13/03/2004

Understanding the tax implications of owning and maintaining a vehicle is crucial for businesses and individuals alike, regardless of your location. While the United Kingdom operates under a Value Added Tax (VAT) system, many other nations, such as India, utilise a Goods and Services Tax (GST) framework. This article delves into the specifics of GST as it applies to vehicle repairs, maintenance, and purchases, offering valuable insights into concepts like Input Tax Credit (ITC). Please note: The detailed tax rules and examples discussed herein pertain specifically to the Indian GST system and should not be interpreted as UK VAT guidance. However, the underlying principles of indirect taxation and input credits often share conceptual similarities, making this a fascinating exploration for a UK audience interested in comparative tax systems.

In the context of the Goods and Services Tax (GST), vehicle repairs and maintenance are typically subject to a standard rate. According to the specified schedule of rates, GST @ 18% is applicable on these services. This charge is levied by the service provider, and for businesses registered under GST, this input tax is generally eligible for Input Tax Credit (ITC). The 'place of supply' for such services is determined by the location of the service recipient. Consequently, if the supply occurs within the same state (intra-state), both Central GST (CGST) and State GST (SGST) are charged at 9% each, totalling the 18% rate.

Understanding Input Tax Credit (ITC) on Motor Vehicles

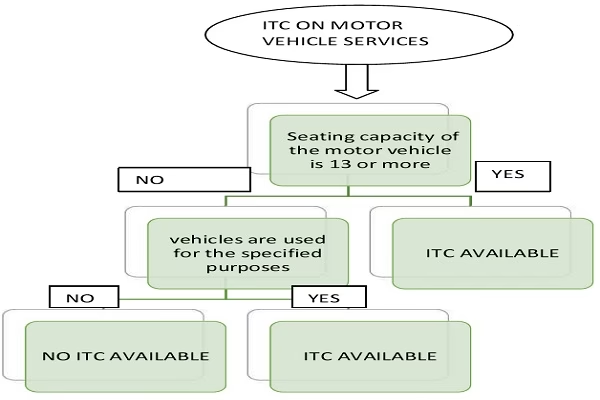

Input Tax Credit is often regarded as the lifeblood of any value-added tax system like GST. Its primary function is to eliminate the cascading effect of taxes, ensuring that tax is only levied on the value added at each stage of the supply chain. This mechanism ultimately helps in reducing the final price of goods and services for the consumer. However, despite this principle of seamless credit flow, certain inward supplies of goods or services are specifically excluded from ITC claims. In the Indian GST framework, Section 17(5) of the CGST Act, 2017, outlines these 'blocked credits', which include certain motor vehicles.

These blocked credits are not available to taxpayers even when the goods or services are used for business purposes and for providing taxable supplies. This means that businesses must carefully consider the type of vehicle they purchase and its intended use to determine ITC eligibility.

Statutory Provisions Regarding Blocked Credit on Motor Vehicles

The provisions concerning blocked credit on motor vehicles under the GST system are quite detailed. ITC can be claimed on vehicles used for transporting goods and on passenger transport vehicles with an approved seating capacity of more than 13 persons (including the driver), without any exceptions. However, for other passenger transport vehicles, such as cars and motorcycles, ITC is generally not admissible, except under specific circumstances outlined in Section 17(5) of the CGST Act.

Let's break down these provisions for clarity:

| Category of Blocked Credit | When ITC is NOT Blocked (ITC is Available) | Remarks |

|---|---|---|

| Motor vehicles for transportation of persons with approved seating capacity of not more than 13 persons (including driver), including leasing, renting, or hiring thereof. Services of general insurance, servicing, repair, and maintenance of these vehicles. | ITC for these motor vehicles and related services will not be blocked when they are used for: i) further supply of such vehicles (e.g., a car dealer selling cars) ii) transportation of passengers (e.g., a taxi service) iii) imparting training on driving of such motor vehicles (e.g., a driving school) | ITC is also admissible for leasing, renting, or hiring of motor vehicles when: i) these are used for making an outward supply of the same category of goods or services or both, or as an element of a taxable composite or mixed supply. ii) it is obligatory for an employer to provide the same to its employees under any law in force. Note: 'Motor Vehicle' includes motorcycles/scooters exceeding 25 CC, so their ITC is also blocked unless above conditions are met. ITC is admissible for motor vehicles for transportation of goods without these restrictions. |

| General Insurance, Servicing, Repair, and Maintenance of otherwise blocked motor vehicles. | ITC will be allowed where: i) the recipient is engaged in the manufacture of such motor vehicles (e.g., a car manufacturer can claim ITC on repair charges for free services provided by dealers). ii) in the supply of general insurance services in respect of such motor vehicles insured by him (e.g., ITC on reinsurance premium paid by an insurance company). | This highlights specific industry-related exceptions where the credit flow is maintained to avoid tax on tax within the manufacturing and insurance sectors. |

It is evident that the purpose of use is a critical factor in determining ITC eligibility. A vehicle bought for direct use in providing a taxable service (like passenger transport) or for resale is treated differently from one bought for general business use, such as a company car for an executive.

Frequently Asked Questions (FAQs) on Input Tax Credit on Motor Vehicles (Under GST Framework)

To further reinforce understanding of these complex rules, let's explore some common scenarios through a series of frequently asked questions, always remembering these apply to the GST system.

Q.1: I am a GST-registered person engaged in trading goods. I have bought a Car for business use. Will I be able to get Input Tax Credit on the GST paid on the purchase of the Car?

Ans: No, ITC cannot be availed. This scenario falls under the blocked credits provision of Section 17(5) of the CGST Act, and your use case does not meet any of the specified exceptions. Furthermore, you will also not be able to claim ITC on GST paid for general insurance, servicing, repair, and maintenance of this car.

Q.2: I am a GST-registered person engaged in manufacturing goods. I have bought a Bus for the transportation of employees to the factory. Will I be able to get Input Tax Credit on the GST paid on the purchase of the Bus?

Ans: Yes, ITC can be availed. Credit is only blocked for passenger vehicles with a seating capacity of not more than 13 persons (including the driver). As a bus typically has a seating capacity above this limit, the credit is not blocked under Section 17(5). Consequently, you will also be able to claim ITC on GST paid for general insurance, servicing, repair, and maintenance of the bus.

Q.3: I am a GST-registered person engaged in trading goods. I have bought a Truck for use in business for the transportation of goods. Will I be able to get Input Tax Credit on the GST paid on the purchase of the Truck?

Ans: Yes, ITC can be availed. The credit blocking provisions under Section 17(5) primarily apply to passenger vehicles. Vehicles designed for the transportation of goods, such as trucks, are generally eligible for ITC. Similarly, ITC on general insurance, servicing, and repair and maintenance of the truck will also be admissible.

Q.4: I am a GST-registered person engaged in supplying consultancy services. I have bought a Motor Cycle for business use. Will I be able to get Input Tax Credit on the GST paid on the purchase of the Motor Cycle?

Ans: No, ITC cannot be availed. This situation falls under the blocked credits of Section 17(5), and your use does not qualify for any of the exceptions. It's important to note that most motorcycles (typically 100 CC and above) are considered 'motor vehicles' under relevant acts, making their ITC generally blocked unless specific conditions are met. If the credit on the motorcycle is blocked, you also cannot avail ITC on its general insurance, servicing, repair, and maintenance.

Q.5: I am a GST-registered person. I have bought a Car for business use. Under what situations will I be able to get Input Tax Credit on the GST paid on the purchase of the Car?

Ans: Input Tax Credit can be availed when such a car is specifically used for:

- Further supply of such vehicles (e.g., a car dealer purchasing a car for resale).

- Transportation of passengers (e.g., purchasing a car for a taxi service or ride-sharing fleet).

- Imparting training on driving of such motor vehicles (e.g., a driving school acquiring cars for instruction).

Q.6: I am a GST-registered person engaged in renting motor vehicles. I have bought a Car for business use. Whether I can avail Input Tax Credit of GST paid on the purchase of the Car?

Ans: No, ITC cannot be availed. While you are engaged in renting motor vehicles, this specific scenario, as per some interpretations, might not be included in the direct exceptions under Section 17(5) of the CGST Act. The exception primarily refers to the 'transportation of passengers', which is distinct from merely 'renting' a vehicle for the client's own use. If the credit on the car purchase is blocked, ITC on its general insurance, servicing, repair, and maintenance would also be blocked.

Q.7: I am a GST-registered person. I have bought a Car for business use. Under what situations will I be able to get Input Tax Credit on the GST paid on Services of general insurance, servicing, repair, and maintenance of said Car?

Ans: Input Tax Credit can be availed for car insurance, servicing, repair, and maintenance when the car itself is used for:

- Further supply of such vehicles.

- Transportation of passengers.

- Imparting training on driving of such motor vehicles.

However, even if the above conditions are not met for the car itself, ITC on general insurance, servicing, repair, and maintenance of motor vehicles will still be allowed where:

- The recipient is engaged in the manufacture of such motor vehicles (e.g., a car manufacturer claiming ITC on repair charges from service dealers for free services given to consumers).

- The recipient is involved in the supply of general insurance services in respect of such motor vehicles insured by them (e.g., an insurance company claiming ITC on reinsurance premium).

Q.8: Whether GST paid on cars provided to different customers on lease rent will be available as Input Tax Credit (ITC) in terms of Section 17(5) of the Central Goods and Service Tax Act, 2017?

Ans: This area has seen some conflicting rulings. The Madhya Pradesh AAR (Authority for Advance Ruling) in the case of Narsingh Transport [2019] held that an applicant is entitled to avail ITC on cars (passenger vehicles) which are further supplied to customers on lease rent, subject to conditions for such service supply. This suggests that supplying vehicles on lease rent could be considered a 'further supply' of services. However, this ruling contrasts with other judgments, like the West Bengal AAR in Mohana Ghosh [2019], which stated that Section 17(5) restricts ITC in cases of renting cars. Our view generally aligns with the idea that ITC for supplying motor vehicles on rent *should* be available, as it constitutes a further supply of services, akin to selling them. Crucially, such vehicles must be registered for commercial use and not for the applicant's own use, and any availed ITC may need to be reversed if the lease terminates and the vehicle is not re-leased.

Q.9: I am a GST-registered person. I have taken a Car on hire for business use. Under what situations will I be able to get Input Tax Credit on the GST paid on hire charges of the Car?

Ans: Input Tax Credit can be availed when such a car on hire is used for:

- Transportation of passengers.

- Imparting training on driving of such motor vehicles.

- Making an outward supply of the same category of goods or services or both, or as an element of a taxable composite or mixed supply (e.g., hiring a vehicle and then further renting it to another person).

- It is obligatory for an employer to provide the same to its employees under any law for the time being in force. (While legally an exception, it's rare for a law to mandate an employer to provide a car specifically for this purpose.)

Q.10: I am a GST-registered person engaged in trading goods. I have taken a Car on hire for business use. Will I be able to get Input Tax Credit on the GST paid on hiring of the Car?

Ans: No, ITC cannot be availed. Similar to purchasing a car for general business use, hiring a car for such purposes by a trader does not fall under the exceptions laid out in Section 17(5).

Q.11: I am a GST-registered person engaged in renting motor vehicles. I have taken a Car on hire for further renting. Will I be able to get Input Tax Credit on the GST paid on hiring of the Car?

Ans: Yes, you would be eligible to avail ITC in this specific instance. This is because these services are used for making an outward supply of the same category of services, i.e., renting of motor vehicles. It's important to differentiate this from *purchasing* a motor vehicle for renting, where ITC is generally not admissible unless it's for the transportation of passengers.

Q.12: Whether an employer/contractor can avail ITC on hiring of commercially licensed vehicles for transportation of its employees?

Ans: The Himachal Pradesh Authority for Advance Ruling (AAR) in the case of Prasar Bharti Broadcasting Corporation of India has ruled that no ITC will be available in respect of renting of taxis used for transportation of employees, if it is not obligatory under any law. This reinforces the principle that mere convenience or company policy is not enough; a statutory obligation is required for this exception.

Q.13: Whether Car Dealers are eligible for ITC on Demo Cars/vehicles?

Ans: Yes, under the GST system, it has been held by the Maharashtra AAR in the case of Chowgule Industries Private Limited that a car dealer is entitled to avail Input Tax Credit (ITC) charged on the inward supply of a motor vehicle used for demonstration purposes in the course of business. This is considered ITC on capital goods and can be utilised for payment of output tax. However, when such demo cars are eventually sold, Section 18(6) of the CGST Act becomes applicable. The car dealer must then pay an amount equal to the ITC taken on the demo vehicle, reduced proportionately based on its remaining useful life (typically considered five years), or the tax on the transaction value of the sale, whichever is higher.

Conclusion

The Goods and Services Tax framework, particularly its provisions regarding Input Tax Credit on motor vehicles and their associated maintenance, presents a complex landscape for businesses. While the UK's VAT system has its own nuances, understanding these GST principles offers a valuable comparative insight into how indirect taxes can significantly impact vehicle-related costs. The core takeaway is that the specific use of a vehicle—whether for further supply, passenger transport, or goods transport—is paramount in determining ITC eligibility, alongside specific exceptions for manufacturers and insurance providers. Businesses must diligently assess their operations against these rules to ensure compliance and maximise legitimate tax credits.

If you want to read more articles similar to Vehicle Tax Implications: A Global Perspective, you can visit the Automotive category.