20/12/2003

Hiring a car for a holiday or business trip offers fantastic flexibility, allowing you to explore at your own pace. However, the process of picking up your rental can sometimes feel like navigating a minefield of optional extras and insurance policies. One term you'll frequently encounter is 'Premium Protection'. But what exactly does it entail, and is it worth the extra cost? This comprehensive guide aims to demystify rental car protection, helping you make informed decisions and avoid unnecessary expenses.

- What is Premium Protection on a Rental Car?

- Is Protection Included in My Rental?

- Can I Purchase Protection When I Rent?

- Types of Rental Car Protection Explained

- What is SIXT Premium Protection?

- Additional Drivers and Protection

- Purchasing Protection Through Third Parties (e.g., Expedia)

- Using Credit Card Coverage for Rental Cars

- Can I Remove or Add Coverage During a Rental?

- How Much Does Car Rental Insurance Cost?

- American Express Premium Car Rental Protection: A Closer Look

- Making the Right Choice

- Frequently Asked Questions (FAQ)

- What happens if I have an accident and don't have enough coverage?

- Can my credit card cover damage to the rental car?

- What is the difference between CDW and LDW?

- Do I need to buy insurance from the rental company if my credit card covers it?

- What if the rental company charges me for damage after I return the car?

Generally speaking, 'Premium Protection' on a rental car refers to a package of optional coverages offered by the rental company that significantly reduces or even eliminates your financial responsibility for accidental damage or theft of the rental vehicle. It's designed to provide peace of mind, ensuring that if something unfortunate happens to the car, your out-of-pocket expenses are capped or entirely covered. The specifics of what's included can vary between rental companies, but it often builds upon or replaces more basic forms of coverage.

Is Protection Included in My Rental?

This is a crucial question, and the answer is often nuanced. Some rental agreements might include a basic level of third-party liability protection as a legal requirement in certain regions. However, comprehensive damage to the rental vehicle itself is rarely included as standard. You can usually find information about any included protection in the 'Mileage & Protection' or a similar step during the booking process. It's always wise to scrutinise the rental agreement details carefully.

Can I Purchase Protection When I Rent?

Absolutely. Rental companies typically offer a range of optional protection products that you can add to your rental agreement at the time of booking or when you collect the vehicle. These can include Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW), Personal Accident Insurance (PAI), and Theft Protection. You'll usually be presented with these options during the booking process or at the rental desk.

Types of Rental Car Protection Explained

Rental companies offer various optional products to cover different scenarios. Understanding these is key to choosing the right level of protection:

Loss Damage Waiver (LDW) / Collision Damage Waiver (CDW)

This is arguably the most important protection to consider. An LDW or CDW waives your financial responsibility for damage to the rental car resulting from a collision or other specified incidents, such as theft. It's crucial to understand the deductible or excess amount associated with these waivers. The rental company will state the maximum amount you'll have to pay if the car is damaged. 'Premium Protection' packages often aim to reduce this deductible to zero.

Personal Accident Coverage (PAC)

PAC provides coverage for medical expenses and sometimes accidental death or dismemberment for the driver and passengers in the event of an accident. The coverage limits and specifics can vary significantly, so it's important to check the policy details.

Third-Party Liability Protection (TPL)

This covers damage or injury you may cause to other people or their property while driving the rental car. In many countries, a basic level of third-party liability is legally mandated and might be included in the rental price. However, the limits of this included coverage might be low, and opting for higher limits through TPL is often advisable.

Roadside Assistance

While not strictly 'protection' against damage, roadside assistance can be invaluable. It typically covers services like flat tyre changes, jump-starting a battery, fuel delivery, and towing if the vehicle breaks down. Some premium packages might include enhanced roadside assistance.

SIXT, a prominent rental company, offers 'Premium Protection' as a package designed to minimise your financial responsibility for accidental damage to the rental car. This package provides enhanced peace of mind. SIXT also offers various other optional products that cater to different needs and situations you might encounter during your rental.

Additional Drivers and Protection

If you plan to have additional drivers, it's important to note that they too can benefit from the optional products and benefits purchased by the primary renter, provided they adhere to the rental agreement's terms and conditions. This includes meeting age requirements for the specific car category. Be aware that a daily charge often applies for each additional driver, and this fee can vary based on location and rental duration. Always check the applicable charges for your specific rental.

Purchasing Protection Through Third Parties (e.g., Expedia)

Booking through third-party sites like Expedia can sometimes offer a level of protection. However, it's vital to scrutinise these policies carefully. Many third-party policies may not offer a $0 financial responsibility for damage and might operate as secondary coverage. This means you'd have to claim against your personal auto insurance first. If you intend to rely on such coverage, ensure you understand all the specific terms and conditions, as they may not be as comprehensive as direct offerings from the rental company.

Using Credit Card Coverage for Rental Cars

Many credit cards offer automatic rental car insurance benefits, which can be a great perk. However, this coverage is often secondary. This means it will only kick in after you've exhausted your personal auto insurance. Furthermore, credit card coverage can have limitations on the types of vehicles covered (e.g., excluding luxury or exotic cars) or the duration of the rental. Always check the specific terms and conditions of your credit card's rental car coverage before relying on it.

Can I Remove or Add Coverage During a Rental?

Generally, no. Once you have signed the rental agreement, it is typically not possible to add or remove protection options. Therefore, it's essential to make these decisions before finalising your booking or at the rental desk before signing. Be sure you are comfortable with the chosen coverage levels for the entire rental period.

How Much Does Car Rental Insurance Cost?

The cost of car rental insurance varies significantly based on the rental company, the type of coverage selected, the duration of the rental, and your location. Over-the-counter collision insurance from rental companies can range from $20 to $50 or more per day. 'Premium Protection' packages, while costing more upfront, can often be more economical than paying for individual, lower-tier waivers, especially for longer rentals. The price is usually a daily rate, but some premium services may offer a flat fee for the entire rental period.

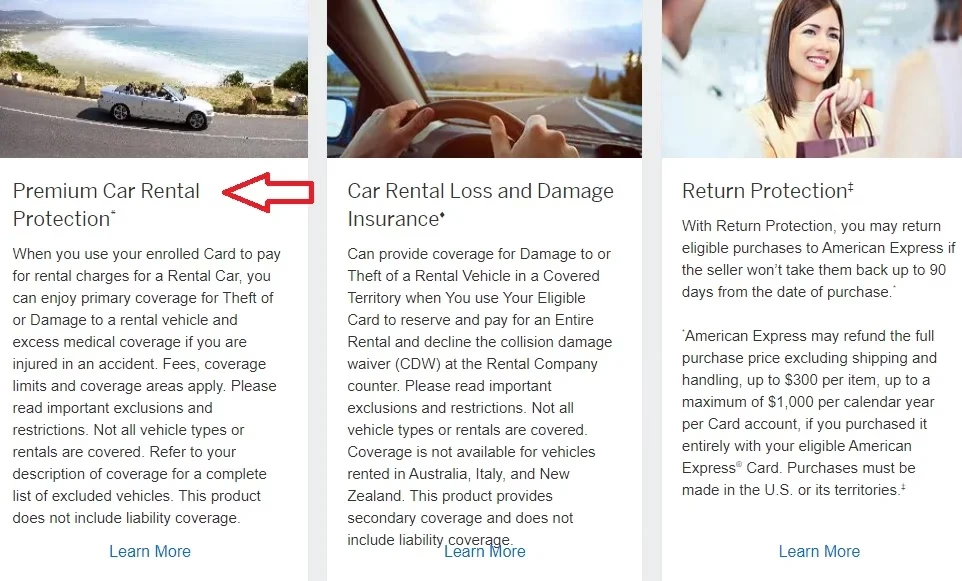

American Express offers a specific service called 'Premium Car Rental Protection'. This is a paid, optional service for eligible cardholders that provides primary coverage for damage or theft during your rental. This means you can file a claim directly with Amex without needing to go through your personal auto insurance first. It can be a more affordable alternative to the rental company's own collision coverage, often costing around the same as a few days of the rental company's coverage but applied to the entire rental period.

- Primary Coverage: Files claims directly, bypassing your personal insurance.

- Cost-Effective: A one-time fee for the entire rental period (up to 42 days, or 30 for Washington State residents), often cheaper than daily rates.

- No Deductible: Typically no excess or deductible to pay.

- Two Levels of Coverage: Offers different tiers of protection, with higher limits for damage, theft, accidental death, and dismemberment.

- Global Use: Valid worldwide, with exceptions for certain countries (Australia, Ireland, Israel, Italy, Jamaica, New Zealand).

While some American Express cards offer standard car rental benefits, these are usually secondary and provide lower coverage limits than the Premium option. The Premium service offers a significant upgrade in terms of coverage level and the direct, primary nature of the claims process.

Enrolling in Amex Premium Car Rental Protection can be a smart move if:

- You don't have personal auto insurance.

- You want to avoid making a claim on your personal policy, which could increase your premiums.

- You find the rental company's daily coverage rates prohibitively expensive.

However, if you already have robust primary coverage through your personal auto insurance or another premium credit card (like the Chase Sapphire Reserve), the additional cost of Amex Premium Protection might be unnecessary.

Making the Right Choice

When deciding on rental car protection, consider the following:

- Your Existing Insurance: Check your personal auto insurance policy and credit card benefits thoroughly. Understand if your coverage is primary or secondary and what its limits are.

- The Rental Company's Offerings: Compare the cost and coverage of the rental company's 'Premium Protection' package against the cost of individual waivers and your existing insurance.

- Rental Duration and Car Type: For longer rentals, a fixed-fee premium package is often more economical. Also, consider the value of the car you are renting.

- Your Risk Tolerance: How much financial risk are you comfortable taking on? 'Premium Protection' offers the lowest risk.

Frequently Asked Questions (FAQ)

What happens if I have an accident and don't have enough coverage?

If you don't have adequate protection, you will be liable for the full cost of the damage to the rental car, as well as any third-party damages, up to the value of the vehicle and beyond, depending on the rental agreement and local laws. This can include repair costs, loss of use (the rental company's lost income while the car is being repaired), and administrative fees.

Can my credit card cover damage to the rental car?

Yes, many credit cards offer rental car damage coverage, but it's often secondary to your personal auto insurance and may have limitations on car types or rental durations. Always verify the specific terms with your card issuer.

What is the difference between CDW and LDW?

CDW (Collision Damage Waiver) and LDW (Loss Damage Waiver) are often used interchangeably. Both are waivers that relieve you of financial responsibility for damage to the rental vehicle, typically excluding theft. Some companies may distinguish them, with LDW potentially including theft coverage, but in practice, they serve a very similar purpose.

Do I need to buy insurance from the rental company if my credit card covers it?

If your credit card provides primary coverage with sufficient limits and no exclusions that apply to your rental, you might be able to decline the rental company's collision damage waiver. However, if your credit card coverage is secondary, you'll likely need to use your personal auto insurance first, or purchase the rental company's coverage to avoid going through your insurer.

What if the rental company charges me for damage after I return the car?

If you have purchased comprehensive protection (like 'Premium Protection' or CDW/LDW with a low/zero deductible), the rental company should not charge you for covered damages. If they do, refer to your rental agreement and the terms of your protection plan. Keep all documentation, including the final rental agreement and any damage reports, to contest unwarranted charges.

Navigating rental car protection can seem daunting, but by understanding the different types of coverage, your existing insurance, and the specific offerings from rental companies like SIXT or credit card providers like American Express, you can make an informed decision that protects both your wallet and your peace of mind. Always read the fine print and ask questions if you're unsure!

If you want to read more articles similar to Rental Car Protection Explained, you can visit the Automotive category.