechanical | Yes | Yes | N/A (whole vehicle) |

Why Do Insurers Write Off Cars?

The decision to write off a car isn't arbitrary; it's a carefully calculated one based on several factors, primarily financial. The main reasons include:

- Economic Viability: As mentioned, if the cost of repairs (parts, labour, paint, specialist equipment) plus the salvage value of the damaged vehicle approaches or exceeds the car's pre-accident market value, it becomes uneconomical to repair. Insurers operate on profit margins, and spending more on repairs than the car is worth doesn't make financial sense.

- Safety Concerns: Even if repairs seem economically viable, a vehicle might be written off if the damage is so severe that it compromises the car's inherent safety features, such as crumple zones, airbags, or chassis integrity, to an extent that it cannot be guaranteed to be safe post-repair.

- Complexity of Repair: Some damage, while not structurally total, might be incredibly complex or time-consuming to fix, requiring highly specialised skills or equipment, making it economically unfeasible.

- Age and Condition: Older vehicles or those with high mileage will have a lower market value. Consequently, even relatively minor damage can lead to a write-off simply because the repair cost quickly outstrips the car's depreciated worth.

What Happens After Your Car is Written Off?

Once your insurer declares your car a write-off, several steps typically follow:

- Valuation and Payout: The insurer will assess the pre-accident market value of your vehicle. This isn't necessarily what you paid for it, but what a similar car would have sold for just before the incident. They will then offer you a settlement based on this valuation, minus any excess you need to pay.

- Vehicle Ownership Transfer: Unless you opt to retain the vehicle (which is usually only an option for Cat S or N vehicles and comes with conditions), the insurer takes legal ownership of the written-off car. They will then typically sell it to a salvage company.

- V5C (Logbook) Update: If your car is a Cat A or B write-off, your V5C will be cancelled, and the car will never return to the road. For Cat S or N write-offs, the V5C will be updated to reflect the write-off status. You will need to send the V5C to your insurer, who will then forward it to the DVLA, or you may need to update the DVLA yourself if you retain the vehicle.

Buying a Written-Off Car: Proceed with Caution

While the idea of buying a Cat S or Cat N car might seem appealing due to the significantly lower purchase price, it comes with a unique set of considerations and potential pitfalls. These vehicles are often available from salvage auctions or specialist dealers.

Pros:

- Lower Price: This is the primary attraction. A written-off car can be considerably cheaper than a comparable non-written-off model, potentially allowing you to afford a newer or higher-spec vehicle.

- Potential for Good Value: If the repairs were carried out professionally and the damage was truly minor (especially for Cat N), you could end up with a perfectly functional car at a bargain price.

Cons:

- Hidden Damage: The most significant risk. While a vehicle might look fine on the surface, there could be underlying damage not properly repaired, leading to future mechanical issues or safety concerns.

- Insurance Challenges: Insuring a written-off car can be more difficult and expensive. Some insurers may refuse to cover them, or they might charge higher premiums due to the perceived increased risk. Getting comprehensive cover might be particularly challenging.

- Resale Value: When it comes to selling, the write-off marker will always affect the car's value. Buyers are often wary of written-off vehicles, and you will likely achieve a much lower price than for a non-written-off equivalent, regardless of how well it's been repaired.

- Finance Issues: Many lenders are reluctant to offer finance on written-off vehicles due to the reduced asset value and increased risk.

- Warranty Voids: Manufacturer warranties are often voided once a car is declared a write-off, even if it's subsequently repaired.

If you're considering buying a written-off vehicle, it is absolutely essential to:

- Get a full HPI check to confirm its write-off status and history.

- Have the car thoroughly inspected by an independent, qualified mechanic who specialises in accident repair, before purchase. They can identify any lingering issues or substandard repairs.

- Ask for photographic evidence of the damage before repair, and documentation of all repairs carried out.

Selling a Written-Off Car

If you decide to sell a car that was previously written off (Cat S or N), you are legally obliged to disclose its history to any potential buyer. Failure to do so could lead to legal action against you for misrepresentation. Transparency is key, even if it means accepting a lower offer. Be prepared to answer questions about the damage and repairs, and have all relevant documentation ready.

Re-registering and Insuring a Written-Off Vehicle (Cat S & N)

For Cat S and N vehicles, once repaired, they can return to the road. However, there are specific requirements in the UK:

- Cat S Vehicles: Although the old VIC (Vehicle Identity Check) check was abolished, for Cat S vehicles, you must ensure that all structural repairs have been carried out to a professional standard. While no specific DVLA inspection is required, it is strongly advised to have an independent inspection to verify the quality and safety of the repairs before driving. The V5C will be updated with the Cat S marker.

- Cat N Vehicles: These do not require a specific DVLA inspection before returning to the road. However, you are still responsible for ensuring all repairs make the vehicle roadworthy. The V5C will be updated with the Cat N marker.

Regardless of the category, once repaired, you must notify the DVLA and ensure your V5C (logbook) is updated with the write-off category. This marker will remain permanently on the vehicle's record.

When it comes to insuring a previously written-off car, be prepared for challenges. Many insurers will ask about a car's write-off history during the quotation process. Some may decline to offer cover, particularly comprehensive policies, while others may offer cover but at a higher premium. It's crucial to be honest about the vehicle's history to avoid invalidating your policy. Shopping around and using specialist brokers who deal with written-off vehicles might be necessary.

Frequently Asked Questions About Car Write-Offs

Q: Can I keep my car if it's written off?

A: If your car is a Cat A or B, no, you cannot keep it; the insurer takes ownership for crushing. If it's a Cat S or N, you might be able to buy it back from your insurer, but the settlement payout will be reduced by the car's salvage value. You'll then be responsible for all repairs and ensuring it's roadworthy.

Q: Is it safe to drive a Cat S or Cat N car?

A: Potentially, yes, but only if it has been repaired to a professional, safe, and roadworthy standard. The 'Cat S' and 'Cat N' classifications simply mean it was uneconomical for the insurer to repair, not necessarily that it's inherently unsafe if fixed correctly. Always have an independent inspection.

Q: Does a write-off affect my insurance premiums in the future?

A: Yes, if you were at fault for the accident, it will likely affect your future premiums and potentially your no-claims bonus. If you buy a previously written-off car, insuring it can be more expensive or difficult, regardless of fault, due to the vehicle's history.

Q: How is the value of my written-off car determined?

A: The insurer will assess the pre-accident market value of your vehicle. This is what a car of the same make, model, age, mileage, and condition would typically sell for on the open market just before the incident. They use various databases and market comparables for this.

Q: What if I don't agree with the insurer's valuation?

A: You have the right to challenge their valuation if you believe it's too low. Gather evidence of comparable vehicles for sale in your area, highlighting their prices, mileage, and condition. Present this to your insurer. If you still can't agree, you can escalate the complaint through their internal complaints procedure and, if necessary, to the Financial Ombudsman Service (FOS).

Conclusion

Understanding car write-offs is an essential part of being a responsible car owner in the UK. Whether you've been in an accident and your vehicle is declared a total loss, or you're considering buying a car with a write-off history, knowing the categories (A, B, S, N) and their implications is paramount. While a written-off car might offer a tempting price point, the long-term considerations regarding safety, insurance, and future resale value should never be overlooked. Always prioritise thorough checks and professional advice to ensure you're making a decision that's both economically sound and, most importantly, safe for the road.

If you want to read more articles similar to Car Write-Offs: The UK Driver's Essential Guide, you can visit the Insurance category.