28/11/2014

Being involved in a car accident can be a stressful experience, and one of the most common questions policyholders have is whether to opt for a cash settlement or have their vehicle repaired. While the appeal of a quick payout is understandable, the decision isn't always straightforward. Insurance companies have specific criteria they consider, and understanding these can empower you to make the best choice for your situation. This article delves into the intricacies of cash settlements following a motor vehicle collision, outlining the factors that influence the insurer's decision and the advantages and disadvantages of each option.

Understanding Your Insurer's Decision-Making Process

When your vehicle has been damaged in a collision, your insurance provider will assess the situation to determine the most appropriate course of action. While you might prefer a cash settlement, the insurer ultimately retains the right to either repair or replace the damaged parts of your vehicle. Several key considerations guide their decision:

Extent of the Damage

The severity of the damage is a primary factor. Minor cosmetic damage might be more amenable to a cash settlement, allowing you to arrange repairs yourself. However, if the damage is significant, particularly if it affects the structural integrity or safety of the vehicle, the insurer will likely opt for direct repairs or replacement to ensure the car is restored to a safe and roadworthy condition.

Ownership of the Vehicle

Whether you own your vehicle outright or if it is leased or financed plays a crucial role. If your car is leased or financed, the leasing company or lender will be listed as a co-payee on any insurance claim. This means you cannot simply take a cash payout and forgo repairs, as you are contractually obligated to maintain the vehicle in good condition. The insurer will ensure that any repairs necessary to uphold the terms of your lease or loan agreement are carried out.

Optional Physical Damage Coverages

Your decision to keep optional physical damage coverages on your policy can also influence the settlement. If you choose not to have repairs made to your damaged vehicle, your insurer might remove these optional coverages from your policy. This would leave you without protection against further damage if your vehicle is involved in another incident down the line. Many insurers require proof of repairs, such as an invoice from a reputable repair shop and photographs of the vehicle from all angles, to keep your policy active and unchanged.

When Insurers Might Not Allow a Cash Payout

There are specific circumstances where an insurer will almost certainly deny a cash settlement request. These often relate to safety and functionality:

- Compromised Vehicle Safety: If the damage is such that it compromises the overall safety of the vehicle, a cash settlement is unlikely. The insurer has a responsibility to ensure vehicles on the road are safe.

- Damage to Safety-Related Components: Damage to critical safety parts, such as lights, tires, seatbelts, or braking systems, means the vehicle is not roadworthy. Driving a vehicle with such damage can lead to fines and further safety risks.

- Complex Sensor Systems: Modern vehicles are equipped with sophisticated sensor systems for features like automatic parking, blind-spot monitoring, and adaptive cruise control. Following a collision, these sensors often require expert testing and recalibration to ensure they function correctly. If the damage affects these systems, the insurer will prioritise ensuring they are properly repaired and calibrated, making a cash settlement improbable.

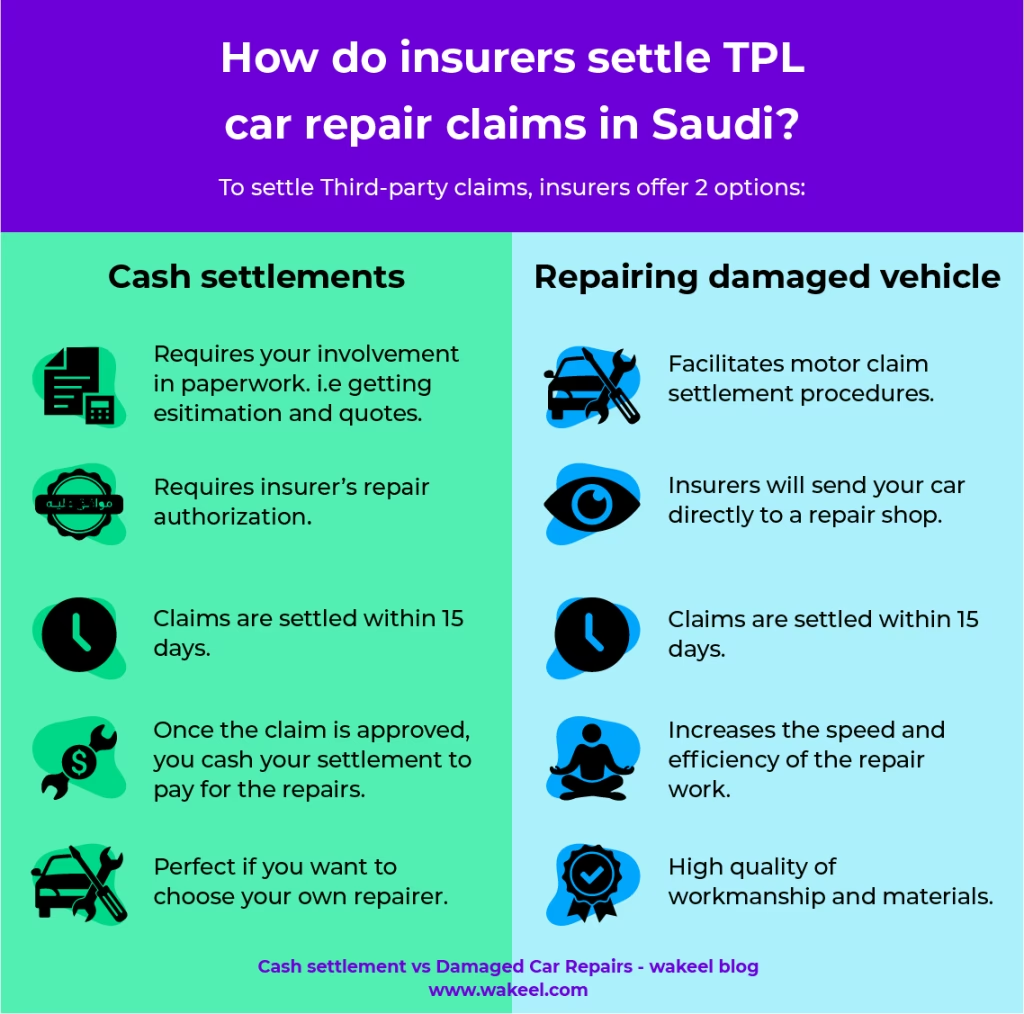

Auto Repair: The Pros and Cons

Opting for auto repair offers a clear path to restoring your vehicle. Here's a breakdown of the advantages and disadvantages:

Pros of Auto Repair:

- Restoration of Vehicle Functionality: Repairs ensure your vehicle is returned to its pre-accident condition, addressing both visible damage and any underlying mechanical issues. This allows for safe and continued use of your car.

- Retained Resale Value: A vehicle that has been properly repaired generally holds a higher resale value compared to one with unrepaired damage, even if a cash settlement was received. A history of professional repairs can be a selling point.

- Insurance Coverage Utilisation: If you have comprehensive insurance, the costs of repairs are often covered, significantly reducing your out-of-pocket expenses. This is particularly beneficial if you intend to keep your current vehicle.

Cons of Auto Repair:

- Time-Consuming Process: Depending on the extent of the damage, repairs can take a considerable amount of time. This can lead to prolonged periods without your vehicle, causing inconvenience, especially if you rely on it for daily commutes or essential tasks.

- Potential for Diminished Future Value: While professional repairs restore functionality, some argue that a vehicle that has been in an accident, even if repaired, may still suffer from a diminished resale value compared to an identical model that has never been damaged.

Cash Settlement: The Pros and Cons

A cash settlement offers a different set of benefits and drawbacks:

Pros of Cash Settlement:

- Flexibility in Vehicle Replacement: A cash settlement provides you with the freedom to choose a replacement vehicle that best suits your needs and budget. This is ideal if your current vehicle has sentimental value or if you're keen to explore different models or makes.

- Expedited Process: Compared to the often lengthy repair process, a cash settlement can offer a quicker resolution. You receive the funds promptly, allowing you to move forward with purchasing a new vehicle or arranging alternative transportation.

- Avoidance of Potential Future Issues: Some individuals prefer a cash settlement to avoid any potential long-term issues that might arise from repairs, such as hidden damage or lingering mechanical problems, despite advancements in repair techniques.

Cons of Cash Settlement:

- Out-of-Pocket Expenses: The settlement amount may not always fully cover the cost of a comparable replacement vehicle. You might need to contribute additional funds from your own pocket, depending on the settlement value and current market prices.

- Emotional Attachment: For some, letting go of a damaged vehicle, especially one with sentimental value, can be emotionally challenging. A cash settlement necessitates parting with your current car.

Negotiating Your Cash Settlement

If a cash settlement is the route you wish to take, understanding how to negotiate effectively with your insurance company is crucial. The goal is to secure fair compensation that accurately reflects the loss or damage sustained.

Key Steps in Negotiation:

- Thorough Research: Before engaging with your insurer, understand the true value of your claim. Obtain multiple repair estimates from reputable garages. Consider not only the cost of repairs but also the potential cost of replacing the vehicle if it's deemed a total loss. Document all expenses, including any temporary transportation costs you incur.

- Determine Your Desired Settlement Value: Based on your research, establish a clear figure for what you believe constitutes a fair settlement. This should encompass all aspects of the damage and the costs associated with returning your vehicle to its pre-incident condition. Note that insurance policies typically cover property damage, not emotional distress or inconvenience.

- Follow the Claims Process: It's generally advisable not to request a cash settlement from the outset. Instead, allow the insurer to proceed with the standard claims process, which involves obtaining repair estimates and authorising the necessary work. This ensures the claim is fully documented and quantified. Once estimates are being authorised, you can then consider requesting a cash settlement.

- Understanding Deductions: Be aware that insurers may deduct VAT from estimates if you are not VAT registered, and 'provisional sums' (costs that may or may not be incurred) are also typically excluded from advance payments. Insurers may also attempt to make other deductions based on various justifications.

- Don't Accept the First Offer: Insurance companies often start with a lower settlement offer. Use this as a starting point for negotiation, armed with your documented repair costs and market research.

- Seek Professional Assistance: If you feel overwhelmed or that your claim is not being handled fairly, consider engaging a loss assessor. These professionals act in your best interest and have the expertise to negotiate with insurers on your behalf.

- Get a Written Agreement: Once a settlement is agreed upon, ensure you receive a written agreement detailing the amount and terms. This serves as legal protection and prevents future disputes.

When to Escalate Your Complaint

If you are unhappy with the settlement offered or how your claim has been handled, you have the right to complain. Start by formally writing to your insurance company. If the issue remains unresolved, you can escalate your complaint to the Financial Ombudsman Service, which provides a free and independent dispute resolution service.

Typical Claim Settlement Times

The time it takes to settle an insurance claim can vary significantly. Simple claims might be resolved within a week, while complex cases with extensive damage could take 12 months or longer. Factors influencing this timeline include the complexity of the damage, the specifics of your policy, and the promptness of your communication and documentation submission.

Ultimately, the decision between a cash settlement and repairs rests on a careful evaluation of your circumstances, the extent of the damage, and your personal preferences. Understanding these factors and knowing your rights as a policyholder will help you navigate the claims process effectively and achieve a satisfactory outcome.

Frequently Asked Questions:

Can I use a cash settlement for car repairs or to buy a different car?

Yes, generally you can use a cash settlement for either car repairs or to purchase a replacement vehicle. The funds are intended to compensate you for the loss or damage to your vehicle, giving you the flexibility to decide how best to use that compensation.

What happens if the cash settlement isn't enough to repair my car?

If the cash settlement offered by your insurer is less than the actual cost of repairs, you have a few options. You can negotiate with the insurer, providing further evidence of repair costs. Alternatively, you may choose to cover the difference yourself or consider if the vehicle is a total loss and use the settlement towards a replacement vehicle.

Can my insurer force me to take a cash settlement?

In most cases, no. While your insurer has the right to determine the method of settlement (repair, replacement, or cash), they typically cannot force you to accept a cash settlement if you prefer repairs, provided the repairs are deemed necessary and feasible by them.

What if my car is leased and damaged?

If your leased car is damaged, the insurance company will typically coordinate with the leasing company. The payout for repairs will often go directly to the leasing company or an approved repairer to ensure the terms of the lease agreement are met. You generally won't be able to opt for a cash settlement in this scenario without the leasing company's agreement.

Do I need to get my car repaired if my insurer offers a cash settlement?

You are not obligated to get your car repaired if your insurer offers a cash settlement. However, if you choose not to repair the vehicle, be aware that your insurance coverage for physical damage might be affected, and the vehicle's resale value could be lower.

If you want to read more articles similar to Car Accident Cash Settlements: Your Options, you can visit the Automotive category.