18/07/2007

For businesses operating in the United Kingdom, understanding Value Added Tax (VAT) is not just a matter of compliance, it's fundamental to financial health. If your business is registered for VAT, you are legally obliged to charge VAT on the taxable supplies you make. The complexities arise when determining what exactly qualifies as taxable, at what rate, and under which specific circumstances. This guide aims to demystify the intricacies of the UK VAT system, drawing on the comprehensive framework provided by HMRC.

While there isn't a single, definitive 'VAT list' in the sense of a simple checklist, HMRC provides extensive guidance on the VAT rates applicable to a vast array of goods and services. This guidance acts as your essential reference, outlining the standard, reduced, and zero rates, as well as categories that are exempt or entirely outside the scope of the UK VAT system. Navigating this landscape correctly is crucial for every business, from sole traders to large corporations.

- Understanding UK VAT Rates and Their Application

- Sector-Specific VAT Rules and Rates

- International Trade

- Food and Drink, Animals, Animal Feed, Plants and Seeds

- Sport, Leisure, Culture and Antiques

- Health, Education, Welfare and Charities

- Power, Utilities, Energy and Energy Saving, Heating

- Building and Construction, Land and Property

- Transport, Freight, Travel and Vehicles

- Printing, Postage, Publications – Books, Magazines and Newspapers

- Other Categories

- Key VAT Rates at a Glance

- Frequently Asked Questions About UK VAT

- What is the difference between 'exempt' and 'zero-rated' supplies?

- Why are some food items zero-rated but hot takeaways or restaurant meals standard-rated?

- Do charities always avoid VAT on their purchases or sales?

- Can I reclaim VAT on international shipping costs?

- Are all energy-saving material installations eligible for the reduced rate?

- Conclusion

Understanding UK VAT Rates and Their Application

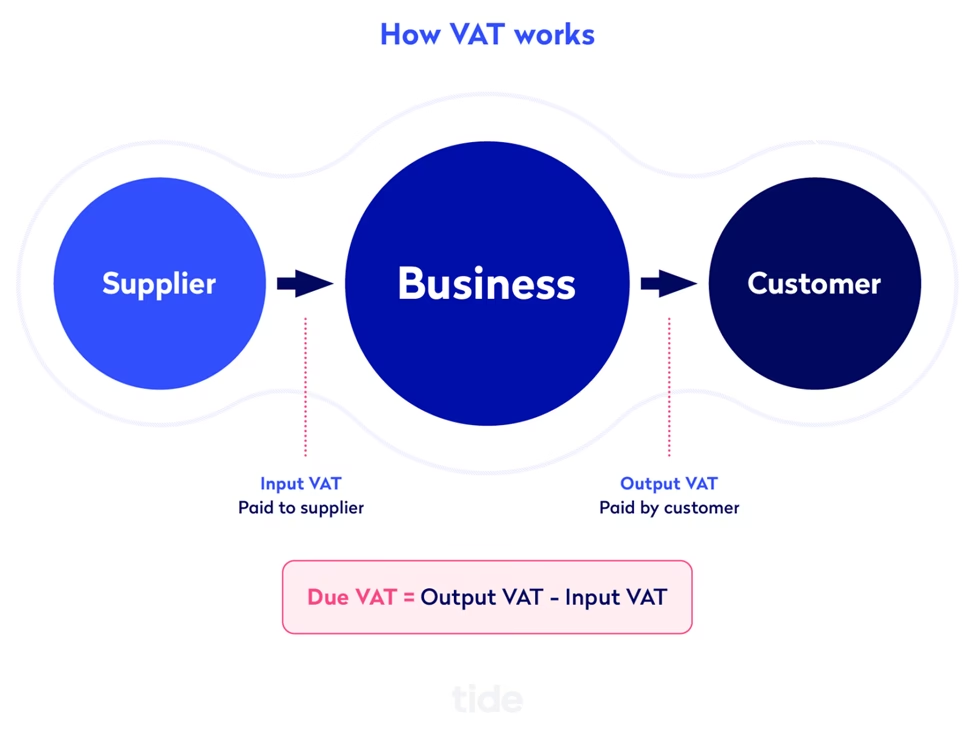

VAT is a consumption tax, meaning it's ultimately paid by the end consumer, but collected by businesses on behalf of the government. The rate you charge is not arbitrary; it depends entirely on the nature of the goods or services you provide. Generally, most goods and services in the UK are subject to the standard rate of VAT. However, many items qualify for a reduced rate, a zero rate, or are entirely exempt from VAT, while others fall outside its scope altogether.

No VAT is charged on goods or services that are either exempt from VAT or are considered to be outside the scope of the UK VAT system. It’s important to distinguish between these two classifications, as they have different implications for your VAT accounting and ability to reclaim input VAT.

Crucial Conditions for VAT Application

The application of a specific VAT rate is rarely straightforward and often hinges on a range of conditions. These conditions are vital and must be meticulously met for the correct rate to apply. Businesses must pay close attention to:

- Who’s providing or buying them: The nature of the supplier or customer can influence the VAT rate. For instance, supplies to charities might sometimes be treated differently.

- Where they’re provided: The geographical location of the supply, especially in international trade, significantly impacts VAT rules.

- How they’re presented for sale: The packaging, bundling, or marketing of a product can sometimes alter its VAT treatment.

- The precise nature of the goods or services: A nuanced understanding of what you are selling is paramount. A 'food item' might be zero-rated, but if it's 'hot food for consumption on premises,' it becomes standard-rated.

- Whether you obtain the necessary evidence: Proper documentation, such as export evidence for zero-rated goods, is critical.

- Whether you keep the right records: Maintaining accurate and comprehensive VAT records is non-negotiable for compliance.

- Whether they’re provided with other goods and services: Bundled supplies can have complex VAT implications, often requiring apportionment or a dominant supply rule.

It is worth noting that other, more specific conditions may also apply, depending on the particular industry or transaction. Certain trades, such as builders and charities, also have specific VAT rules that affect how they account for VAT, how much they must pay, and how much they can reclaim. Ensuring compliance with these detailed regulations is paramount to avoid penalties.

Sector-Specific VAT Rules and Rates

The UK VAT system categorises goods and services into broad areas, each with its own set of rules. Understanding these categories is key to applying the correct VAT rate.

International Trade

For businesses engaged in international trade, goods exported outside the UK are generally zero-rated, provided certain conditions are met. This applies to goods sent overseas, requiring businesses to maintain robust evidence of export to justify the zero-rating.

Food and Drink, Animals, Animal Feed, Plants and Seeds

This category holds some of the most intricate VAT rules. Food and drink for human consumption are typically zero-rated. However, there are significant exceptions that are always standard-rated:

- Catering services

- Alcoholic drinks

- Confectionery

- Crisps and savoury snacks

- Hot food

- Sports drinks

- Hot takeaways

- Ice cream

- Soft drinks and mineral water

Restaurants, for example, must always charge VAT on everything consumed on their premises or in designated communal areas. For takeaways, hot food and home deliveries are standard-rated, but cold takeaway food (unless consumed in a designated area) is not subject to VAT. It's also worth remembering the temporary reduced rate of 5% that applied to certain catering and hot takeaway food supplies from 15 July 2020 to 31 March 2021, a measure introduced to support the hospitality sector during challenging times.

Certain animals, animal feeding products, plants, and seeds can also qualify for the zero rate, subject to specific conditions outlined in relevant VAT notices. However, products packaged explicitly as pet food are standard-rated, highlighting the precise nature rule.

Sport, Leisure, Culture and Antiques

Services within this domain often qualify for VAT exemption. Physical education and sports activities, as detailed in VAT Notice 701/45, are exempt. Similarly, admission charges by public authorities or eligible cultural bodies to certain cultural events – such as visits to museums, art exhibitions, zoos, and performances – are also exempt under VAT Notice 701/47. Antiques, works of art, or similar items, when sold by private treaty to public collections or used to settle tax debts with HMRC, are also exempt, as outlined in VAT Notice 701/12.

Health, Education, Welfare and Charities

These sectors frequently benefit from VAT exemptions due to their public benefit nature. Education and vocational training provided by an eligible body (excluding 'private schools' in certain contexts), along with goods or services closely connected to that education, are exempt under VAT Notice 701/30. While specific details for welfare and charities weren't provided, it's understood that these sectors have particular VAT treatments, often involving exemptions or reliefs for certain activities.

Power, Utilities, Energy and Energy Saving, Heating

This category features a mix of reduced and zero rates, particularly for domestic use. Electricity, gas, heating oil, and solid fuel for domestic and residential use, or for non-business use by a charity, are subject to the 5% reduced rate. In contrast, fuel for business use is typically standard-rated (VAT Notice 701/19). For utilities, emptying domestic cesspools, septic tanks, or similar, and sewerage services supplied to domestic or industrial customers, are zero-rated. Water supplied to households is also zero-rated, while water supplied to industrial customers is standard-rated (VAT Notice 701/16).

Energy-saving materials installed in dwellings and buildings used for a relevant residential purpose can also qualify for the reduced rate. Eligibility often depends on the age or benefit status of the recipient (e.g., over 60 or receiving certain benefits as per VAT Notice 708/6), or on the cost proportion of the materials versus installation.

Building and Construction, Land and Property

This sector sees a mix of rates depending on the specific supply. Garages or parking spaces let together with dwellings under shorthold tenancy agreements for permanent residential use are exempt. Similarly, the grant or licence to occupy land on which incidental parking takes place, and the grant or licence to occupy land or buildings generally, are exempt (VAT Notice 742). The sale or long lease of a new dwelling with a garage or parking space is zero-rated (VAT Notice 708), distinguishing it from standard-rated garages or facilities specifically designed for parking.

Transport, Freight, Travel and Vehicles

VAT rates in transport vary significantly. Aircraft repair and maintenance are zero-rated (VAT Notice 744C). Freight transport to or from a place outside the UK is zero-rated, including the domestic leg of such international freight (VAT Notice 744B). The sale, lease, or hire of freight containers to a place outside the UK and the EU is also zero-rated (VAT Notice 703/1). Passenger transport in a vehicle, boat, or aircraft carrying not less than 10 passengers is zero-rated (VAT Notice 744A). Houseboat moorings and parking spaces supplied with them are exempt (VAT Notice 742). Tolls for bridges, tunnels, and roads operated by public authorities are outside the scope of VAT, whereas privately-operated tolls are standard-rated (VAT Notice 700).

Printing, Postage, Publications – Books, Magazines and Newspapers

Many items in this category benefit from zero-rating. Babywear, children’s clothes and footwear are zero-rated (VAT Notice 714). Books, magazines, and newspapers are also zero-rated. For postage, public postal services provided by Royal Mail under a universal service obligation (e.g., standard first and second class services) are exempt. Direct-mail postal services meeting specific conditions can be outside the scope of VAT (VAT Notice 700/24). If postage, packing, and delivery within the UK are included in the sales contract but charged separately, they take the same rate as the goods delivered. However, if charged as an optional extra, they are always standard-rated.

Other Categories

While this guide highlights many key areas, certain categories like Protective and Safety Equipment, Financial Services and Investments, and Insurance also have specific VAT rules that apply to them, though the detailed rates for these were not provided in this specific guidance. Businesses operating in these areas must consult the relevant HMRC VAT notices to ensure correct application of VAT.

Key VAT Rates at a Glance

| Goods/Services | Typical VAT Rate | Conditions/Notes |

|---|---|---|

| Most Food for Human Consumption | Zero-rated | Excludes catering, hot takeaways, confectionery, alcoholic drinks, etc. |

| Domestic Electricity/Gas | 5% Reduced Rate | For domestic and residential use or non-business charity use. |

| Education (Eligible Body) | Exempt | Provided by eligible bodies, closely connected goods/services. |

| International Freight Transport | Zero-rated | To or from a place outside the UK. |

| Children's Clothes & Footwear | Zero-rated | Specific to children's sizes. |

| Hot Takeaway Food | Standard-rated | Unless consumed in a designated area. Was 5% from 15/07/2020 to 31/03/2021. |

| Privately-operated Bridge Tolls | Standard-rated | Public authority tolls are outside the scope of VAT. |

Frequently Asked Questions About UK VAT

What is the difference between 'exempt' and 'zero-rated' supplies?

This is a common point of confusion. 'Zero-rated' means that VAT is charged at 0%. You still account for these sales in your VAT return, and crucially, you can usually reclaim any input VAT on related purchases. 'Exempt' means that the supply is not subject to VAT at all. You do not charge VAT on these sales, and you generally cannot reclaim any input VAT on costs related to making exempt supplies. For example, most food is zero-rated, while most education from an eligible body is exempt.

Why are some food items zero-rated but hot takeaways or restaurant meals standard-rated?

The distinction lies in the 'catering' element. When food is prepared and served for immediate consumption, or consumed in a designated area, it's considered a catering service, which is standard-rated. This includes hot takeaways, restaurant meals, and even hot food from a supermarket deli. Basic foodstuffs, designed for home preparation and consumption, remain zero-rated.

Do charities always avoid VAT on their purchases or sales?

Not always. While charities can benefit from specific VAT reliefs and exemptions on certain supplies (e.g., some welfare services), and some goods supplied to them might be zero-rated (e.g., certain building works for disabled people), they are generally subject to VAT like any other entity for their taxable supplies. They may also incur standard-rated VAT on their purchases. Specific rules apply, making it essential for charities to understand their unique VAT position.

Can I reclaim VAT on international shipping costs?

If you are a VAT-registered business and the international shipping forms part of a zero-rated export of goods, then the associated VAT on the shipping costs (if any were charged, e.g., for domestic legs of international freight) would typically be reclaimable as input VAT. However, domestic freight transport that is not part of an international journey is generally standard-rated.

Are all energy-saving material installations eligible for the reduced rate?

No, not all. For energy-saving materials installed in dwellings, the reduced rate of 5% applies under specific conditions. These often relate to the age or benefit status of the recipient or the cost proportion of the materials versus the installation service. If the cost of the materials exceeds 60% of the total installation cost (excluding VAT), the reduced rate might only apply to the installation service itself, with the materials being standard-rated. It's crucial to check the specific criteria in VAT Notice 708/6.

Conclusion

The UK VAT system is a dynamic and intricate framework that demands careful attention from all businesses. From the nuances of food and drink classifications to the specific exemptions for education and health, and the varied rates for utilities and transport, understanding where your goods and services fit is paramount. The difference between exempt and zero-rated status is a particularly common area of misunderstanding that can have significant financial implications.

While this guide provides a comprehensive overview based on HMRC's guidance, it is not exhaustive. The precise nature of your business activities, the conditions under which you operate, and your meticulous record-keeping are all critical factors in determining the correct VAT treatment. For specific advice tailored to your unique circumstances, always consider consulting HMRC's official guidance or a qualified tax professional. Ensuring accurate VAT application is not just about avoiding penalties; it's about maintaining healthy financial operations and contributing correctly to the UK's economic framework.

If you want to read more articles similar to Navigating UK VAT: Your Essential Guide, you can visit the Automotive category.