05/07/2009

Experiencing a car crash can be a stressful and disorienting event. Beyond the immediate shock and potential for injuries, the aftermath often involves dealing with vehicle damage. Understanding what happens to your car after a collision, and what steps you should take, is crucial for a smooth recovery process. This article will guide you through the typical scenarios and essential actions following a car accident, focusing on the impact on your vehicle and how to navigate the repair and insurance landscape.

- Immediate Aftermath: Assessing the Damage

- The Role of Insurance

- Types of Vehicle Damage and Their Implications

- Repair Options

- When is a Car a Total Loss?

- What if the Other Party is at Fault?

- Frequently Asked Questions

- Q1: How long does it take to get a car repaired after an accident?

- Q2: What happens if my car is not drivable after a crash?

- Q3: Can I claim for loss of earnings if I can't use my car for work?

- Q4: What should I do if I disagree with the insurance assessor's valuation?

- Q5: Do I have to use the garage recommended by my insurance company?

- Conclusion

Immediate Aftermath: Assessing the Damage

The very first moments after a crash are critical. While ensuring everyone's safety is paramount, a preliminary assessment of the vehicle's condition can provide valuable information. Even minor-looking dents or scratches could conceal more significant underlying structural or mechanical damage. Look for:

- Visible exterior damage: Dents, scratches, broken lights, damaged bumpers, and compromised body panels.

- Fluid leaks: Check under the car for any signs of leaking oil, coolant, transmission fluid, or brake fluid. This is a significant indicator of potential mechanical failure.

- Tyre and wheel damage: Bent rims, deflated tyres, or damage to the suspension components connected to the wheels.

- Operational issues: If it's safe to do so, try to start the engine. Listen for unusual noises. Check if the steering feels normal, and if the brakes are responsive. Never drive a vehicle that exhibits severe operational issues, such as compromised steering or braking, as this can lead to further accidents.

The Role of Insurance

Your car insurance policy is designed to cover damages resulting from accidents. The process typically involves:

Reporting the Incident:

You will need to report the accident to your insurance provider as soon as possible. Most policies have a time limit for reporting, so don't delay. You'll likely need to provide details of the accident, including the date, time, location, a description of what happened, and information about any other parties involved.

The Claims Process:

Once reported, your insurer will assign a claims handler. They will likely arrange for an assessor to inspect the damage to your vehicle. This assessor will determine the extent of the damage and estimate the cost of repairs.

The assessor's report will be used to generate an estimate for the repairs. You may have the option to choose your preferred repair garage, or your insurer might have a network of approved repairers. It's important to understand that your insurer will only authorise repairs that are deemed necessary and reasonable based on the assessor's findings. You might also be responsible for paying an excess, which is a fixed amount you pay towards the repair cost before your insurance covers the rest.

Types of Vehicle Damage and Their Implications

The nature and severity of the damage can vary significantly:

| Type of Damage | Description | Potential Implications |

|---|---|---|

| Cosmetic Damage | Superficial scratches, minor dents, scuffs on bumpers. | Primarily affects appearance. Usually covered by insurance if part of a larger claim. |

| Structural Damage | Compromised frame, chassis, or body integrity due to impact. | Can affect the vehicle's safety and handling. May require extensive and costly repairs. Can be a safety hazard if not repaired properly. |

| Mechanical Damage | Damage to engine, transmission, suspension, steering, or braking systems. | Affects the vehicle's drivability and safety. Requires expert diagnosis and repair. |

| Electrical Damage | Damage to wiring harnesses, sensors, ECUs, or lighting systems. | Can lead to a wide range of issues, from warning lights to complete system failures. Modern cars are heavily reliant on electronics. |

Repair Options

Once the damage is assessed and authorised by your insurer, you'll need to decide on the repair approach:

Approved Repairers:

Using your insurer's approved repairers often streamlines the process. These garages typically have established relationships with insurers, and the repair work is often guaranteed for a period.

Independent Garages:

You have the right to choose your own garage. However, if you choose an independent garage, you may need to manage the payment process more closely with your insurer. Ensure the independent garage is reputable and has the necessary expertise.

DIY Repairs:

For very minor cosmetic issues, some owners might consider DIY repairs. However, for anything beyond superficial scratches, it's strongly recommended to use professional services, especially if the damage affects the vehicle's safety or structural integrity. Safety should always be the primary concern.

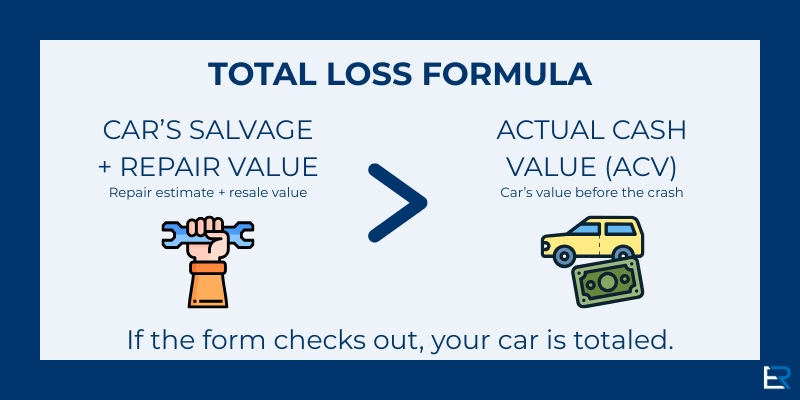

When is a Car a Total Loss?

In some cases, the cost of repairing the damage may exceed the vehicle's market value. This is known as a 'write-off' or 'total loss'. Your insurer will determine this based on their assessment and the cost of repairs. There are different categories of write-offs:

- Category A (Scrap): The vehicle is severely damaged and must be scrapped. It cannot be repaired or put back on the road.

- Category B (Break): The vehicle's structure is significantly damaged, but some parts can be salvaged for reuse. The shell must be scrapped.

- Category C (Repairable): The vehicle has been declared a total loss by the insurer, but it can be repaired. The owner can buy it back from the insurer.

- Category D (Repairable): Similar to Category C, but the damage is less severe.

If your car is declared a total loss, your insurer will typically pay you the market value of the vehicle before the accident, minus your excess. You may then have the option to buy the damaged vehicle back from them.

What if the Other Party is at Fault?

If the accident was not your fault, you would typically claim against the other driver's insurance. This process can sometimes be more complex, and it's advisable to gather as much information as possible at the scene, including the other driver's details, insurance information, and any witness statements. Your own insurer may be able to assist you with a 'knock-for-knock' agreement or by managing the claim on your behalf.

Frequently Asked Questions

Q1: How long does it take to get a car repaired after an accident?

The timeframe can vary greatly depending on the severity of the damage, the availability of parts, and the workload of the repair garage. Minor repairs might take a few days, while significant structural damage could take weeks or even months.

Q2: What happens if my car is not drivable after a crash?

If your car is not drivable, your insurance policy may cover the cost of towing it to a repair garage or your home. Check your policy documents for details on recovery and towing assistance.

Q3: Can I claim for loss of earnings if I can't use my car for work?

In some cases, if the accident was not your fault, you may be able to claim for associated losses, which could include loss of earnings if your car is essential for your work. This is usually handled through the claims process with the at-fault party's insurer.

Q4: What should I do if I disagree with the insurance assessor's valuation?

If you believe the assessor's valuation of the damage or the vehicle's market value is incorrect, you should provide your insurer with evidence to support your claim. This could include quotes from other reputable repair garages or evidence of your vehicle's recent market value.

Q5: Do I have to use the garage recommended by my insurance company?

Generally, you have the right to choose your own repairer. However, using an insurer-approved garage can often simplify the process. If you choose an independent garage, discuss the payment and repair authorisation process with your insurer beforehand.

Conclusion

Dealing with car damage after a crash is an inevitable part of motoring for many. By understanding the steps involved, from immediate assessment to navigating insurance claims and repair options, you can approach the situation with greater confidence. Always prioritise safety, keep thorough records, and communicate clearly with your insurance provider to ensure your vehicle is restored to its pre-accident condition as safely and efficiently as possible. Remember, your vehicle's safety and your own well-being are paramount.

If you want to read more articles similar to Car Damage After a Crash: What to Do, you can visit the Repair category.