16/06/2008

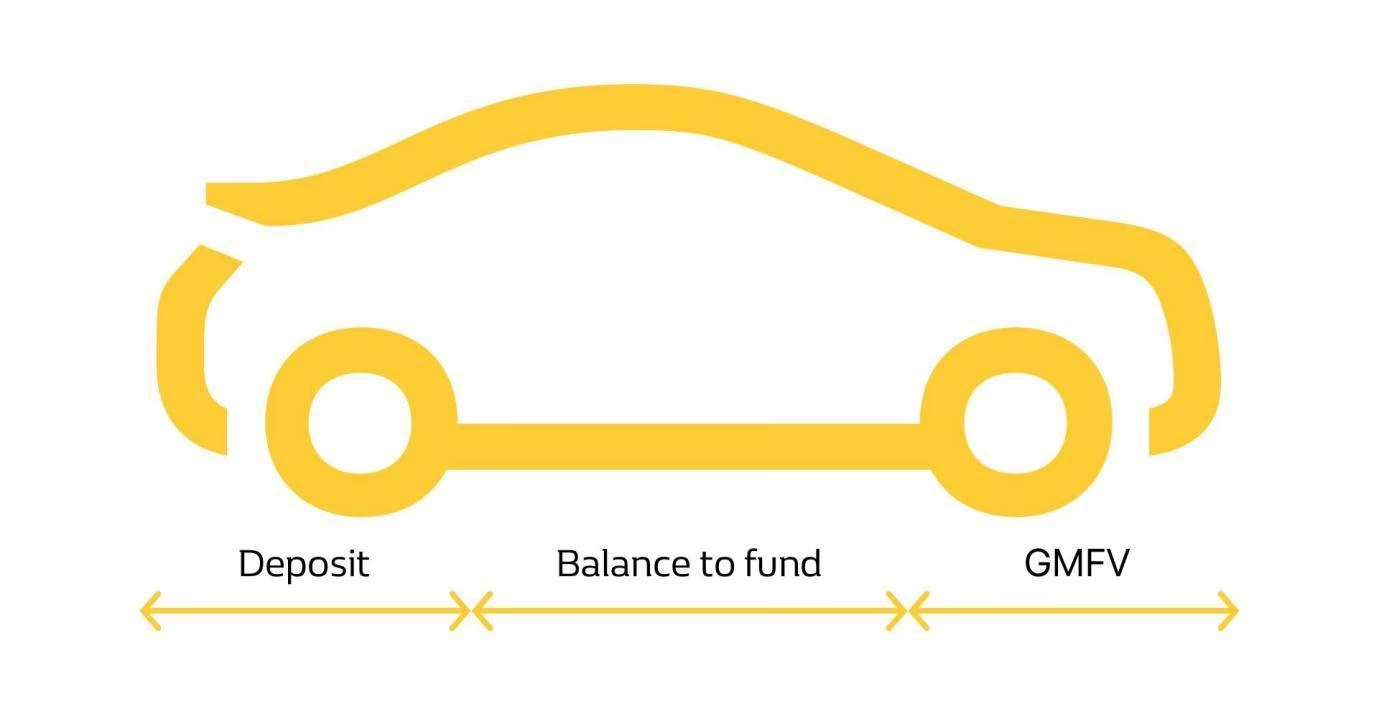

Personal Contract Purchase, or PCP, has become an incredibly popular way for motorists across the UK to finance their vehicles. Car dealers and finance companies often extol its virtues, particularly highlighting its supposed 'flexibility' and the array of 'options' available to customers when the agreement concludes. While PCP certainly offers a structured payment plan, typically spanning 36 or 48 months, it culminates in a significant final payment, often referred to as a balloon payment. Understanding these end-of-agreement options is paramount, as failing to act can lead to unexpected financial repercussions.

It's crucial to grasp that the decision-making process concerning your PCP agreement must take place after your final regular monthly payment but before this large final payment is due. Procrastination in this regard can inadvertently trigger the default option, which, as we shall explore, may not align with your financial situation or intentions.

Understanding the Final Payment: The Guaranteed Future Value (GFV)

The large final payment at the end of a PCP agreement is frequently dubbed the 'guaranteed future value' (GFV). While technically distinct from the 'balloon payment', for practical purposes, they often refer to the same amount you'd need to pay to own the car outright. Many finance providers playfully label it the 'optional final payment', implying it's a choice you can easily forgo. In reality, the opposite is true, and misinterpreting this can have severe consequences for your personal finances.

Perhaps the most critical piece of information, often overlooked or poorly explained by car dealerships, is that paying off this balloon payment is the *default* action. Unless you take specific, proactive steps to indicate otherwise, the finance company will attempt to debit this substantial sum from your bank account on the due date. Imagine the shock if you discover several thousand pounds have been unexpectedly withdrawn, or worse, if the payment bounces. A bounced payment can immediately put you in default on your loan, incurring not only a default fee from the finance company but potentially additional charges from your bank. Such an event can severely impact your credit rating and create significant financial distress.

Therefore, it is absolutely essential to make a clear decision about your intentions before the end of your PCP agreement approaches. Let's delve into the three primary options available to you, explaining what each truly entails and when they are most (and least) suitable.

Option 1: Pay Off the Balloon and Keep the Car

If you have the necessary funds available and wish to retain ownership of the vehicle, you can simply pay off the final balloon payment. A PCP agreement is fundamentally a form of Hire Purchase (HP), meaning the car technically belongs to the finance company until the entire outstanding balance is settled. Once you pay the balloon, the vehicle's title is transferred to you, and it becomes officially yours.

The primary advantage of this option is the complete freedom it grants. Once the car is yours, you are no longer bound by any mileage limits, condition clauses, or servicing requirements imposed by the finance company. You are free to sell it, modify it, or simply continue driving it as you please. This removes the stress of potential end-of-contract charges for excess mileage or damage.

Historically, some finance companies offered the option to refinance the balloon payment, effectively allowing you to take out another HP agreement to cover the final sum. While this is less common with original finance providers today, you can still explore securing a personal loan from a bank or another lender to cover the amount if you wish to keep the car but lack the immediate cash.

When to Consider Paying Off the Balloon:

| Scenario | Reasoning |

|---|---|

| You genuinely want to keep the car | The most straightforward path to ownership. |

| You have sufficient cash reserves | Avoids additional borrowing or financial strain. |

| The car is worth more than the GFV | You're gaining equity by purchasing it at a lower effective price. |

| High mileage/condition charges are anticipated | Avoids costly penalties by taking ownership. |

When This Option Is Not Ideal:

| Scenario | Reasoning |

|---|---|

| Insufficient funds without borrowing | Taking out a new loan adds interest and debt. |

| The car is worth less than the GFV | You'd be paying more than the car's market value. |

| You no longer need or want the car | Unnecessary financial commitment for a depreciating asset. |

Option 2: Give the Car Back and Claim the Guaranteed Future Value

Instead of paying the large balloon payment, you have the choice to hand the car back to the finance company after you have completed all your regular monthly payments. In this scenario, the finance company accepts the car in lieu of the final payment, as long as certain conditions have been met. They then typically sell the vehicle at auction, hoping to recoup the GFV.

The finance company's commitment to accept the car in place of the final payment, regardless of its actual market value at that time, is the 'guarantee' in Guaranteed Future Value. However, this guarantee is contingent upon your adherence to several key requirements throughout the agreement:

- Your mileage must be within the agreed-upon limit. Exceeding this will result in an excess mileage penalty, commonly around 10p per mile (or £100 for every 1,000 miles over).

- The car must possess a full manufacturer service history. Failure to have the car serviced on time, or servicing it at an unauthorised garage, can lead to significant penalties, potentially running into hundreds or even thousands of pounds.

- The car should exhibit no damage beyond what is considered 'normal wear and tear'. Any excessive damage will incur charges for 'repairs'. It's worth noting the finance company rarely carries out these repairs; they simply charge you for the theoretical reduction in the car's value at auction due to the damage. This also extends to missing items; a lost key, for instance, can result in hundreds of pounds in replacement charges.

Once the car is returned and any applicable penalties have been settled, your PCP agreement is officially concluded. It's important to differentiate this end-of-term option from voluntary termination, which allows you to hand the car back early under specific circumstances (usually having paid 50% of the total amount payable). The GFV option only applies at the scheduled end of your PCP term.

When to Consider Giving the Car Back:

| Scenario | Reasoning |

|---|---|

| The car is worth less than the GFV | You avoid paying the negative equity you'd face otherwise. |

| You no longer need a car or a replacement | A hassle-free exit from car ownership. |

| You've met all mileage/service/condition terms | Avoids additional charges. |

| You are willing to pay any associated charges | If charges are acceptable, it's a viable option. |

When This Option Is Not Ideal:

| Scenario | Reasoning |

|---|---|

| The car is worth substantially more than the GFV | You're missing out on potential equity that could be used for a new car. |

| High mileage/service/condition charges are anticipated | The penalties might make this option financially unviable. |

Option 3: Part-Exchange the Car at a Dealership

This is by far the most popular option, chosen by approximately 80% of PCP customers. For many, it's the most practical route, as they may not have the funds to pay off the balloon payment and cannot afford to be without a car if they simply hand it back to the finance company.

A common misconception is that you must return to the same dealership or even stick with the same car brand when part-exchanging. This is entirely untrue. You are free to part-exchange your vehicle at any dealership, for any make or model of car that suits your needs.

The process involves the dealership valuing your current vehicle. Simultaneously, you will need to obtain the precise settlement figure for your outstanding finance from your finance company. Often, the dealership's finance manager or salesperson will facilitate this call while you are present, ensuring you get the exact figure and due date directly. The finance company will then typically provide this in writing to the dealership.

Once you have both the dealer's valuation of your car and the exact settlement figure for your PCP, you can determine if you have any equity. For example, if your car is valued at £9,000 and your final payment (GFV) is £8,000, you have £1,000 of positive equity. This £1,000 can then be used as a deposit towards your next vehicle, reducing your new monthly payments.

Conversely, a growing number of motorists find themselves in a position of negative equity. This occurs if your car's market value is less than the GFV. If your car is valued at £7,000 but your final payment is £8,000, you have £1,000 of negative equity. In this situation, you essentially have two choices: either pay the £1,000 negative equity directly to the dealer (or the finance company, via the dealer) to clear the outstanding finance, or revert to Option 2 and give the car back to the finance company (assuming you meet their conditions). A crucial warning: some dealers might suggest rolling this negative equity into your new car finance agreement. This is a highly detrimental practice that will only inflate your new loan, leading to larger payments and potentially even greater negative equity down the line. It's almost always best to avoid this.

As part of the part-exchange, the dealer will handle the payment of your outstanding finance. It is vital to ensure that you hand over the car to the dealership at least a few days before your final payment is due. This provides sufficient time for the dealer to pay off your finance. If the dealer fails to settle the finance before your due date, the finance company will assume you are keeping the car and attempt to debit the final payment from your bank account, leading to the same issues discussed earlier.

When to Consider Part-Exchanging the Car:

| Scenario | Reasoning |

|---|---|

| You want to upgrade or change your car | A seamless transition to a new vehicle. |

| The car is worth at least the GFV or more | You can use positive equity as a deposit for your next car. |

| You are buying another car on PCP (or other finance) | Convenient way to manage the old agreement and start a new one. |

| High mileage/service/condition charges are anticipated | The dealer takes on the responsibility, potentially offsetting charges. |

When This Option Is Not Ideal:

| Scenario | Reasoning |

|---|---|

| The car is worth substantially less than the GFV | You'd have to pay significant negative equity, or it's simply not financially viable. |

| You don't need another car | Unnecessary to take on new finance if you don't require a vehicle. |

Frequently Asked Questions About PCP End-of-Agreement

What if I can't afford the balloon payment?

If you cannot afford the balloon payment, you should absolutely not let the due date pass without taking action. Your options are to either part-exchange the car (Option 3), ensuring any negative equity is managed responsibly, or to hand the car back to the finance company (Option 2), provided you meet the mileage, servicing, and condition requirements. Do not ignore the payment, as it will lead to default on your loan.

Can I change my mind after choosing an option?

Once you commit to an option, particularly if paperwork is signed or the car is handed over, it becomes legally binding. It's crucial to be certain of your decision before proceeding. Always read all documents carefully before signing.

What happens if I exceed the mileage limit?

If you return the car (Option 2) and have exceeded the agreed mileage limit, you will be charged an excess mileage penalty. This is typically a per-mile charge (e.g., 10p per mile) for every mile over the agreed allowance. These charges can quickly add up, so it's wise to monitor your mileage throughout the agreement.

Do I need a full service history?

Yes, for Option 2 (giving the car back), a full manufacturer service history is usually a strict requirement. Failure to maintain this can result in substantial penalties, as it affects the car's resale value. Even if you don't return the car, a full service history is beneficial for resale value if you choose to sell it privately or part-exchange.

What is 'normal wear and tear' versus damage?

'Normal wear and tear' refers to the expected deterioration of a vehicle through regular use, such as minor scuffs on alloys, small stone chips, or light interior wear. Damage, on the other hand, includes anything beyond this, like dents, deep scratches, cracked windscreens, or significant interior damage (e.g., torn upholstery, broken trim). Finance companies often have detailed guides on what constitutes 'normal wear and tear' – it's advisable to review these or consult with an independent inspector if you're unsure before returning the car.

Hopefully, this comprehensive guide will equip you with the knowledge needed to make the best decision for your personal circumstances when your PCP agreement reaches its conclusion. Understanding your options and acting proactively are key to a smooth and financially sound transition.

If you want to read more articles similar to Navigating Your PCP End-of-Agreement Options, you can visit the Automotive category.