07/06/2016

- What is Diminished Value?

- Why Does Diminished Value Occur?

- Types of Diminished Value

- How to Calculate Diminished Value: The Professional Formula

- Factors That Affect Diminished Value (Beyond the Formula)

- Diminished Value vs. Total Loss

- Why Calculate Diminished Value?

- State Laws and Diminished Value Claims

- How to File a Diminished Value Claim

- Common Mistakes to Avoid

- Frequently Asked Questions

- Final Thoughts

What is Diminished Value?

Following a road traffic accident, even if your vehicle is meticulously repaired to its pre-accident condition, it's an unfortunate reality that its market value will likely decrease. This loss in value is known as diminished value. It's the difference between the value of your car before the accident and its value after it has been repaired. Understanding how to calculate this can be crucial, especially when dealing with insurance claims.

Why Does Diminished Value Occur?

The primary reason for diminished value is the inherent stigma attached to vehicles that have been involved in an accident. Potential buyers are often wary of cars with a history of repairs, particularly those involving structural damage or airbag deployment, regardless of the quality of the repairs. This hesitance translates into a lower resale value. Factors influencing the extent of diminished value include:

- Severity of Damage: More significant damage, especially to the frame or structural components, leads to a higher diminished value.

- Vehicle Age and Mileage: Newer, lower-mileage vehicles typically experience a greater percentage of value loss than older, higher-mileage ones.

- Make and Model: Luxury and high-performance vehicles often suffer a more pronounced diminished value compared to more common makes and models.

- Quality of Repairs: While our calculator focuses on inherent diminished value, poor or substandard repairs can exacerbate the loss.

- Accident History Disclosure: Vehicle history reports (like HPI checks in the UK) will flag accident damage, directly impacting resale value.

Types of Diminished Value

It's important to distinguish between the different types of diminished value:

- Inherent Diminished Value: This is the most common type and refers to the automatic loss of value a vehicle sustains simply because it has a recorded accident history, even with perfect repairs. Our calculator primarily addresses this.

- Repair-Related Diminished Value: This occurs when the repairs themselves are substandard, leading to issues like mismatched paint, poor panel alignment, or faulty components. This type often requires a professional inspection to quantify.

- Immediate Diminished Value: This is the difference between the car's value immediately before the accident and its value immediately after repairs are completed. This value tends to decrease over time as the accident fades further into the past.

How to Calculate Diminished Value: The Professional Formula

While a precise calculation can be complex and often requires professional appraisal, a widely accepted method used by insurers and appraisers provides a good estimate. The core formula often looks something like this:

Base Diminished Value Calculation

A common starting point is a percentage of the vehicle's pre-accident retail value. A standard benchmark used is:

Base Diminished Value = 10% of Pre-Accident Value

This 10% is a baseline, and multipliers are then applied to adjust for specific factors. The pre-accident value should reflect the fair market value of your car *before* the incident, not the agreed salvage value if it were a total loss.

Applying Multipliers

To refine the estimate, multipliers are applied based on key factors:

Damage Multiplier

This reflects the severity of the damage and the extent of repairs needed:

| Damage Severity | Multiplier |

|---|---|

| Severe (e.g., Frame Damage) | 1.0 |

| Major (e.g., Airbags Deployed) | 0.75 |

| Moderate (e.g., Significant Body Panel Damage) | 0.5 |

| Minor (e.g., Cosmetic Damage to Panels) | 0.25 |

Mileage Multiplier

This accounts for the vehicle's mileage at the time of the accident, as higher mileage generally lessens the impact of accident history:

| Mileage Range (Miles) | Multiplier |

|---|---|

| 0 - 19,999 | 1.0 |

| 20,000 - 39,999 | 0.8 |

| 40,000 - 59,999 | 0.6 |

| 60,000 - 79,999 | 0.4 |

| 80,000+ | 0.2 |

The Final Diminished Value Calculation

The estimated diminished value is then calculated by applying these multipliers to the base diminished value:

Final Diminished Value = Base Diminished Value × Damage Multiplier × Mileage Multiplier

Example:

Let's say your car had a pre-accident value of £20,000. It sustained moderate damage (Damage Multiplier: 0.5) and had 35,000 miles (Mileage Multiplier: 0.8).

- Base Diminished Value = 10% of £20,000 = £2,000

- Final Diminished Value = £2,000 × 0.5 × 0.8 = £800

In this scenario, your car's value might have diminished by approximately £800 due to the accident history.

Factors That Affect Diminished Value (Beyond the Formula)

While the formula provides a solid estimate, several other factors can influence the final diminished value:

- Vehicle Condition: A vehicle in excellent condition prior to the accident will likely experience a higher diminished value than one that was already in fair or poor condition.

- Market Demand: The popularity and desirability of your car's make and model in the current market play a role. Highly sought-after vehicles might see less impact.

- Repair Quality: While inherent diminished value exists regardless of repair quality, poor repairs (e.g., non-OEM parts, improper paint matching) can significantly worsen the loss. Using certified repair shops can help mitigate this.

- Accident Disclosure Laws: Regulations in your jurisdiction regarding the mandatory disclosure of accident history can impact how much value is lost.

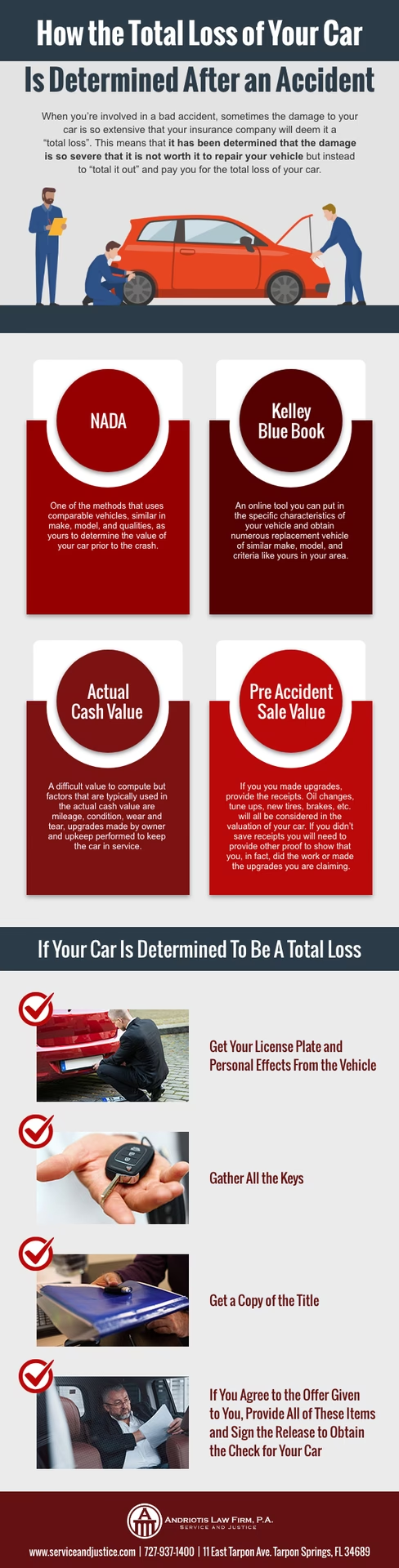

Diminished Value vs. Total Loss

It's crucial to understand that this calculation is for vehicles that are repaired. If a vehicle is deemed a total loss by the insurance company, the calculation changes. In a total loss scenario, the insurer will typically offer you the pre-accident market value of your car (less any deductible). You don't claim diminished value in this case, as the car is effectively replaced rather than repaired.

Why Calculate Diminished Value?

Calculating diminished value is primarily for:

- Insurance Claims: If another driver was at fault for the accident, you have the right to claim diminished value from their insurance company to compensate for the loss in your vehicle's worth.

- Negotiating Trade-In Value: Knowing the diminished value can help you negotiate a fairer price when trading in your vehicle.

- Private Sales: Understanding the loss in value helps you accurately price your car for a private sale.

- Tax Purposes: In some cases, documented diminished value can be considered a casualty loss for tax deductions, though consulting a tax professional is advised.

State Laws and Diminished Value Claims

The ability to claim diminished value, and the specific rules surrounding it, can vary significantly by region.

- Third-Party Claims: In most jurisdictions, you can claim diminished value from the at-fault party's insurance if your car was damaged by their negligence. This is generally the most common and successful route.

- First-Party Claims: Claiming diminished value from your *own* insurance policy (your insurer) is less common and often restricted to specific states or policy types. It's essential to check your policy and local laws.

- Leased Vehicles: If you lease your vehicle, specific clauses in your lease agreement might affect your ability to claim diminished value.

How to File a Diminished Value Claim

Once you have an estimate of your car's diminished value:

- Gather Documentation: Collect all repair invoices, photos of the damage before and after repairs, your vehicle's history report, and any previous appraisals.

- Obtain a Professional Appraisal: While online calculators are useful, a formal appraisal from a qualified expert provides strong evidence for your claim. Many companies specialise in diminished value appraisals.

- Submit a Demand Letter: Write a formal letter to the insurance company (of the at-fault driver) detailing the accident, the damages, the repairs, and the calculated diminished value, supported by your documentation and appraisal.

- Negotiate: Be prepared to negotiate. Insurance companies may offer a lower amount initially. Use your evidence to justify your claim.

- Consider Legal Action: If negotiations fail, you might consider small claims court or consulting a legal professional, especially for higher value claims.

Common Mistakes to Avoid

- Accepting the First Offer: Insurers often start with a lowball offer. Always negotiate.

- Missing Deadlines: Be aware of statutes of limitations for filing claims in your area.

- Not Documenting Pre-Accident Condition: Having photos or records of your car's condition before the accident can be beneficial.

- Using Incorrect Values: Ensure you're using the accurate pre-accident market value for your vehicle.

- Failing to Get Professional Appraisals: Relying solely on online calculators might not be sufficient for a strong claim.

Frequently Asked Questions

Does insurance cover diminished value?

It depends. Third-party claims (against the at-fault driver) typically allow for diminished value claims in most places. First-party claims (against your own insurance) are often excluded or limited by state law and policy terms.

How long do I have to file a diminished value claim?

This varies by jurisdiction. It's often tied to the statute of limitations for property damage claims, which can range from 2 to 6 years. However, it's always best to act sooner rather than later while evidence is fresh and readily available.

Is diminished value tax deductible?

If you incurred diminished value and did not receive full compensation from insurance, you might be able to deduct it as a casualty loss on your taxes. It is highly recommended to consult with a qualified tax advisor for personalized advice.

How accurate are online calculators?

Online calculators, like the one described, provide valuable estimates. They use industry-standard formulas and can give you a strong indication of your potential claim. However, for official purposes and robust negotiation, a professional appraisal is usually required. The accuracy can typically be within 10-15% of a professional assessment.

Final Thoughts

Don't overlook the financial impact of an accident on your vehicle's worth. By understanding the concept of diminished value and knowing how to calculate and claim it, you can ensure you receive fair compensation. Use the tools and information available, gather your evidence diligently, and be prepared to advocate for the true value of your vehicle.

If you want to read more articles similar to Understanding Diminished Vehicle Value, you can visit the Automotive category.