07/06/2016

Imagine the full cost of a car as a delicious pizza. When you opt for a Personal Contract Purchase (PCP) deal, you typically start by taking a large slice – perhaps 10% of the pizza – which represents your initial deposit. From there, you decide how many smaller slices you want to eat, and over what period of time. However, with PCP, you won't consume the entire pizza. The amount of 'leftovers' is determined upfront, known as the Guaranteed Minimum Future Value (GMFV), and at the end of the agreement, you choose whether to 'eat' the rest by paying the GMFV or simply hand the car back.

This unique structure makes PCP a highly popular car finance option in the UK, offering flexibility that traditional loans or Hire Purchase agreements often don't. But is it the right choice for you? Let's delve deeper into the mechanics of a PCP deal, exploring its benefits, drawbacks, and what you need to consider before signing on the dotted line.

- What Exactly is a PCP Deal?

- The Guaranteed Minimum Future Value (GMFV) Explained

- Understanding Your Payments: Deposit and Monthly Instalments

- Your Options at the End of a PCP Agreement

- PCP vs. Other Popular Car Finance Options

- The Advantages and Disadvantages of PCP

- Is a PCP Deal Right for You?

- Frequently Asked Questions About PCP

What Exactly is a PCP Deal?

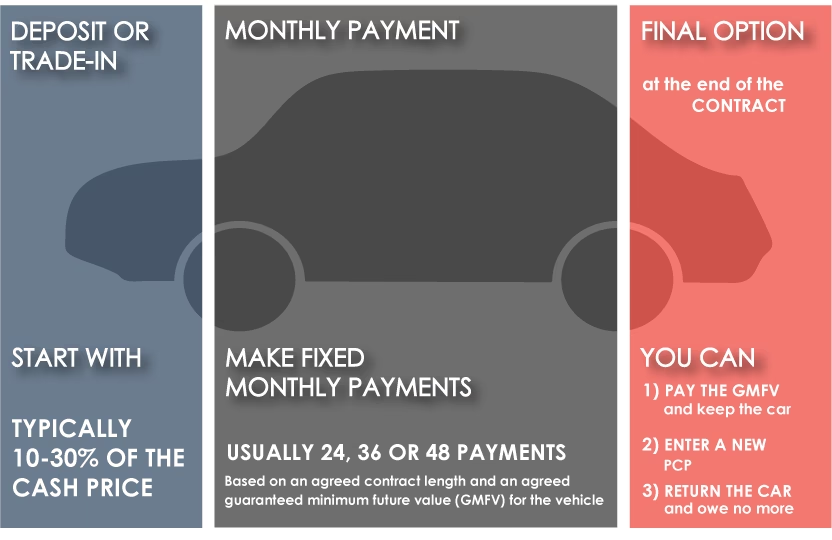

At its core, a PCP agreement is a type of car finance where you pay for the depreciation of the vehicle over an agreed period, rather than its full purchase price. The finance lender estimates how much the car will be worth at the end of the contract, which is the Guaranteed Minimum Future Value (GMFV). Your deposit and subsequent monthly payments cover the difference between the car's initial price and this GMFV, plus interest.

Here's a simple breakdown of how a PCP deal typically works:

- Choose the Contract Length: PCP agreements usually run for two to five years, though longer terms can sometimes be arranged. This period dictates how long you make your monthly payments.

- Pay an Initial Deposit: This can vary significantly. While often around 10% of the car's value, you might find deals with no deposit required, or you could choose to pay a larger sum to reduce your monthly outgoings. The more you put down, the less you'll pay each month.

- Make Fixed Monthly Payments: For the duration of your contract, you'll make an agreed number of fixed monthly payments. The amount is calculated based on the difference between the car's initial price and its GMFV, plus the interest charged by the lender.

- Decide at the End of the Contract: This is where PCP offers its distinct flexibility. You have three primary options, which we'll explore in detail below.

The Guaranteed Minimum Future Value (GMFV) Explained

The GMFV is a crucial element of any PCP agreement. It's the finance company's prediction of what the car will be worth at the end of your contract, assuming it meets certain conditions (such as mileage limits and fair wear and tear). This figure is guaranteed by the lender, meaning even if the car's actual market value drops below the GMFV, you won't be liable for the difference if you decide to hand it back.

The GMFV is influenced by several factors, including:

- The car's make, model, and specification.

- The length of your contract.

- Your agreed annual mileage limit.

- Market trends and the car's predicted depreciation rate.

Understanding the GMFV is vital because it directly impacts your monthly payments. A higher GMFV (meaning the car is predicted to hold its value well) will result in lower monthly payments, as the amount you're financing (the depreciation) is smaller. Conversely, a lower GMFV will lead to higher monthly payments.

Understanding Your Payments: Deposit and Monthly Instalments

Your financial commitment in a PCP deal is split into two main components: the initial deposit and the subsequent monthly payments.

The Initial Deposit

While often recommended to be around 10% of the car's value, the deposit is flexible. Some dealers offer 'no deposit' PCP deals, which can be appealing if you have limited upfront cash. However, be aware that a smaller or zero deposit will increase your monthly payments, as you're financing a larger portion of the car's depreciation. Conversely, a larger deposit will significantly reduce your monthly outgoings, making the deal more affordable on a month-to-month basis.

Fixed Monthly Payments

These payments cover the difference between the car's initial price and its GMFV, plus interest. The interest rate, often referred to as the Annual Percentage Rate (APR), is a critical factor in the total cost of your PCP deal. A lower APR means less interest paid over the term of the agreement. It's always wise to compare APRs from different lenders and negotiate where possible.

It's important to remember that these payments do not contribute towards outright ownership of the vehicle, unless you choose to make the final balloon payment at the end of the contract.

Your Options at the End of a PCP Agreement

The flexibility at the end of the term is arguably PCP's biggest selling point. You have three main choices:

1. Return the Car

If you no longer want the car, or simply fancy a change, you can hand it back to the finance company. Provided you've stayed within your agreed mileage limit and the car is in a condition consistent with 'fair wear and tear' (i.e., no excessive damage), you'll have nothing more to pay. This option is ideal for those who like to drive a new car every few years without the hassle of selling it themselves.

However, be mindful of potential charges for excess mileage or damage beyond what's considered fair wear and tear. These can add unexpected costs, so it's crucial to understand these terms upfront.

2. Buy the Car

If you've fallen in love with your car and want to keep it, you can pay the GMFV, sometimes referred to as the 'balloon payment'. Once this final payment is made, along with a small 'option to purchase' fee, the car is legally yours. This can be a good option if the car's market value at the end of the term is higher than the GMFV, as you're effectively buying it for less than it's worth.

If you don't have the cash readily available for the balloon payment, you might be able to arrange a separate loan to cover this cost.

3. Part-Exchange for a New Car

This is a popular choice for those who enjoy driving a new car regularly. If your car's market value at the end of the contract is higher than its GMFV, you have built up 'equity' in the vehicle. This equity can then be used as a deposit towards a new PCP deal on a different car, effectively rolling you into a new agreement without needing a fresh cash deposit.

However, if the car's market value is less than the GMFV (known as 'negative equity'), you'd need to pay the difference to the finance company before you could use it as a part-exchange, or roll the negative equity into a new deal, which increases the cost of your next car.

PCP vs. Other Popular Car Finance Options

To truly understand if PCP is for you, it's helpful to compare it with other common car finance methods available in the UK.

| Feature | Personal Contract Purchase (PCP) | Hire Purchase (HP) | Personal Loan |

|---|---|---|---|

| Ownership | You do not own the car until the final 'balloon' payment is made. | You own the car after the final monthly payment. | You own the car from day one. |

| Monthly Payments | Typically lower, as you're only paying for depreciation + interest. | Higher than PCP, as you're paying off the full car value + interest. | Payments cover the loan amount + interest; car is collateral. |

| Deposit Required | Often required, but flexible; can be zero. | Often required, typically 10%+. | Not directly related to the loan; you pay cash for the car. |

| End of Contract | Return, buy (balloon payment), or part-exchange. | Car is automatically yours. | Loan repaid; car is yours. |

| Mileage Limits | Yes, often with excess mileage charges. | No. | No. |

| Maintenance Responsibility | Your responsibility, unless a maintenance package is included. | Your responsibility. | Your responsibility. |

| Flexibility | High flexibility at contract end. | Less flexible; aim is ownership. | High flexibility; car is yours to sell or keep. |

The Advantages and Disadvantages of PCP

Like any financial product, PCP comes with its own set of pros and cons.

| Advantages | Disadvantages |

|---|---|

| Lower Monthly Payments: Compared to HP or a personal loan for the same car, PCP payments are typically much lower, making more expensive cars affordable. | You Don't Own the Car: Unless you make the large balloon payment at the end, you never truly own the vehicle. |

| Flexibility at Contract End: You have clear options to return, buy, or part-exchange, suiting various needs. | Mileage Restrictions: Exceeding your agreed annual mileage limit can result in hefty penalty charges. |

| Drive a New Car More Often: The part-exchange option makes it easy to upgrade to a brand-new vehicle every few years. | Fair Wear and Tear Clauses: Damage beyond what's deemed 'fair' can lead to additional charges when returning the car. |

| Avoid Depreciation Risk: The GMFV protects you from unexpected drops in the car's market value. If it's worth less than the GMFV, you can simply hand it back. | Total Cost Can Be Higher: If you intend to buy the car outright at the end, the combined cost of your deposit, monthly payments, and the balloon payment can sometimes exceed the cash price of the car. |

| Fixed Costs: Your monthly payments are fixed, making budgeting straightforward. | Potential for Negative Equity: If the car's market value drops significantly below its GMFV, you could be in negative equity, making part-exchanging trickier. |

| No Hassle of Selling: If you return the car, you avoid the time and effort involved in selling a used vehicle privately. | Modifications: You typically cannot make significant modifications to a car on PCP without permission from the finance company. |

Is a PCP Deal Right for You?

PCP is an excellent option for many drivers, but it's not a universal solution. Consider the following questions to help decide if it aligns with your lifestyle and financial goals:

- Do you like to change your car every few years? If you enjoy driving the latest models and don't want the long-term commitment of ownership, PCP's flexibility is a significant advantage.

- Do you want lower monthly payments? If budgeting for a premium car is a priority, PCP can make it more accessible than other finance options.

- Are you comfortable with mileage limits? If your annual mileage is predictable and within typical limits (e.g., 8,000-12,000 miles per year), PCP can work well. If you're a high-mileage driver, the excess charges could quickly negate the benefits.

- Are you meticulous about car care? Keeping the car in good condition is important to avoid 'fair wear and tear' charges when returning it.

- Is outright ownership a priority? If owning the car outright from day one, or after fixed payments, is crucial to you, then Hire Purchase or a personal loan might be more suitable.

- Do you have a clear plan for the end of the contract? Understanding your options and potential costs at the agreement's conclusion is key to a successful PCP experience.

Frequently Asked Questions About PCP

Can I end my PCP early?

Yes, under the Consumer Credit Act, you typically have the right to voluntary termination once you've paid 50% of the total amount payable (including the GMFV and any fees). However, if you terminate early and haven't paid 50%, you'll need to make up the difference. Be aware of any excess mileage or damage charges that may still apply.

What happens if I go over my mileage limit?

If you exceed your agreed annual mileage, you will be charged an excess mileage fee, usually a set amount per mile (e.g., 6p to 15p per mile). These charges can quickly add up, so it's crucial to be realistic about your driving habits when setting your mileage limit.

What is "fair wear and tear"?

Fair wear and tear refers to the expected deterioration of a vehicle over time and use. It covers minor scratches, small dents, and general ageing that wouldn't typically be repaired. However, significant damage, large dents, tears in upholstery, or missing parts would likely be charged for. Most finance companies provide a guide to fair wear and tear at the start of the agreement.

Can I modify a car on PCP?

Generally, no. Since you don't own the car, you typically cannot make significant modifications (e.g., engine tuning, major bodywork changes) without the finance company's explicit permission. Minor, easily reversible changes like tinting windows might be acceptable, but always check your contract or ask your lender first.

What is equity in a PCP deal?

Equity occurs when the car's actual market value at the end of the contract is higher than its Guaranteed Minimum Future Value (GMFV). This positive difference is your equity, which can be used as a deposit for your next car. If the market value is lower than the GMFV, you are in negative equity.

Is insurance included in PCP?

No, PCP agreements do not typically include car insurance. You are responsible for arranging and paying for your own fully comprehensive insurance for the duration of the agreement.

Can I get a PCP with bad credit?

It can be more challenging to secure a PCP deal with a poor credit history, as lenders may perceive you as a higher risk. However, some specialist lenders cater to individuals with lower credit scores, though the interest rates (APR) will likely be higher. Building a strong credit history before applying is always advisable.

Is PCP good value for money?

Whether PCP offers good value depends entirely on your personal circumstances and intentions. If you want to drive a new car every few years with lower monthly payments and aren't concerned about outright ownership, it can be excellent value. If your ultimate goal is to own the car, paying the large balloon payment at the end might make the overall cost higher than if you had chosen Hire Purchase or a personal loan from the outset.

In conclusion, PCP deals offer a compelling blend of flexibility and affordability, making new cars more accessible to a broader range of drivers across the UK. However, understanding the nuances of the Guaranteed Minimum Future Value, mileage limits, and your end-of-contract options is paramount. By carefully considering your driving habits, financial situation, and long-term goals, you can determine if a PCP agreement is the smart choice for your next vehicle.

If you want to read more articles similar to Should You Buy a Car with a PCP Deal?, you can visit the Automotive category.