24/03/2026

Imagine the unthinkable: your beloved car, a vital part of your daily life, is involved in an incident that leaves it severely damaged. Now, imagine facing this devastating situation without the safety net of car insurance. This is a stark reality for many, and understanding the ramifications of a car being written off without adequate cover is crucial. While the bulk of discussions around vehicle write-offs revolve around insurance claims and payouts, the absence of a policy dramatically alters the landscape, leaving you solely responsible for the financial burden and the vehicle's fate. But what exactly constitutes a 'write-off' in the eyes of the automotive and insurance world? Let's delve into the intricacies of this often-misunderstood term and explore what happens when your vehicle is deemed a total loss, both with and without the protection of insurance.

- What Exactly is a Car Insurance Write-Off?

- The Four Write-Off Categories Explained

- Who Decides Your Car's Fate?

- Navigating a Written-Off Vehicle: Your Options

- Re-Registering a Written-Off Car: Is It Possible?

- The Impact on Your Future Insurance

- When It's Not Your Fault: Understanding Your Rights

- Financed Cars and Write-Offs: A Special Consideration

- Selling a Repaired Write-Off: The Resale Reality

- Even New Cars Can Be Written Off

- Crucial Steps if Your Car is Written Off Without Insurance

- Frequently Asked Questions

- Conclusion

What Exactly is a Car Insurance Write-Off?

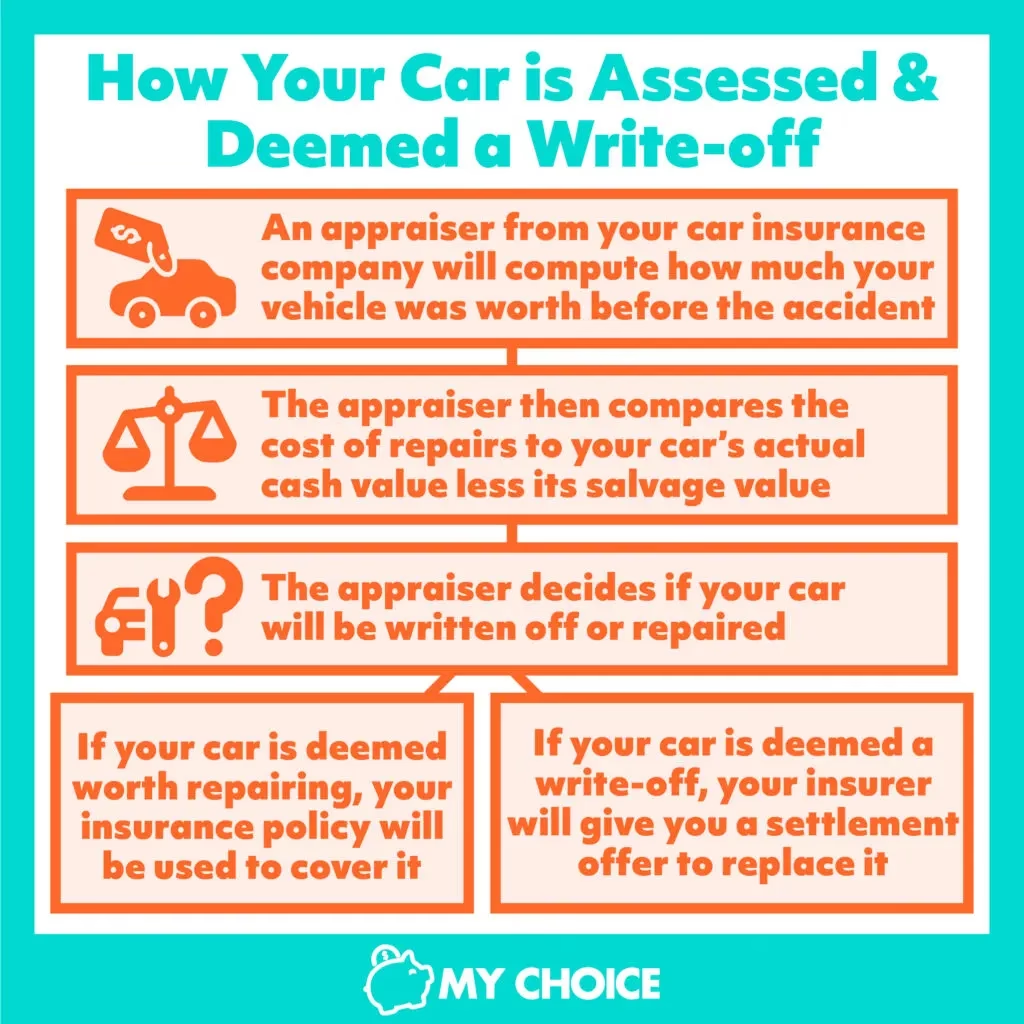

An insurance write-off, formally known as a 'total loss', occurs when your vehicle sustains such severe damage that it's either deemed unsafe to drive or the cost of repairing it far exceeds its current market value. This can stem from various unfortunate events, be it a collision, extensive water damage, fire, or even accidental mishaps. When you lodge a claim for an at-fault accident with your insurer, they dispatch an assessor or engineer to meticulously inspect the damage. The specific criteria for classifying a car as a write-off can vary slightly between different insurance providers, and the ultimate decision might sometimes come as a surprise to the car owner. However, if the insurer concludes that the repair costs would be 'uneconomical' – meaning it's cheaper to pay out the car's value than to fix it – writing the car off becomes their default course of action, regardless of how minor the damage might appear at first glance. If your insurer classifies your car as an insurance write-off, you are typically entitled to a cash payout equivalent to the vehicle's market value, contingent on you holding the appropriate level of insurance cover.

The Four Write-Off Categories Explained

Since October 2017, the UK has standardised four distinct categories for vehicle write-offs. These categories dictate what can, or cannot, be done with a damaged vehicle, ensuring public safety and preventing unroadworthy cars from returning to circulation. Understanding these categories is paramount, as they determine the future viability of your vehicle.

Here’s a breakdown of each category:

| Category | Description | Future Use |

|---|---|---|

| Category A | Beyond repair, so significantly damaged it must be crushed for scrap only. | Never to be driven again; no parts salvageable for other vehicles. |

| Category B | Extensive damage; the body shell must be crushed, but some parts may be salvaged. | Never to be driven again; specific parts may be used in other roadworthy vehicles. |

| Category S | Structural damage that requires professional repair. | Can be driven again on the road, but only after professional repair work is completed and deemed safe. |

| Category N | Non-structural damage, possibly cosmetic or electrical faults, that is uneconomical to repair. | Can be driven again on the road once all safety-related repairs are completed. No re-registration needed, but DVLA must be informed. |

Categories A and B are considered 'unrepairable' write-offs, meaning the vehicle can never return to the road. Categories S and N, however, are 'repairable' write-offs, offering a potential path for the vehicle to be back on the road once necessary repairs are completed.

Who Decides Your Car's Fate?

When your car is damaged in an accident, the power to decide its fate – whether it gets repaired or is declared a write-off – typically rests with the insurance company's assessor. It's worth taking a moment to review the fine print of your car insurance policy. You might find it stipulates that the insurer has the sole discretion to:

- Arrange for your car to be repaired.

- Provide you with a cash payment so you can arrange the repairs yourself.

- Declare your car a total loss and write it off, offering a settlement figure instead.

This means that even if you believe your car is repairable, the insurer's assessment of the economic viability of repairs often overrides your personal preference. Their decision is primarily driven by cost-effectiveness rather than the emotional attachment you might have to your vehicle.

If your car is officially declared a write-off by your insurer, its ownership legally transfers to the insurance company. In return, and depending on the specific terms of your policy, you should receive a cash payout. This 'settlement figure' is intended to be equivalent to the market value of your vehicle had it been sold in its pre-accident condition. This payout allows you to purchase a replacement vehicle.

However, what if you disagree with the insurer's assessment, or you wish to keep the car for sentimental reasons, perhaps for its parts or even a creative repurposing (like transforming it into unique furniture)? You do have options:

Challenging the Write-Off Decision

If you genuinely believe your car can be repaired economically, or if you dispute the valuation offered by your insurer, you can challenge their decision. This is a time-sensitive process, as insurers are required to notify the MIAFTR register (Motor Insurance Anti-Fraud and Theft Register) within seven days of declaring a car a write-off. Once listed on this register, reversing the decision becomes significantly more difficult.

To successfully challenge a repairable write-off assessment (Category S or N), you'll need to gather compelling evidence to demonstrate that the repair costs or the vehicle's salvage value are lower than the market value of your car. Essential evidence includes:

- Multiple quotes from reputable smash repairers detailing the actual cost to repair the vehicle to a roadworthy standard.

- Quotes from salvage yards that accurately reflect the salvage value of your specific vehicle.

- Robust evidence of your vehicle's pre-accident market value, such as comparable listings, valuation guides, or recent sales data for similar models.

It's crucial to provide this information to your insurer immediately and explicitly request that they delay reporting your vehicle to the MIAFTR register while your appeal is under review. If you remain dissatisfied with how your insurer handles your case, you can escalate your complaint through their internal dispute resolution service, and if still unresolved, to the Financial Ombudsman Service (FOS).

Keeping Your Written-Off Car

For repairable write-offs (Category N or Category S), you technically have the option to keep your vehicle. If you choose this route, the insurer will deduct the salvage value from your payout. For a Category S vehicle, you will need to re-register the car with the DVLA after it has been professionally repaired and inspected to ensure it is safe and roadworthy. For both Category S and Category N vehicles, you must report the write-off to the DVLA. Failing to inform the DVLA could result in a hefty £1,000 fine.

Even a Category B vehicle, which is extensive damage where the body must be crushed, can technically be kept for its parts. While it can never return to the road, keeping a Cat B vehicle might be worthwhile if you have a use for its components, particularly if it's a vintage, modified, or rare vehicle fitted with valuable parts.

Re-Registering a Written-Off Car: Is It Possible?

Yes, re-registering a written-off car is indeed possible, provided it falls into the repairable write-off categories (S or N). If your car was written off because it was deemed uneconomical to repair, the insurance company might offer you a payout and then sell the vehicle back to you or to an interested third party.

For a Category S vehicle – one written off due to structural damage that was uneconomical to repair – you can repair it and then apply to have it re-registered. To do this, you'll need to send the complete log book (V5C) to your insurance company. Once the settlement is complete, you will then need to apply for a free duplicate log book using form V62 after the vehicle has been repaired and passes any necessary inspections.

A repaired Category N car, which suffered non-structural damage, does not typically require re-registration, but you are still legally obligated to inform the DVLA that it was written off. You can keep hold of the original log book in this instance.

For both Category S and Category N vehicles, once the DVLA is informed and any necessary re-registration steps are completed, the car’s DVLA status will be permanently changed to 'repaired write-off'. It’s important to note that vehicles classified as statutory write-offs (Category A and B) have their Vehicle Identification Number (VIN) recorded as such, meaning they can never be re-registered or driven on public roads again.

The Impact on Your Future Insurance

Having your car declared a write-off, even if the incident wasn't your fault, is almost certainly going to impact your future car insurance premiums. Unfortunately, it's one of the most significant claims an insurer can process against your record, and it signals a higher risk to future providers.

Here’s what you can generally expect:

- Upfront Policy Payments: If you paid for your policy in full at the beginning of the term, it's highly unlikely you'll receive a refund for the remaining policy term. The policy effectively ends when the car is written off and the settlement is paid.

- Monthly Instalments: If you pay your premium via monthly instalments, you will typically be required to continue these payments until the original policy end date. Some insurance companies may offer the flexibility to transfer your existing policy to a new car you purchase, but this is entirely at the insurer’s discretion and may incur administrative fees or a revised premium.

- Future Premiums: Most insurance application processes include questions about previous claims, including whether you've ever had a car written off. You are legally obliged to provide full and accurate details. Failure to do so can invalidate any new policy you take out, leaving you uninsured. Expect your future premiums to be higher, as a write-off claim signals a greater risk to insurers. While a non-fault write-off might have a slightly less severe impact than an at-fault one, an increase is still probable.

It's vital to remember that transparency with your insurer is key. Any misrepresentation of your claims history can lead to serious consequences, including policy cancellation.

When It's Not Your Fault: Understanding Your Rights

If your car is written off as a result of an accident that wasn’t your fault, the legal framework of 'tort law' comes into play. Under this principle, you, as the injured party, have the right to claim back your losses from the driver who was at fault. This doesn't solely refer to physical injuries; it encompasses financial losses incurred due to the at-fault party's actions.

Even if you don't intend to claim on your own insurance, it's still imperative to inform them of the accident. Make it unequivocally clear that you are merely notifying them for record-keeping purposes and have no intention of making a claim through your policy. This prevents your insurer from potentially settling with the other driver's insurer without your express consent.

When your car is written off in a non-fault accident, you have several avenues to explore for recourse:

- Utilise a Credit Hire Company: This is an increasingly popular option. Instead of claiming on your own insurance, a credit hire company will arrange for a replacement vehicle for you to use while your own car is being dealt with, and will cover the cost of repairs (or the write-off settlement). They then directly claim these costs back from the insurance company of the at-fault driver. A significant advantage of this route is that you typically won't have to pay your policy excess, as your own insurance company isn't directly involved in the financial aspect of the claim.

- Claim Back Your Excess Through Their Insurer: If you opt not to use a credit hire company and instead proceed through your own insurer, you will likely need to pay your policy excess initially. However, once the claim is settled, you can pursue the at-fault driver's insurer for reimbursement of this excess. Many insurers will assist you in reclaiming your excess from the other party's insurer, so it’s always worth asking for their support.

- Small Claims Court: As a last resort, if all other avenues fail and you cannot secure compensation for your losses from the other driver or their insurer, you have the option to take the case to a small claims court. Be aware, however, that pursuing this route will incur costs, and reimbursement of these costs will depend entirely on the court’s judgment. This option should be considered carefully due to the potential for further financial outlay.

Financed Cars and Write-Offs: A Special Consideration

The situation becomes more complex if your written-off car still has outstanding finance. When a financed vehicle is deemed a total loss, your insurer is generally obligated to pay the outstanding amount directly to the financier. However, a common issue arises where there's a 'shortfall' or 'gap' between the amount your insurer pays out and the total amount still owed on your finance agreement. This is particularly prevalent with depreciation on newer cars.

This is where 'gap insurance' proves invaluable. Designed specifically for this scenario, gap insurance is a separate policy that pays the difference between your comprehensive car insurer's total loss payout and the remaining balance of your loan contract. Without gap insurance, you could find yourself in the unenviable position of continuing to pay for a car you no longer own, which can be a significant financial burden.

If the valuation offered by your insurer seems significantly below the car's true market value, it’s advisable to challenge it and negotiate for a fairer figure. However, if the discrepancy is primarily due to high interest repayments on your car finance rather than an inaccurate market valuation, you will need to directly liaise with your finance company to arrange a suitable payment plan for the remaining debt.

Selling a Repaired Write-Off: The Resale Reality

While it is possible to repair and re-register a Category S or Category N written-off vehicle, there's a significant drawback: its status as a 'repaired write-off' will severely diminish its resale value. The MIAFTR register plays a crucial role here, designed to protect consumers by making the history of such vehicles transparent.

When you decide to sell a car that has been previously written off and repaired, potential buyers will be able to access this information. The fact that a vehicle is listed on the register as a repaired write-off can have a substantial impact on how much prospective buyers are willing to pay, often leading to a much lower offer compared to a vehicle with a clean history. Transparency is key when selling such a vehicle; you are legally obliged to disclose its write-off history to potential buyers. Failure to do so could lead to legal repercussions down the line.

Even New Cars Can Be Written Off

It might seem counterintuitive, but even a relatively new vehicle can be declared a write-off. For a brand-new car, a seemingly minor scrape or dent in the paintwork could lead to it being declared a write-off by an assessor. This is because the expense of repairing and professionally painting multiple panels might, surprisingly, exceed the vehicle’s actual value, even without any serious structural damage. In such instances, the car will most likely be classified as a Category N write-off. This means it can be made roadworthy again, and you can retain ownership without the need to re-register it with the DVLA, though you are still required to report the write-off to them. A Category N car can be driven again on the road once all repairs pertaining to the vehicle’s safety have been meticulously completed.

Crucial Steps if Your Car is Written Off Without Insurance

Now, let's circle back to the critical scenario: what happens if your car is written off, and you have no insurance cover? This is a precarious position with significant financial and legal implications.

Firstly, there will be no insurance company to assess the damage, no payout to cover the vehicle's market value, and no assistance with recovery or disposal. The entire financial burden falls squarely on your shoulders. You will be responsible for:

- Repair Costs: If the car is repairable (equivalent to a Cat S or N), you will have to fund all repairs out of your own pocket. There will be no insurer to deem repairs uneconomical; the decision to repair rests solely on your financial capacity and willingness.

- Disposal Costs: If the car is beyond economic repair (equivalent to a Cat A or B), you will be responsible for arranging and paying for its safe and legal disposal. This often involves paying a salvage yard or a scrapyard to take the vehicle.

- Third-Party Damages: If the write-off was the result of an accident where you were at fault and caused damage to another vehicle or property, you would be personally liable for all those costs. This could run into thousands, if not tens of thousands, of pounds. Without third-party insurance, you face the prospect of significant debt or even legal action from the affected parties.

- Legal Consequences: Driving without at least third-party insurance in the UK is illegal and carries severe penalties, including a fixed penalty of £300 and 6 penalty points on your licence. If the case goes to court, you could face an unlimited fine and disqualification from driving. If your car is written off while uninsured, and it's discovered you were driving illegally, these penalties will be applied on top of your financial woes.

- No Replacement Vehicle: There will be no credit hire company or insurer to provide a courtesy car. You will need to arrange and pay for your own transport, adding another layer of financial strain.

In essence, being uninsured means you bear all the risks and costs associated with vehicle ownership and accidents. It's a stark reminder of why car insurance isn't just a legal requirement, but a fundamental financial protection.

Frequently Asked Questions

Navigating the aftermath of a car write-off can be complex and confusing. Here are some frequently asked questions to help clarify common concerns:

- How do companies determine a write-off?

- When you make a claim for vehicle damage with your insurer, they dispatch an assessor or engineer to inspect the damage thoroughly. Each insurance company employs different 'repair-to-value' ratios to ascertain whether it's economically viable to repair the vehicle. Essentially, they compare the estimated cost of repairs against the car's current market value. If the repair cost is deemed uneconomical, writing the car off becomes the preferred option for most insurers, irrespective of how minor the damage might superficially appear. While this decision can sometimes surprise car owners, the option to appeal and, in certain cases, retain the car despite it being written off, is available.

- What does an insurance company do with a car that's been written off?

- Vehicles classified as Category A and Category B write-offs are destined for crushing. From Category B cars, however, any safe and functional parts that can be salvaged for use in other roadworthy vehicles are removed prior to crushing.

- Will my insurance go up if my car is written off?

- Unfortunately, it is highly probable. Any previous claims on your insurance record tend to increase your future premiums, and a write-off is considered the most severe outcome following an accident. If the accident was not your fault, the impact on your premiums might be less severe, but an increase is still likely. It is absolutely crucial to always provide full and accurate details about your driving history and any previous claims when obtaining an insurance quote, as any misrepresentation can completely invalidate your policy.

- Can I buy my car back after it's been written off?

- Depending on the write-off category and the specifics of your situation, it may indeed be possible for you to buy back your vehicle from the insurer after a payout has been agreed. To explore this option, contact your insurer as early as possible in the claims process. It's highly advisable to locate and inspect the car thoroughly if feasible. Maintain continuous communication with your insurer throughout the claims process and be prepared to negotiate a fair deal for its repurchase.

- What if the write-off valuation won't cover my car finance?

- If your written-off car was purchased on finance, there might be outstanding repayments that are not fully covered by the insurer's settlement figure, leaving you in the difficult position of paying for a car you no longer possess. If the value offered by your insurer is significantly below the car’s true market value, it’s worth contacting them to dispute the valuation and negotiate a revised figure. However, if this discrepancy arises primarily from high interest repayments on your car finance rather than an inaccurate market valuation, you will need to directly liaise with your finance company to establish an arrangement for the outstanding debt.

Conclusion

The journey through a car write-off, whether insured or uninsured, is undoubtedly stressful. Understanding the categories, the decision-making process, and your rights is empowering. While a written-off car can fall into one of four categories, it's reassuring to know that, depending on the classification, you may be able to retain your vehicle and even get it back on the road, provided appropriate and safe repairs are meticulously carried out. Crucially, always remember your legal obligation to inform the DVLA if your car is written off. Failure to do so can result in a substantial fine, adding further unnecessary burden to an already challenging situation. Arming yourself with this knowledge ensures you can navigate the complexities of a write-off with greater clarity and confidence.

If you want to read more articles similar to Car Write-Offs: The UK Uninsured & Insured Guide, you can visit the Insurance category.