06/07/2002

Driving a vehicle on public roads in the United Kingdom comes with a set of responsibilities, and two of the most fundamental are ensuring your vehicle is properly taxed and insured. Many drivers often wonder about the specifics, perhaps questioning if these are truly non-negotiable requirements or merely strong suggestions. Let's be unequivocally clear from the outset: both car tax, officially known as Vehicle Excise Duty (VED), and car insurance are mandatory in the UK. Failure to comply with either can lead to severe penalties, including substantial fines, points on your licence, and even the seizure of your vehicle. This comprehensive guide will delve into the intricacies of both VED and car insurance, explaining what they are, why they're required, and the grave consequences of not adhering to the law.

Understanding these obligations isn't just about avoiding trouble; it's about contributing to the safety and functionality of our roads and protecting yourself and others financially. The system is designed to ensure that all drivers are accountable and that there's a safety net in place should an unfortunate incident occur.

- Vehicle Excise Duty (VED): Dispelling the 'Road Tax' Myth

- Car Insurance: Your Financial Shield

- The Grave Consequences of Non-Compliance

- Statutory Off Road Notification (SORN)

- Comparative Overview: VED vs. Insurance

- Frequently Asked Questions

- Q: Can I drive my new car home from the dealership without tax or insurance?

- Q: What if I only drive my car occasionally? Do I still need to pay VED and have insurance?

- Q: Does my car insurance cover me for driving other people's cars?

- Q: How do the authorities know if my car is taxed and insured?

- Q: Are electric vehicles exempt from VED indefinitely?

- Q: What if I forget to renew my VED or insurance?

- Conclusion

Vehicle Excise Duty (VED): Dispelling the 'Road Tax' Myth

For decades, the term 'road tax' has been colloquially used to describe the charge drivers pay for their vehicles. However, this is a significant misnomer. The correct term is Vehicle Excise Duty (VED). This distinction is crucial because VED is not hypothecated to road maintenance or construction. In simpler terms, the money collected from VED goes directly into the government's consolidated fund, contributing to general public spending, much like income tax or VAT. It does not specifically fund roads, which are instead funded from general taxation.

VED is essentially a tax on owning and keeping a vehicle on public roads. If your vehicle is off the road and not being used, you must declare it with a Statutory Off Road Notification (SORN) to avoid paying VED. Once a vehicle is SORN, it cannot be driven or parked on a public road.

How VED is Calculated and Paid

The calculation of VED is primarily based on the vehicle's CO2 emissions, fuel type, and its age. There are different rates for the first year of registration (the 'first year rate') and subsequent years ('standard rate').

- First Year Rate: This rate is usually higher and is determined by the vehicle's CO2 emissions. Higher emissions typically mean a higher first-year rate.

- Standard Rate: From the second year onwards, most vehicles pay a standard rate. For cars registered after 1 April 2017, this is a flat rate, with an additional premium for cars with a list price over £40,000 when new. This premium applies for five years from the second time the vehicle is taxed.

- Fuel Type: Diesel vehicles that do not meet certain emissions standards often face higher VED charges. Electric vehicles, until April 2025, are exempt from VED, though this is set to change.

- Historic Vehicles: Vehicles over 40 years old are exempt from VED, allowing owners of classic cars to enjoy their vehicles without this particular annual cost.

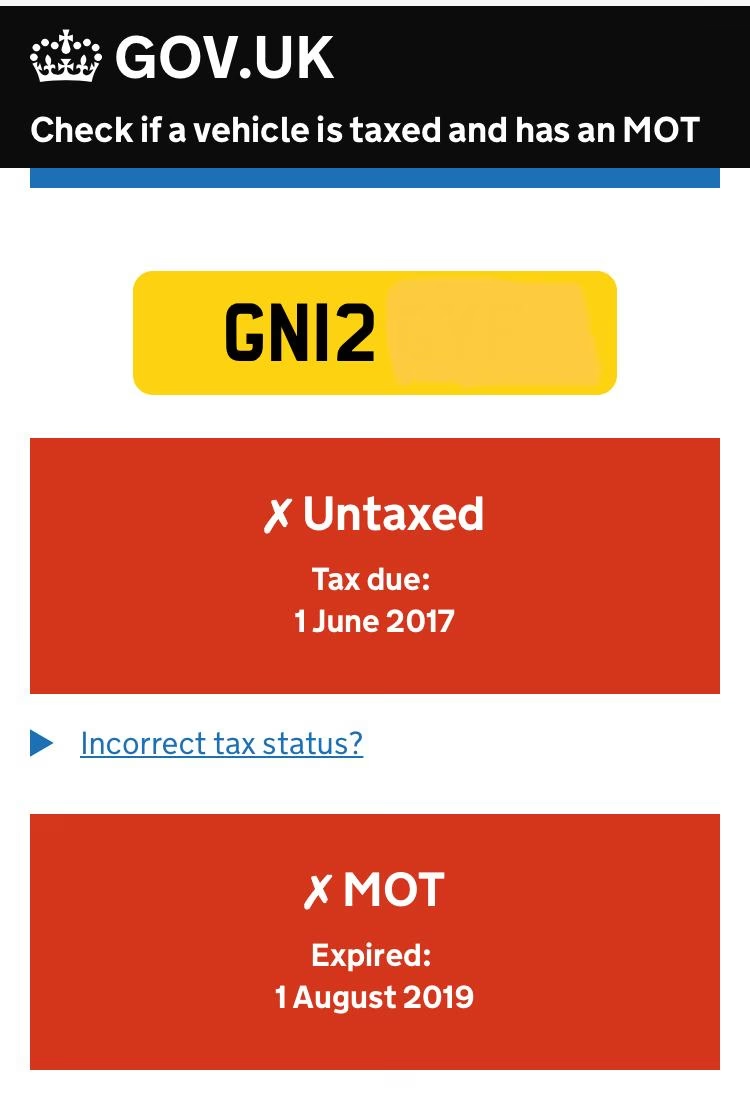

Paying your VED is straightforward and can be done online via the GOV.UK website, at a Post Office, or by phone. You can choose to pay annually, every six months, or monthly via direct debit. The DVLA (Driver and Vehicle Licensing Agency) uses sophisticated systems, including Automatic Number Plate Recognition (ANPR) cameras and comparisons with their databases, to identify untaxed vehicles. There's no longer a physical tax disc to display, so it's entirely digital.

Car Insurance: Your Financial Shield

Car insurance is the second pillar of mandatory vehicle compliance in the UK. Unlike VED, which is a tax, car insurance is a contract between you and an insurance provider. It's designed to provide financial protection against loss or damage that might occur to your vehicle, other vehicles, or property, and to cover personal injury to yourself or others in the event of an accident.

The legal requirement for car insurance is enshrined in the Road Traffic Act. It ensures that anyone driving on public roads has at least third-party cover, meaning that if they cause an accident, any damage or injury to other people or their property will be covered financially. Without this, victims of accidents caused by uninsured drivers would face significant hardship.

Types of Car Insurance

There are three main types of car insurance available in the UK, offering varying levels of cover:

1. Third-Party Only (TPO)

This is the minimum legal requirement. It covers injury or damage to a third party (another person, vehicle, or property) if you are at fault in an accident. It does not cover any damage to your own vehicle or injuries to yourself. While it's the cheapest option upfront, it can leave you significantly out of pocket if your own car is damaged.

2. Third-Party, Fire and Theft (TPFT)

This provides the same cover as TPO, but with the added protection against your vehicle being stolen or catching fire. It still doesn't cover damage to your own vehicle if you're at fault in an accident.

3. Comprehensive Insurance

As the name suggests, this is the most extensive level of cover. It includes everything covered by TPFT, plus it covers damage to your own vehicle, even if you are at fault in an accident. It often includes additional benefits like personal accident cover, medical expenses, and sometimes even a courtesy car while yours is being repaired. Despite being the most expensive on paper, many drivers find that comprehensive policies offer the best value for money due to the peace of mind and extensive protection they provide.

Insurance providers assess a multitude of factors when calculating your premium. These include:

- Your Age and Driving Experience: Younger, less experienced drivers typically pay more due to higher perceived risk.

- Your Driving History: A clean record with no claims or convictions will result in lower premiums.

- The Vehicle Itself: Make, model, engine size, value, and security features all play a role. High-performance or high-value cars are more expensive to insure.

- Your Location: Areas with higher crime rates or traffic density can lead to higher premiums.

- Annual Mileage: The more you drive, the higher the risk of an accident.

- Voluntary Excess: Agreeing to pay a higher voluntary excess (the amount you pay towards a claim) can reduce your premium.

- No-Claims Discount (NCD): For each year you drive without making a claim, you build up an NCD, which can significantly reduce your premium.

- Occupation: Certain professions are deemed higher risk than others.

It's always advisable to shop around and compare quotes from multiple insurers to find the best deal that meets your needs and budget.

The Grave Consequences of Non-Compliance

Ignoring the requirements for VED and car insurance is not just a minor oversight; it carries significant penalties that can have serious financial and legal repercussions.

Untaxed Vehicle Penalties

If your vehicle is found to be untaxed:

- You can receive an automatic £80 fine, which is reduced to £40 if paid within 21 days.

- If the fine remains unpaid, the DVLA can take you to court, where the maximum penalty is £1,000 or five times the amount of the unpaid tax, whichever is greater.

- Your vehicle can be clamped, and you'll have to pay a release fee and show proof of VED to get it back. If it's not claimed, it can be impounded and eventually crushed.

- You could also face a backdated tax bill for the period your vehicle was untaxed.

Uninsured Vehicle Penalties

Driving without valid car insurance is arguably even more serious:

- Fixed Penalty Notice: You can receive a fixed penalty of £300 and 6 penalty points on your licence.

- Court Prosecution: If the case goes to court, you could face an unlimited fine and disqualification from driving.

- Vehicle Seizure: The police have the power to seize, impound, or even destroy your vehicle. You would also be liable for recovery and storage costs.

- Increased Future Premiums: Having a conviction for driving uninsured will make it significantly harder and more expensive to get insurance in the future.

- Personal Liability: If you cause an accident while uninsured, you could be personally liable for the costs of damages and injuries to others, which could amount to hundreds of thousands of pounds and result in severe financial ruin.

The Motor Insurance Database (MID) is a central record of all insured vehicles in the UK, used by the police and DVLA to check insurance status. This, combined with ANPR technology, makes it incredibly difficult to escape detection if you are driving without insurance.

Statutory Off Road Notification (SORN)

If you plan to keep your vehicle off public roads and not use it, you must make a SORN. This tells the DVLA that your vehicle is not being used or kept on a public road, and therefore you do not need to pay VED or have active insurance (though you might still want fire and theft cover if it's stored). A SORN lasts indefinitely until you tax the vehicle again or sell it. If you sell a SORN vehicle, the SORN does not transfer to the new owner; they must make a new one or tax the vehicle immediately.

It's important to remember that a SORN vehicle cannot be driven on a public road for any reason, even for an MOT, unless you have specifically booked an MOT test and are driving directly to and from the test centre.

Comparative Overview: VED vs. Insurance

While both are mandatory, their purpose and how they operate differ significantly:

| Feature | Vehicle Excise Duty (VED) | Car Insurance |

|---|---|---|

| Purpose | Tax on vehicle ownership/use on public roads; contributes to general government funds. | Financial protection against loss/damage/injury from road incidents. |

| Beneficiary | Government (for public spending). | Policyholder (for own losses) and third parties (for their losses caused by policyholder). |

| Calculation Basis | CO2 emissions, fuel type, age, list price. | Driver's age/history, vehicle type, location, mileage, cover level. |

| Payment Frequency | Annually, bi-annually, or monthly. | Annually or monthly. |

| Legal Basis | Vehicle Excise and Registration Act 1994. | Road Traffic Act. |

| Physical Proof | Digital (no tax disc). | Insurance certificate. |

| Off-Road Status | Requires SORN if not taxed and off-road. | Not legally required if vehicle is SORN and off-road. |

Frequently Asked Questions

Q: Can I drive my new car home from the dealership without tax or insurance?

A: No, absolutely not. Before you drive any vehicle on a public road, it must be taxed and insured. Most dealerships will facilitate this process for you at the point of sale, or you must arrange it yourself beforehand.

Q: What if I only drive my car occasionally? Do I still need to pay VED and have insurance?

A: Yes. If your car is kept or driven on a public road, it must be continuously taxed and insured, regardless of how often you use it. If you only use it very rarely and keep it off-road, you might consider a SORN, but remember it cannot then be driven on public roads.

Q: Does my car insurance cover me for driving other people's cars?

A: Not necessarily. While some comprehensive policies include 'Driving Other Cars' (DOC) cover, it's usually third-party only and has strict conditions (e.g., driver must be over 25, the car must be insured by its owner). Always check your policy documents carefully before driving someone else's car.

A: The DVLA and police use Automatic Number Plate Recognition (ANPR) cameras which automatically check your registration against the DVLA's vehicle register (for VED) and the Motor Insurance Database (MID) for insurance. If a discrepancy is found, it can trigger an alert leading to roadside stops or warning letters.

Q: Are electric vehicles exempt from VED indefinitely?

A: No. While electric vehicles currently benefit from VED exemption, this is set to change from April 2025. From that date, they will be subject to VED in the same way as petrol and diesel vehicles, although typically at the lowest rates.

Q: What if I forget to renew my VED or insurance?

A: It is your responsibility to ensure your vehicle is continuously taxed and insured. While reminders are often sent, forgetting is not a valid defence if caught. Set up direct debits for VED and automatic renewals for insurance where possible, or use calendar reminders.

Conclusion

In the UK, Vehicle Excise Duty and car insurance are not optional extras; they are fundamental legal requirements for anyone owning or driving a vehicle on public roads. Understanding these obligations, how they operate, and the severe repercussions of non-compliance is essential for every motorist. Beyond the legalities, having adequate insurance provides crucial financial protection for yourself and others, making our roads safer for everyone. Always ensure your vehicle is compliant to avoid the significant fines, points, and potential vehicle seizure that come with ignoring these vital regulations.

If you want to read more articles similar to UK Car Tax & Insurance: Your Essential Guide, you can visit the Motoring category.