04/05/2013

Encountering the phrase 'Beyond Economic Repair' (BER) when discussing your vehicle can be a daunting experience. It’s a technical term often used by mechanics and insurance adjusters, and it essentially signifies that the cost of repairing your car to a roadworthy condition exceeds its current market value, or a predetermined threshold. This doesn't necessarily mean the car is irreparable, but rather that the investment required to fix it is no longer financially sensible for the owner or insurer. Understanding what BER entails is crucial for making informed decisions about your vehicle's future.

- Understanding the 'Economic' in Beyond Economic Repair

- When Does a Car Become Beyond Economic Repair?

- The Repair Cost vs. Value Calculation

- What Happens When a Car is Declared BER?

- The 'Write-Off' Categories: Understanding the Nuances

- Is it Ever Worth Repairing a BER Car?

- Key Takeaways

- Frequently Asked Questions

Understanding the 'Economic' in Beyond Economic Repair

The core of the BER designation lies in the word 'economic'. It’s a purely financial calculation. When a car suffers significant damage, whether from an accident, a major mechanical failure, or even extensive wear and tear, the process of assessing its repairability involves comparing the estimated cost of repairs against the car’s pre-damage value. If the repair bill climbs higher than the car's worth, it’s deemed BER. This is a standard practice, particularly in the insurance industry, to prevent owners from spending more on repairs than the vehicle is actually worth.

When Does a Car Become Beyond Economic Repair?

Several scenarios can lead to a vehicle being classified as BER:

- Major Accident Damage: Following a significant collision, the chassis, engine, transmission, or bodywork might be so severely compromised that the labour and parts required for repair push the cost over the vehicle's value. Think of substantial frame damage or extensive damage to multiple critical components.

- Severe Mechanical Failure: A catastrophic engine failure, a complete transmission breakdown, or extensive electrical system faults can also render a car BER. For instance, if the engine seizes and requires a full rebuild or replacement, and the car is older or has high mileage, the repair cost might easily surpass its market value.

- Corrosion and Rust: While less common for a sudden BER classification, severe, widespread corrosion, especially if it affects structural integrity (like the chassis or subframes), can lead to a BER assessment. This is more typical for older vehicles or those exposed to harsh environments.

- Flood Damage: Cars that have been submerged in water, particularly saltwater, often suffer extensive electrical and mechanical damage that is incredibly difficult and expensive to rectify. The corrosion and potential for long-term issues often make them BER.

- Age and Depreciation: Even without a major incident, older cars with significant mileage and accumulated wear and tear are more susceptible to being declared BER. A costly repair on a car that has already depreciated significantly might be deemed uneconomical.

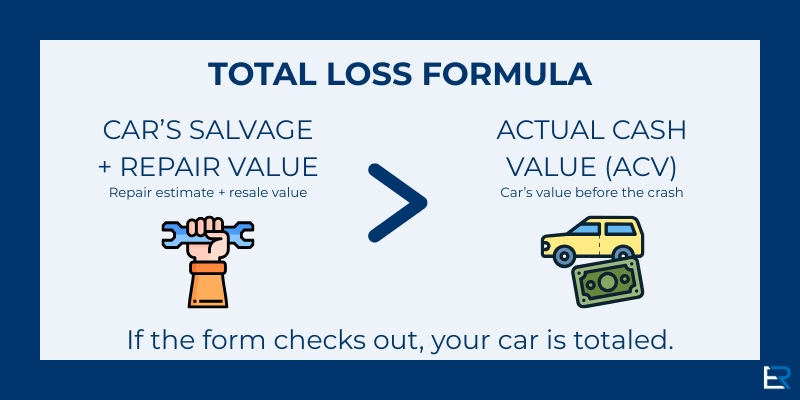

The Repair Cost vs. Value Calculation

The calculation of whether a car is BER is usually performed by qualified assessors, often from an insurance company. They will:

- Assess the Damage: A thorough inspection is carried out to identify all necessary repairs. This includes parts, labour, and any associated costs like diagnostic testing or painting.

- Estimate Repair Costs: Based on the assessment, a detailed quote for the repairs is generated. This quote will factor in the cost of new or used parts, the hourly rate for mechanics, and the estimated time to complete the work.

- Determine the Pre-Accident Value (PAV): This is the market value of the car immediately before the damage occurred. Insurance companies use various sources, including industry guides (like Glass’s Guide in the UK), recent sales data for similar vehicles, and the car’s specific age, mileage, condition, and optional extras.

- Compare Costs and Value: The estimated repair cost is then compared to the PAV. If the repair cost is, for example, 70% or more of the PAV (this percentage threshold can vary between insurers), the vehicle is typically declared BER.

Example Scenario:

Imagine a 10-year-old hatchback with a pre-accident value of £3,000. A significant accident causes damage that an independent garage quotes at £2,800 to repair. In this case, the repair cost (£2,800) is 93% of the car's value (£3,000). If the insurer's threshold for BER is 70%, this car would be declared Beyond Economic Repair.

What Happens When a Car is Declared BER?

When a vehicle is classified as BER, the implications for the owner depend largely on whether the car is insured and the type of insurance policy held:

- With Comprehensive Insurance: If you have comprehensive insurance, the insurer will typically offer you a settlement. This settlement is usually based on the car's pre-accident value, minus any excess you might have to pay. The insurer will then usually take possession of the damaged vehicle, as they have effectively 'written it off'.

- Without Insurance or Third-Party Cover: If you don't have comprehensive insurance, or if the damage isn't covered by your policy (e.g., it's a mechanical failure not due to an accident), you will be responsible for the repair costs. If the car is declared BER, you have a few options:

- Sell for salvage: You can sell the car to a salvage yard or specialist breaker. You'll receive a sum for the remaining value of the parts, but this will be significantly less than the car's pre-accident value.

- Repair it yourself: You could choose to repair the car yourself or find a cheaper mechanic, accepting the financial risk. However, if the car is severely damaged (e.g., chassis damage), it might not be safe to do so.

- Scrap the vehicle: If the car is beyond even salvageable parts, you can have it scrapped. You might receive a small payment for the metal weight, but it's essentially the end of the road for the vehicle.

The 'Write-Off' Categories: Understanding the Nuances

It's important to note that 'Beyond Economic Repair' is a financial assessment, not always a definitive statement about the car's structural safety. Insurers categorise write-offs, and BER often falls into these categories:

| Category | Description |

|---|---|

| Category A | Structurally damaged and must be scrapped. Cannot be repaired or used again. Parts can be reclaimed but the shell must be crushed. |

| Category B | Structurally damaged and must be scrapped. Some parts can be salvaged and reused, but the car itself cannot be returned to the road. The owner must provide proof of disposal. |

| Category S (Previously Category C) | Structurally damaged but repairable. The vehicle has sustained structural damage, and the cost of repair is less than the vehicle's salvage value. These vehicles can be repaired and returned to the road, but must pass a Vehicle Identity Check (VIC) and a standard MOT test. The owner must inform DVLA. |

| Category N (Previously Category D) | Non-structurally damaged and repairable. The vehicle has not sustained structural damage but has been written off by the insurer due to repair costs exceeding its market value. These vehicles can be repaired and returned to the road without a VIC inspection, but still require an MOT. |

A car declared BER by an insurer will typically be assigned a Category S or Category N, depending on the nature of the damage. Category N is often where a car is declared BER due to a major mechanical or electrical fault that isn't structural, or where the repair cost for non-structural damage is simply too high relative to the car's value.

Is it Ever Worth Repairing a BER Car?

For most people, the answer is no. If your insurer declares your car BER, accepting their settlement and purchasing a replacement vehicle is usually the most sensible financial decision. The payout, while less than you might hope, often represents the realistic market value of your car before the incident. Trying to repair a BER vehicle yourself, especially if it's a major mechanical issue, can lead to unforeseen problems and escalating costs. You might end up spending more than the car's value anyway, and you'll still have a vehicle that may have had significant damage, potentially affecting its future resale value or reliability.

However, there might be rare exceptions:

- Sentimental Value: If the car holds immense sentimental value and you are prepared to invest significant personal time and money, you might choose to repair it. This is often a labour of love rather than a financial decision.

- Specialist/Classic Cars: For very rare or classic cars, the market value calculation might not fully reflect their true worth or potential for appreciation. In such cases, specialist repairers might be able to justify higher repair costs, but this is a niche situation.

- DIY Repairs on Minor Issues: If a car is declared BER due to a single, expensive but non-critical component failure, and you have the skills and tools to replace it yourself for a fraction of the professional cost, it might be considered. But again, the risk of other issues needs careful assessment.

Key Takeaways

Being told your car is 'Beyond Economic Repair' means the cost to fix it outweighs its value. This is a financial assessment, not necessarily a death sentence for the vehicle, but it signals the end of its economical life for you or your insurer. Understanding the valuation process, the potential payout from your insurer, and the options for salvage or disposal are crucial steps in navigating this situation. While it can be upsetting, it’s an opportunity to reassess your vehicle needs and potentially move on to a more reliable or suitable car.

Frequently Asked Questions

Q1: What is the typical threshold for a car to be declared BER?

A1: While it varies by insurer, a common threshold is when the estimated repair cost reaches 70% or more of the vehicle's pre-accident market value.

Q2: Can I keep my car if it's declared BER?

A2: Yes, if you are not claiming on insurance, you can keep the car. If you are claiming, the insurer usually takes ownership of the vehicle after paying out the settlement amount.

Q3: If my car is BER, will I get the full market value from my insurer?

A3: You will typically receive the market value of the car before the damage occurred, minus your policy excess. You will not receive funds for the repairs themselves.

Q4: What's the difference between BER and a 'write-off'?

A4: 'Beyond Economic Repair' is the financial assessment. A 'write-off' is the insurer's classification of the vehicle based on that assessment, categorising it as either repairable (Category S/N) or scrap (Category A/B).

Q5: Should I try to repair a Category N vehicle myself?

A5: Only if you are highly skilled, have access to cheap parts, and understand the risks. A Category N vehicle was deemed uneconomical to repair by professionals, and attempting it yourself can be costly and may not result in a safe or reliable vehicle.

If you want to read more articles similar to Beyond Economic Repair: What It Means, you can visit the Repair category.