06/01/2009

The oil and gas industry stands at a pivotal juncture, where its long-term viability is inextricably linked to its capacity to manage and significantly reduce its carbon footprint. This isn't merely an environmental aspiration; it's a fundamental strategic imperative reshaping the future of energy. As global demands shift and climate concerns intensify, the sector must proactively address its emissions across the entire supply chain, from the initial stages of extraction and processing right through to the final consumption of its products. This monumental undertaking necessitates unprecedented collaboration between industry players, governments, and even consumers, forging a collective path towards a lower-carbon future.

For too long, the economic viability of energy projects was solely measured by a breakeven price. However, a truly competitive portfolio in today's climate-conscious world must also rigorously account for its carbon intensity. Leading companies are now incorporating a 'shadow price of carbon' into their project-level economics, allowing them to optimise their investments for both financial returns and environmental impact. This drive towards a low-carbon, low-cost paradigm is becoming the new industry standard, offering a distinct competitive advantage to those who embrace it. Surprisingly, some nations, like Saudi Arabia, have already demonstrated the ability to produce oil with a remarkably low carbon footprint, setting a precedent for what is achievable.

- Reducing 'Own' Emissions: Scope 1 and 2

- Addressing the Elephant in the Room: Scope 3 Emissions

- The UK's Decarbonisation Journey: A Broader Context

- The Global Footprint: Emissions from International Trade

- Frequently Asked Questions (FAQs)

- What are the biggest challenges for the oil and gas industry in reducing emissions?

- How can Carbon Capture Usage and Storage (CCUS) help the oil and gas industry?

- Is the UK's focus on electrification relevant to the oil and gas industry?

- What is 'carbon leakage' and why is it a concern?

- How important is consumer behaviour in reducing emissions from oil and gas?

- Conclusion

Reducing 'Own' Emissions: Scope 1 and 2

The first crucial step for any oil and gas company on its decarbonisation journey is to minimise its direct operational emissions, commonly referred to as Scope 1 and Scope 2 emissions. Scope 1 encompasses direct emissions from sources owned or controlled by the company, such as methane leaks from pipelines or emissions from flaring. Scope 2 emissions are indirect emissions from the generation of purchased electricity, heating, or cooling consumed by the company. An increasing number of industry leaders are setting ambitious targets for these scopes, implementing a range of actions both individually and through collaborative initiatives like the Oil & Gas Climate Initiative.

Key strategies for tackling Scope 1 and 2 emissions include:

- Eliminating Methane Leaks, Flaring, and Venting: Methane is a potent greenhouse gas, and preventing its release through improved infrastructure, diligent maintenance, and advanced leak detection technologies offers immediate and significant reductions. Flaring (burning off excess gas) and venting (releasing gas directly) are also prime targets for elimination through better gas capture and utilisation.

- Scaling Up Carbon Capture Usage and Storage (CCUS) Development and Deployment:CCUS technologies capture CO2 emissions from industrial processes or power generation and then either reuse or store them permanently underground. Accelerating the development and widespread deployment of CCUS is vital for decarbonising hard-to-abate emissions from industrial operations.

- Switching Fuel and Improving Energy Efficiency of Operations: Transitioning from higher-carbon fuels to cleaner alternatives within operations, such as renewable electricity or hydrogen, can drastically cut emissions. Concurrently, improving the energy efficiency of all processes, from drilling to refining, reduces overall energy demand and thus associated emissions.

- Utilising Lower-Carbon Feedstocks to Offer Low-Carbon Products: Exploring and integrating lower-carbon raw materials into production processes can lead to the development of products with a reduced lifecycle carbon footprint, catering to a growing demand for sustainable solutions.

- Collaborating Across the Supply Chain: No single entity can achieve significant emission reductions in isolation. Partnerships with suppliers, contractors, and other industry players are essential to identify and implement best practices and innovative solutions throughout the entire operational chain.

- Building Capacities to Measure Emissions Granularly: Accurate and granular measurement of emissions is the foundation for effective reduction strategies. Companies need robust systems to track, report, and verify their emissions data to identify hotspots and monitor progress effectively.

The potential for profitable emission reduction in these areas is enormous. An analysis by Accenture suggests that a concerted effort from the oil and gas ecosystem, investing in scalable and profitable solutions, could slash CO2 emissions from 5 gigatonnes to less than 1 gigatonne per year by 2050. This staggering reduction is equivalent to the European Union's combined emissions, or 80% of the US's, or the combined emissions of India and Russia.

Addressing the Elephant in the Room: Scope 3 Emissions

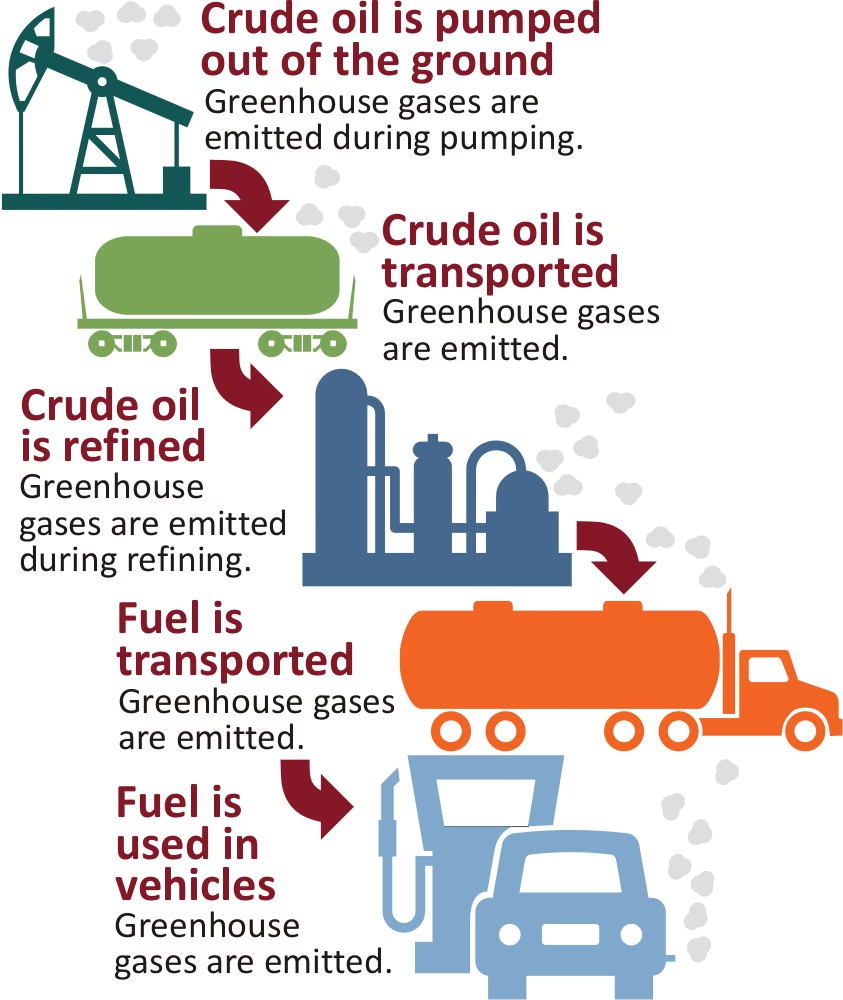

While industry's direct emissions (Scope 1 and 2) are being actively addressed, an even larger and more complex challenge lies in Scope 3 emissions. These are indirect emissions that occur in the value chain of the reporting company, including both upstream and downstream emissions. Crucially, emissions from the fuels burnt by end-users and consumers (downstream Scope 3) are responsible for a staggering 75-80% of the 35 gigatonnes generated annually from the lifecycle of oil and gas products.

Defining, bounding, and allocating accountability for Scope 3 emissions remains a significant challenge for industry experts and policymakers. Consider a practical example: a litre of petrol used by a consumer, produced by company A, used in a car manufactured by company B, on a road built by company C, and financed by bank D. How should the emissions and accountability be distributed among the consumer and companies A, B, C, and D? The complexity multiplies rapidly when considering the myriad actors involved in real-world scenarios.

While a definitive, universally agreed-upon answer may remain elusive, it is unequivocally clear that a strategy must be found to manage this substantial portion of emissions. Since consumer choices and behaviours are the primary drivers behind industrial Scope 3 emissions, any effective strategy must be consumer-centred. This approach not only helps to address the emissions challenge but also unlocks opportunities to create and capture new markets for low-carbon fuels, solutions, and services that empower consumers to minimise their own carbon footprint.

The UK's Decarbonisation Journey: A Broader Context

The UK has demonstrated a leading commitment to decarbonisation, with greenhouse gas emissions more than halving since 1990. This progress has been significantly accelerated since the introduction of the Climate Change Act in 2008. The initial success was largely driven by the decarbonisation of the electricity system, with renewables progressively replacing coal and, increasingly, natural gas. The UK's last coal-fired power station, Ratcliffe-on-Soar, closed in October 2024, marking a major milestone.

However, future progress towards the ambitious target of a 68% reduction by 2030 (on 1990 levels) and ultimately Net Zero by 2050 will require a much broader transformation. The focus is now shifting to widespread electrification across key sectors: surface transport, heating in buildings, and industry. For instance, the number of electric cars on UK roads has roughly doubled every two years, and heat pump installations saw a 56% increase in 2024. While encouraging, the pace of change in these areas, particularly in buildings and industry, still needs to accelerate significantly to meet targets.

The move away from fossil fuels also critically enhances the UK's energy security, reducing dependence on volatile international prices and imports. The transition to a predominantly home-grown energy supply system, powered by modern, efficient electric technologies, promises lower household bills, improved air quality, and a robust path to Net Zero.

The Global Footprint: Emissions from International Trade

While territorial emissions (those within a country's borders) are the primary focus of national targets, it's crucial to consider emissions embodied in international trade. The globalisation of economies has led to service-focused nations, like the UK, indirectly creating emissions by outsourcing manufacturing to countries with lower labour costs and, often, more carbon-intensive energy mixes. This concept is often referred to as 'carbon leakage', where domestic emission reductions are potentially offset by increased emissions elsewhere.

The UK provides a compelling example of this trend. Between 1970 and 1986, consumption-based emissions (including imports) were only marginally higher than territorial emissions. However, as the UK economy shifted from manufacturing to services post-1986, this gap widened considerably. By 2007, consumption-based CO2 emissions were 37% higher than territorial emissions, implying that some of the UK's apparent 'decoupling' of GDP from emissions was due to outsourcing rather than purely domestic policy impacts. While both territorial and consumption-based emissions have declined since the 2008 economic downturn, the UK remains a net importer of CO2 emissions.

For example, the UK imports significant carbon emissions from China, where manufacturing processes may be less advanced and rely heavily on coal for energy. This highlights a critical challenge: without a global approach to environmental policy, there's an incentive to outsource emissions to countries with less stringent regulations, potentially undermining global efforts despite domestic improvements. The strong coupling between global GDP and CO2 emissions underscores the need for technological change and robust environmental policies on an international scale to achieve true decoupling.

Comparative Overview of Emission Scopes

Understanding the different categories of emissions is fundamental to effective decarbonisation strategies.

| Emission Scope | Definition | Primary Responsibility | Strategies for Reduction (Oil & Gas) |

|---|---|---|---|

| Scope 1 | Direct emissions from sources owned or controlled by the company. | Company Operations | Methane leak reduction, flaring elimination, fuel switching (on-site), energy efficiency. |

| Scope 2 | Indirect emissions from the generation of purchased energy (electricity, heat, steam, cooling). | Company Energy Consumption | Purchasing renewable electricity, improving energy efficiency of purchased energy use. |

| Scope 3 | All other indirect emissions in a company's value chain, both upstream and downstream. | Value Chain (Suppliers, Consumers, Logistics) | Consumer-centred strategies, lower-carbon products, supply chain collaboration, CCUS for product end-use. |

Frequently Asked Questions (FAQs)

What are the biggest challenges for the oil and gas industry in reducing emissions?

The primary challenge lies in addressing Scope 3 emissions, which represent the vast majority (75-80%) of their lifecycle emissions. These emissions occur when consumers burn the fuels, making them much harder for the industry to directly control. Defining accountability and implementing effective consumer-centred strategies are complex hurdles.

How can Carbon Capture Usage and Storage (CCUS) help the oil and gas industry?

CCUS is crucial for capturing CO2 from industrial processes and power generation, preventing it from entering the atmosphere. For the oil and gas industry, it can decarbonise their own operations (Scope 1 & 2) and also potentially be applied to emissions from the use of their products, though this is more complex and less developed for widespread consumer use.

Is the UK's focus on electrification relevant to the oil and gas industry?

Absolutely. As the UK and other nations electrify their transport, heating, and industrial sectors, the demand for fossil fuels will naturally decrease. This shift necessitates the oil and gas industry to adapt by either producing lower-carbon fuels, investing in renewable energy, or focusing on carbon capture and storage to remain relevant in a Net Zero economy.

What is 'carbon leakage' and why is it a concern?

Carbon leakage occurs when a country's strict climate policies lead to carbon-intensive production moving to countries with weaker regulations, resulting in no net global emission reduction or even an increase. It's a concern because it undermines domestic decarbonisation efforts and highlights the need for international cooperation and consistent global policies.

How important is consumer behaviour in reducing emissions from oil and gas?

Consumer behaviour is paramount, especially for Scope 3 emissions. Choices like opting for electric vehicles, installing heat pumps, and reducing energy consumption directly impact the demand for fossil fuels and thus the emissions associated with their use. Industry and government efforts must enable and incentivise these consumer shifts.

Conclusion

The journey towards a significantly lower-carbon future for the oil and gas industry is complex but undeniable. By diligently tackling Scope 1 and 2 emissions through operational efficiencies, methane abatement, and CCUS, and by innovatively engaging with the formidable challenge of Scope 3 emissions via consumer-centred strategies, the industry can play a crucial role in global decarbonisation. The UK's broader progress in electrification and its experience with consumption-based emissions underscore the interconnectedness of national and international efforts. Ultimately, achieving Net Zero requires a concerted, collaborative effort from all stakeholders, ensuring a sustainable and secure energy future for generations to come.

If you want to read more articles similar to Cutting Carbon: Oil & Gas Industry's Net Zero Path, you can visit the Automotive category.