17/10/2009

Understanding VAT Relief for Adapted Vehicles

For many individuals with disabilities, owning a car that meets their specific mobility needs is not just a convenience but a necessity. The cost of adapting a vehicle can be substantial, and thankfully, the UK government offers a valuable tax exemption through VAT relief on qualifying adapted cars. This means that if your vehicle is specifically designed or modified to accommodate a wheelchair user or someone with a significant mobility impairment, you may be able to purchase it without paying Value Added Tax. This can represent a considerable saving, making essential personal transport more accessible. This article will delve into the intricacies of this relief, outlining who is eligible, what constitutes a qualifying adaptation, and the process involved in claiming this exemption.

Who is Eligible for VAT Relief?

The primary criterion for VAT relief on adapted cars centres around the individual's mobility needs. To be eligible, you must meet one of the following conditions:

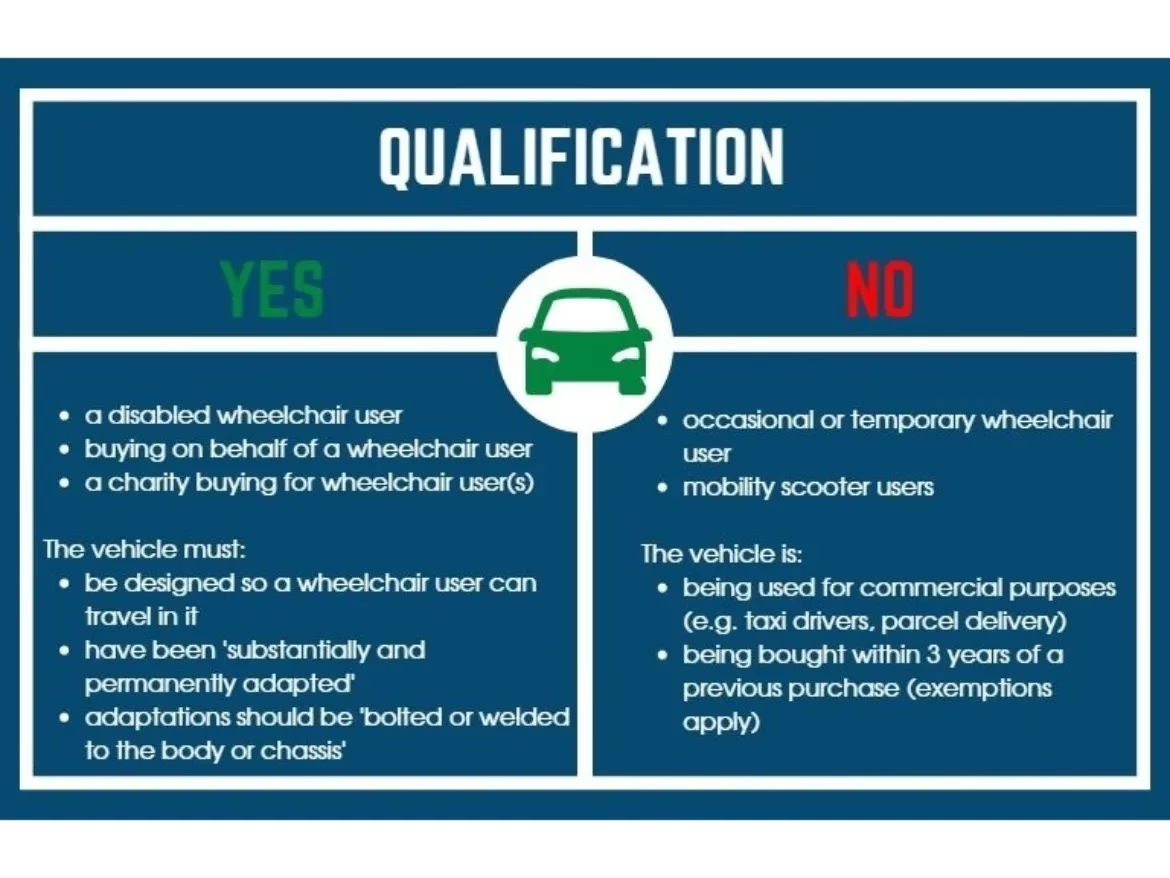

- You are a wheelchair user: The Gov.uk website defines a wheelchair user as 'any disabled person who normally uses a wheelchair (electrically powered or otherwise) in order to be mobile'. This is a crucial definition, and it's important to note that those who only occasionally use a wheelchair may not qualify. Furthermore, mobility scooters, while vital for many, are not considered wheelchairs for the purposes of this VAT exemption, meaning users of mobility scooters typically do not qualify for this specific relief.

- You have a disability that makes it difficult or impossible to use a standard car: This category encompasses a broader range of disabilities that directly impact your ability to enter, exit, or operate a conventional vehicle. The key is that the disability necessitates the use of an adapted vehicle.

Beyond the individual's disability, there are other essential requirements:

- Driving Licence: You must possess a valid driving licence. If you do not drive yourself, you must have a designated person who can legally drive the vehicle on your behalf.

- Personal Use: The adapted vehicle must be intended for your personal use. This includes essential journeys such as shopping, transporting children to school, or commuting to and from work. The relief is not applicable if the vehicle is primarily intended for business purposes.

What Qualifies as a 'Substantially and Permanently Adapted' Vehicle?

HM Revenue & Customs (HMRC) has specific rules regarding the types of adaptations that qualify for VAT relief. The vehicle must be 'substantially and permanently adapted' to meet the needs of a wheelchair user or individual with a significant mobility impairment. This means the modifications should be integral to the vehicle's design for its intended purpose and not easily reversible or temporary.

Examples of qualifying adaptations include:

- Ramps and Lifts: Permanent installations that allow for the safe entry and exit of a wheelchair user.

- Swivel Seats: Seats that rotate to facilitate easier transfer into and out of the vehicle.

- Hoists: Mechanical devices designed to assist with lifting and lowering a person into the vehicle.

- Other Modifications: This can include alterations to the vehicle's interior to accommodate wheelchairs, such as lowered floors, securement systems for wheelchairs, or modifications to the driving controls to assist drivers with disabilities.

Crucially, these adaptations should be physically integrated into the vehicle. HMRC guidance specifies that modifications should be 'bolted or welded to the body or chassis...[or]...wired into the electrics of the vehicle'. This underscores the requirement for permanent and significant structural changes, differentiating them from minor or temporary aids.

The Application Process

The process for claiming VAT relief typically involves completing a declaration form when purchasing the adapted vehicle. Your vehicle supplier will usually guide you through this process. You will need to declare that you meet the eligibility criteria and that the vehicle will be used for your personal mobility needs.

It's essential to ensure all information provided is accurate and truthful, as providing false information to obtain tax relief can have serious consequences. Keep records of your purchase and any documentation related to your disability that supports your claim.

Common Scenarios and Clarifications

To further clarify the nuances of VAT relief, let's consider some common questions:

| Scenario | Eligibility for VAT Relief | Explanation |

|---|---|---|

| Person with a mobility scooter. | Generally No | Mobility scooters are not considered wheelchairs for VAT purposes. |

| Person who uses a wheelchair occasionally. | Generally No | Eligibility requires the normal use of a wheelchair for mobility. |

| Someone buying a car for a disabled relative who will drive it. | Yes (if conditions met) | Provided the relative is a wheelchair user or has a qualifying disability, and the car is for their personal use. |

| Purchase of a standard car that will be adapted later. | Yes (if declared correctly) | VAT can be reclaimed on the purchase of a standard car if it is subsequently adapted and meets the criteria. The declaration should be made at the time of purchase. |

| Using the adapted car for business deliveries. | No | The vehicle must be for personal use only. Business use disqualifies the relief. |

Seeking Further Advice

Navigating tax regulations can sometimes be complex. If you have specific questions about your eligibility or the application process, it is highly recommended to seek clarification directly from HM Revenue & Customs. You can do this by sending an enquiry or calling them on 0300 123 1073. They are the definitive source for advice on tax matters and can provide tailored guidance to your situation.

Key Takeaways:

- Eligibility hinges on being a wheelchair user or having a significant mobility impairment requiring an adapted vehicle.

- The vehicle must be substantially and permanently adapted.

- The car is for personal use only.

- Always consult HMRC for definitive advice.

By understanding these guidelines, individuals can more effectively access the financial support available through VAT relief, making adapted vehicle ownership a more attainable reality for those who need it most.

If you want to read more articles similar to VAT Relief on Adapted Cars, you can visit the Automotive category.