23/01/2009

Driving on UK roads without valid vehicle insurance is not just a minor infraction; it's a serious criminal offence with significant consequences. The law is unequivocal: if you're behind the wheel of any vehicle, you must have appropriate insurance cover in place. The penalties for non-compliance are severe and can have a lasting impact on your finances, driving record, and even your freedom. Imagine facing an immediate £300 fine and six penalty points, or worse, an unlimited fine in court, a driving ban, and even the seizure of your vehicle. Furthermore, a criminal record for such an offence can haunt you for years, making future insurance premiums sky-high. Given these stark realities, ensuring your car insurance is valid at all times isn't merely good practice; it's an absolute necessity. But how can you be certain your policy is current and covers you for your specific circumstances? This comprehensive guide will walk you through the essential steps to verify your insurance validity, offering peace of mind and keeping you on the right side of the law.

Why Is Checking Your Insurance Validity So Crucial?

Beyond the obvious legal requirement, there are compelling reasons why regularly checking the validity of your car insurance is paramount. Firstly, the penalties are incredibly harsh. As mentioned, being caught driving uninsured means an immediate £300 fixed penalty notice and six points on your driving licence. Accumulate 12 or more points within three years, and you're looking at a driving ban, which could devastate your ability to commute, work, or manage daily life. In more serious cases, or if you challenge the fixed penalty in court, the fines can be unlimited, truly crippling your finances. Police also have the power to seize and impound your vehicle immediately, leaving you with hefty recovery fees on top of everything else. And it doesn't end there; a conviction for driving without insurance results in a criminal record, which can affect employment opportunities and travel. Long after fines are paid and points eventually removed, future insurance premiums will be significantly higher, potentially for many years, as you'll be considered a high-risk driver. Secondly, in the event of an accident, if you're uninsured, you'll be personally liable for all damages and injuries to third parties. This could run into hundreds of thousands, or even millions, of pounds, leading to financial ruin. Clearly, a quick check now could save you an immense amount of trouble and expense later.

The Definitive Check: The Motor Insurance Database (MID)

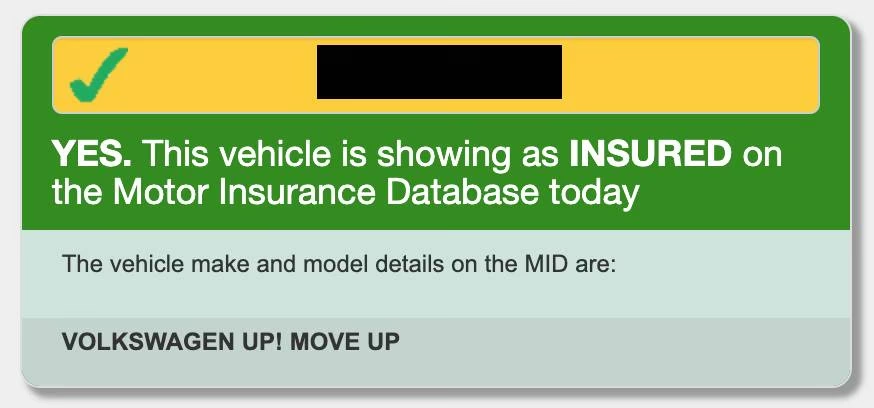

The most authoritative and straightforward way to check if your car is insured is through the Motor Insurance Database (MID). The MID is a central record of all insured vehicles in the UK, maintained by the Motor Insurers' Bureau (MIB). Police use this database to identify uninsured drivers, and it's also accessible to the public for free via the AskMID.com website. This is your primary tool for verifying your insurance status.

How to Use AskMID.com

- Visit AskMID.com: Open your web browser and navigate to the official AskMID.com website. Be wary of unofficial sites.

- Enter Your Vehicle Registration Number: On the homepage, you'll find a simple form asking for your vehicle's registration number (number plate). Enter it carefully to avoid errors.

- Confirm You Are the Keeper: You'll be asked to confirm that you are the registered keeper of the vehicle or have permission to check its insurance status. This is a legal requirement.

- View Results: The website will then display whether your vehicle is currently recorded as insured on the MID. It will show the make and model of the car and confirm if it's insured.

It's important to remember that the MID can take up to 48 hours to update after you've purchased or renewed a policy. So, if you've just taken out new insurance, don't panic if it doesn't show up immediately. Always keep your physical or digital policy documents handy during this brief transition period. If more than 48 hours have passed and your vehicle still isn't showing as insured, or if the details are incorrect, contact your insurer immediately.

Beyond AskMID: Other Ways to Verify Your Policy

While AskMID is an excellent first port of call, it's not the only way to confirm your insurance details. Your own policy documents are the definitive source of truth and should always be consulted.

Reviewing Your Policy Documents

When you purchase or renew car insurance, your insurer will provide you with policy documents. These might be sent via email, accessible through an online customer portal, or delivered as physical paper copies. These documents contain all the critical information about your cover:

- Policy Number: A unique identifier for your insurance contract.

- Effective Dates: Clearly states the start and end dates of your cover. Ensure the current date falls within this period.

- Vehicle Details: Confirms the make, model, and crucially, the registration number of the insured vehicle. Make sure this matches your car exactly.

- Named Drivers: Lists all individuals legally permitted to drive the vehicle under the policy.

- Level of Cover: Specifies whether you have Third Party Only, Third Party Fire & Theft, or Comprehensive cover.

- Policy Excess: The amount you'd need to pay towards a claim.

- Conditions and Exclusions: Important clauses that could invalidate your cover if not adhered to.

Always keep these documents in an accessible place, either digitally on your phone or computer, or a physical copy at home. Regularly review them, especially after any changes to your circumstances or vehicle.

Contacting Your Insurer Directly

If you're still unsure after checking AskMID and your policy documents, or if you have specific questions, the most reliable course of action is to contact your insurance provider directly. Their customer service team can confirm your policy's status, clarify any ambiguities, and provide immediate reassurance. Have your policy number and vehicle registration ready to speed up the process.

Renewal Notices

Your insurer will typically send you a renewal notice a few weeks before your current policy is due to expire. This notice will outline the new premium, terms, and conditions for the upcoming year. It's vital to read these carefully. Many policies now auto-renew, so if you don't explicitly cancel or switch, your cover might continue. However, it's your responsibility to ensure the payment goes through and that the new policy is active and suitable for your needs. Always confirm the new policy's start date and ensure there are no gaps in cover.

Common Pitfalls That Can Invalidate Your Insurance

Even if you've paid your premiums, certain actions or omissions can render your insurance invalid, leaving you exposed to severe penalties. Insurers rely on accurate information, and any significant changes not declared could be problematic.

- Undeclared Modifications: Any changes to your vehicle's engine, suspension, bodywork, or even cosmetic alterations like alloy wheels or tinted windows, must be declared. Failing to do so can invalidate your policy, as modifications can alter the vehicle's risk profile.

- Incorrect Information: Providing false or inaccurate information during the application process, whether intentional or accidental, is a major issue. This includes your address, occupation, estimated annual mileage, where the car is parked overnight, or even your claims history. Always ensure all details are precise and up-to-date.

- Lapsed Payments: If you pay your premiums monthly via direct debit and a payment is missed or bounces, your insurer may cancel your policy. You might receive a warning, but ultimately, non-payment will lead to invalid cover.

- Unlisted Drivers: Allowing someone who isn't named on your policy to drive your car can invalidate your insurance, especially if they have an accident. Always ensure all regular drivers are explicitly added to your policy.

- Change of Usage: If your car's primary use changes (e.g., from social, domestic, and pleasure to commuting, or even business use), you must inform your insurer. Different uses carry different risk levels and premiums.

- Driving Other Cars (DOC) Clause: Many comprehensive policies used to include a 'driving other cars' (DOC) clause, allowing the policyholder to drive another vehicle (that they don't own) with third-party only cover. However, this is becoming increasingly rare, often restricted to drivers over 25, and is never guaranteed. Crucially, you must check your specific policy documents for this clause and understand its limitations. Never assume you have DOC cover; it's a common misconception leading to uninsured driving.

- Selling Your Car: When you sell a vehicle, you must inform your insurer to either cancel the policy or transfer it to a new vehicle. If you fail to do so, and the new owner drives without their own insurance, it could cause complications.

- New Car Purchase: Never assume your existing insurance automatically covers a newly acquired vehicle. You must either transfer your current policy to the new car or purchase a new policy before driving it.

What Happens If Your Insurance Isn't Valid?

The consequences of driving without valid insurance in the UK are severe and far-reaching:

- On-the-Spot Fine & Points: A fixed penalty of £300 and 6 penalty points on your driving licence.

- Unlimited Court Fine: If the case goes to court, you could face an unlimited fine.

- Driving Ban: Accumulating 12 or more points within three years will result in a minimum 6-month driving ban.

- Vehicle Seizure: Police have the power to seize and impound your vehicle immediately. You'll incur significant recovery and storage fees to get it back, assuming you can prove valid insurance.

- Criminal Record: Driving without insurance is a criminal offence, leading to a criminal record that can impact future employment, travel, and visa applications.

- Sky-High Future Premiums: Insurers will view you as a high-risk driver, leading to significantly increased premiums for years to come.

- Personal Liability in an Accident: If you cause an accident while uninsured, you will be personally liable for all damages and injuries. This could amount to hundreds of thousands or even millions of pounds, potentially leading to bankruptcy.

What To Do If You Discover Your Insurance Is Invalid

If you check your insurance and find it's not valid, or there's a discrepancy, the most important thing is to not drive the vehicle. Immediately contact your insurance provider to understand why it's invalid and to rectify the situation. If your policy has been cancelled or lapsed, you'll need to arrange new cover before getting back on the road. Do not delay, as driving even for a short distance could lead to severe penalties.

Valid vs. Invalid Insurance: A Comparative Overview

To highlight the stark differences, consider this comparison:

| Aspect | Valid Insurance (Peace of Mind) | Invalid Insurance (Risky Business) |

|---|---|---|

| Legality | Fully compliant with UK law, no worries. | Illegal, criminal offence, immediate penalties. |

| Financial Security | Insurer handles claims, protects your assets. | Personal liability for all damages, potential bankruptcy. |

| Driving Licence | Secure, no penalty points for insurance. | 6 points, potential driving ban, criminal record. |

| Vehicle Status | Road legal, secure from seizure. | Risk of immediate seizure, impoundment fees. |

| Future Premiums | Generally stable, good driving record helps. | Massively increased, considered high-risk for years. |

| Accident Response | Insurer deals with legal and financial aftermath. | You are solely responsible for all costs and legal issues. |

| Overall Stress | Low, confident on the road. | High, constant worry about being caught, post-accident burden. |

Frequently Asked Questions (FAQs)

Q: How quickly does my insurance show on AskMID?

A: It can take up to 48 hours for your insurance details to appear or update on the Motor Insurance Database (MID). If it's been longer than 48 hours and your details are incorrect or missing, contact your insurer immediately.

Q: Can I drive a new car home without insurance?

A: No, absolutely not. You must have valid insurance in place for the new vehicle before you drive it, even if it's just from the dealership to your home. Many dealerships offer temporary drive-away insurance, or you can arrange cover beforehand.

Q: What if I borrowed a friend's car? Do I need my own insurance?

A: Yes, you usually need your own insurance. While some comprehensive policies used to include a 'Driving Other Cars' (DOC) clause, this is now rare and comes with strict limitations (often third-party only, for cars you don't own, and for drivers over 25). Never assume you have DOC cover. The safest option is to be added as a named driver on your friend's policy, or to take out temporary cover for the specific period.

Q: My policy says "driving other cars" – is that enough?

A: It might be, but you must read your specific policy documents very carefully. The DOC clause is often highly restrictive, providing only third-party cover, and may only apply to vehicles you do not own. It will never cover you for a car you own but haven't insured, or for business use. Always verify the exact terms and conditions with your insurer.

Q: What if I forget to renew my insurance?

A: If your policy lapses, you are immediately uninsured. Driving the vehicle, even unknowingly, is illegal and carries severe penalties. Your insurer will usually send renewal reminders, but it's ultimately your responsibility to ensure continuous cover. If you forget, do not drive the car until you've arranged new insurance.

Q: Does comprehensive cover allow me to drive any car?

A: No, comprehensive cover typically only applies to the specific vehicle(s) listed on your policy. It does not automatically grant you permission to drive any car. Any 'Driving Other Cars' (DOC) clause is separate, limited, and generally only provides third-party cover for unowned vehicles, if it exists at all. Always check your policy wording.

Conclusion

The message is clear: driving without valid car insurance on UK roads is a grave error with far-reaching and severe repercussions. From hefty fines and penalty points to driving bans, vehicle seizure, and the burden of a criminal record, the risks are simply not worth taking. Furthermore, the financial liability in the event of an accident could be catastrophic. By regularly checking your insurance validity using the Motor Insurance Database (AskMID.com) and diligently reviewing your policy documents, you can ensure you're always compliant with the law and protected against unforeseen circumstances. Don't leave it to chance; a few minutes spent verifying your cover today can save you from a lifetime of regret and financial hardship. Drive safely, drive legally, and always drive insured.

If you want to read more articles similar to Is Your Car Insurance Valid? A UK Driver's Guide, you can visit the Insurance category.