23/05/2021

The automotive industry, long a bastion of traditional engineering and manufacturing, is currently undergoing a seismic transformation. What was once primarily about building and selling cars is rapidly evolving into a complex web of interconnected services and technologies, fundamentally changing how we perceive and interact with personal transport. From the emergence of ride-sharing platforms that have profoundly impacted conventional taxi and rental car sectors, to the burgeoning concept of mobility-as-a-service (MaaS), the landscape is shifting at an unprecedented pace. This disruption isn't just about new vehicles; it's about a complete redefinition of the automotive ecosystem, which has multiplied exponentially, welcoming a host of new players and specialisations.

The Multiplied Automotive Landscape

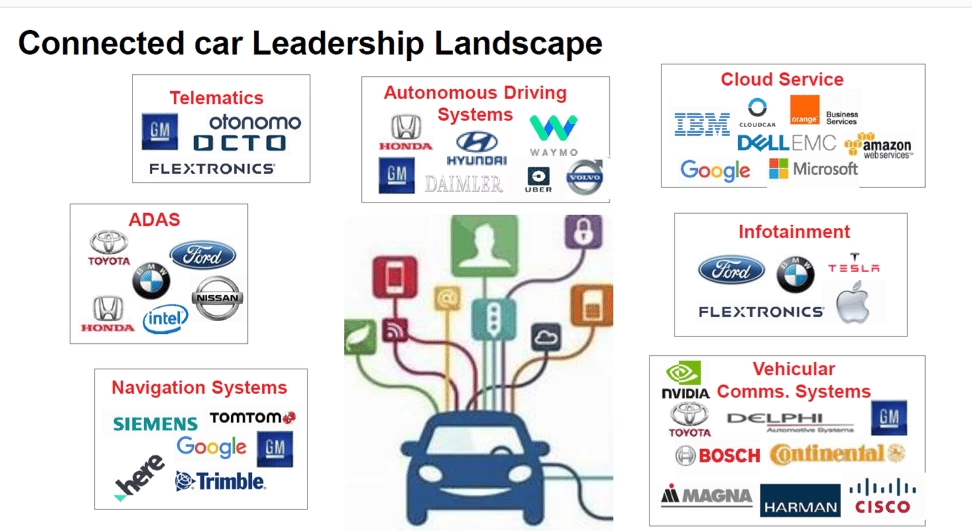

For decades, the automotive industry was largely dominated by a relatively small number of well-established vehicle manufacturers and their 'Tier 1' suppliers, often concentrated in traditional automotive hubs like Detroit. However, this insular structure has fractured and expanded dramatically. The automotive ecosystem has multiplied, embracing thousands of new entities, from nimble tech startups to vast software corporations, all contributing to solve the myriad problems and unlock the vast opportunities presented by the next generation of vehicles.

This expansion is evident in the geographical shift of innovation. While Detroit remains a key player, Silicon Valley has emerged as a crucial centre for automotive development, particularly in areas like autonomous driving. This reflects the industry's increasing reliance on advanced technologies such as cloud computing, artificial intelligence (AI), sophisticated networking, and powerful data processing. Startups from across the globe are now pitching solutions that range from highly specialised components, like advanced sensors and mapping systems, to groundbreaking software applications designed to track driver emotions and alertness, or machine learning algorithms to optimise route planning and road conditions.

This influx of diverse expertise means that the automotive supply chain is no longer a linear progression from raw materials to a finished car. Instead, it's a dynamic, multi-directional network where software developers, data scientists, cybersecurity experts, and urban planners are just as critical as traditional component manufacturers. The sheer breadth of problems to be solved, from ensuring the safety of autonomous systems to managing vast amounts of data, has opened doors to innovators from sectors previously unconnected to the automotive world.

New Components for a Smarter Ride

The innovation occurring within autonomous and connected vehicles naturally demands an entirely new generation of parts and systems, many of which were unimaginable just a few years ago. The traditional mechanical and electrical components are now complemented, and often superseded, by sophisticated digital and sensory hardware. This rapid evolution has significantly broadened the list of essential components within a vehicle, consequently expanding the number of vendors within the automotive supply chain.

Consider the rise of 'smart' mirrors, which integrate cameras, displays, and advanced driver-assistance systems (ADAS) to provide enhanced visibility and information. Beyond this, technologies like LiDAR (Light Detection and Ranging) systems, crucial for creating highly accurate 3D maps of a vehicle's surroundings, and an array of sophisticated sensors (radar, ultrasonic, cameras) are becoming standard. These aren't just add-ons; they are fundamental to how autonomous vehicles perceive and interact with their environment. Each of these new technologies requires specialised manufacturing, integration, and ongoing software support, bringing a host of new companies into the fold.

The demand for these cutting-edge components means that suppliers must not only deliver hardware but also integrate seamlessly with complex software ecosystems. This shift is driving a need for greater modularity and interoperability, as vehicle manufacturers look to combine the best solutions from a diverse range of suppliers. The days of a few monolithic suppliers providing all major sub-systems are giving way to a more fragmented yet highly specialised network.

Emerging Services and Redefined Ownership Models

As the way we travel from point A to point B undergoes a radical change, an entirely new ecosystem of services is emerging, creating novel business opportunities. Imagine a future where shared, autonomous vehicles are the norm. This scenario presents unique challenges and, crucially, solutions. For instance, who will ensure the cleanliness and readiness of a robo-taxi after a passenger's journey? This seemingly minor detail opens up a market for 'on-the-go' cleaning and sanitisation services, allowing vehicles to be maintained while in transit, maximising their uptime.

Furthermore, the very concept of vehicle maintenance is being revolutionised. Rather than an individual driver needing to schedule an appointment and physically take their car to a garage, future autonomous vehicles could drive themselves to service centres for routine checks, repairs, or even refuelling. This 'self-servicing' capability would eliminate queues, reduce inconvenience for owners, and allow for far more efficient fleet management for shared vehicle operators. Predictive maintenance, driven by real-time data from the vehicle, will become standard, allowing issues to be addressed proactively before they become major problems.

Beyond services, the fundamental model of car ownership is undergoing a profound shift. The traditional model of individual ownership, where a car sits idle for 95% of its lifespan, is being challenged by the rise of shared mobility models. As autonomous fleets become more widespread, many individuals, particularly in urban areas, may opt to share vehicles or subscribe to mobility services rather than owning a car outright. This shift has significant implications for vehicle utilisation. If cars are on the road for significantly longer hours each day, their lifespan may actually decrease, not due to wear and tear from a single owner, but from constant, high-intensity use. This, in turn, impacts the durability requirements for parts and the frequency of maintenance, shifting from periodic checks to continuous, data-driven monitoring.

The Unprecedented Role of Data

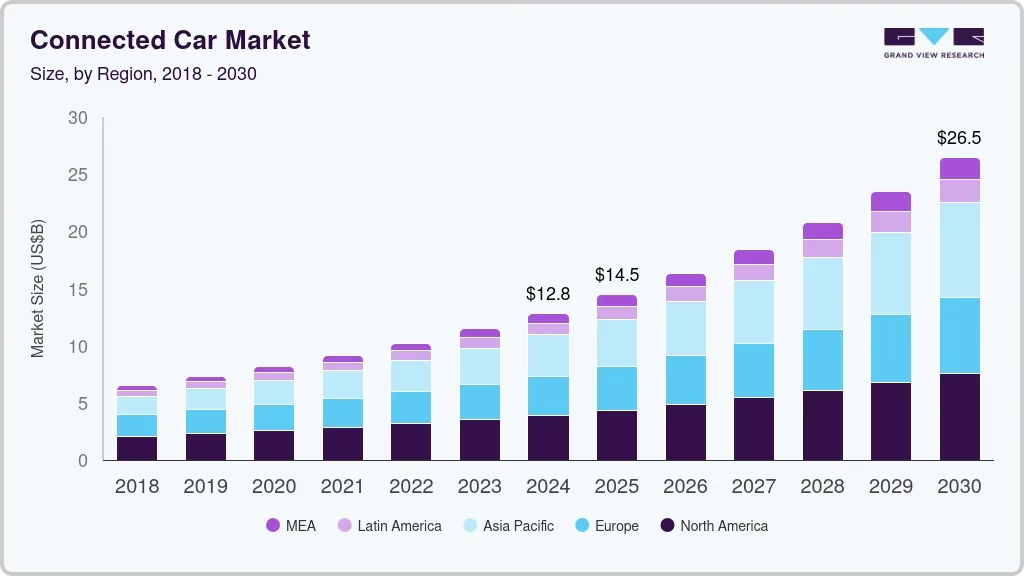

At the heart of this evolving automotive ecosystem lies data, which has become the lifeblood of modern vehicles and the services built around them. The sheer volume of data generated and consumed by autonomous cars is staggering, with some estimates suggesting up to 0.75 GB per second. This 'data deluge' is driven by a multitude of integrated systems: telematics for vehicle tracking and diagnostics, sophisticated voice recognition for in-car controls, augmented reality displays providing contextual information, drive recorders capturing every moment, and vehicle-to-vehicle (V2V) communications enabling cars to 'talk' to each other and infrastructure.

This exponential growth in data presents both immense opportunities and significant challenges. For instance, while data storage might have once been an afterthought, it is now a critical component of the automotive supply chain. The ability to efficiently capture, preserve, access, and transform vast quantities of data at lightning speed is paramount for the safe and effective operation of autonomous systems. This raises fundamental questions that the industry is grappling with:

- Who legally owns the vast amounts of data generated by a vehicle?

- What specific data points are truly necessary to capture and store for operational, legal, and diagnostic purposes?

- How much data needs to be stored, and for how long, given regulatory requirements and the pace of technological change?

- How can this data be secured against cyber threats and privacy breaches?

These questions are not merely technical; they have profound implications for business models, regulatory frameworks, and consumer trust. Companies that can effectively manage, analyse, and leverage this data will be at a significant advantage in the competitive mobility market.

The transformation of the automotive industry, while disruptive, also presents an abundance of opportunities for innovation and growth. For established players, the key is to embrace this change rather than resist it. This means collaborating with the plethora of emerging startups, each bringing specialised knowledge and agile development capabilities to the table. For example, the market for 'smart mirror' suppliers alone boasts dozens of companies, each with varying levels of integration with ADAS. While consolidation is inevitable as the market matures and true leaders emerge, working with this diverse ecosystem in the interim is crucial for staying at the forefront of technological advancement.

Buyers in this evolving landscape will increasingly demand modularity, allowing them to integrate best-in-class components and software from different vendors, rather than being locked into proprietary systems. This fosters innovation and competition, ultimately benefiting the end-user. The ability to adapt quickly, form strategic partnerships, and invest in nascent technologies will define success in this new era.

Traditional Automotive vs. Evolving Automotive Ecosystem

To better understand the scale of this transformation, consider the stark differences between the traditional and evolving automotive landscapes:

| Feature | Traditional Automotive | Evolving Automotive Ecosystem |

|---|---|---|

| Key Players | OEMs, Tier 1 Suppliers (established, often geographically concentrated) | OEMs, Tier 1s, Tech Startups, Software Firms, Data Specialists, Infrastructure Providers, Service Operators (diverse, global) |

| Primary Focus | Vehicle Manufacturing & Sales, Performance, Safety | Mobility Solutions, Data Management, Service Provision, User Experience |

| Core Technologies | Mechanical Engineering, Electrical Systems, Internal Combustion Engines | AI, Sensors (LiDAR, Radar), Cloud Computing, Connectivity (5G, V2V), Software Algorithms, Electric Powertrains |

| Ownership Model | Individual Ownership, Purchase-based | Individual Ownership, Shared Fleets, Subscription Models, On-Demand Services |

| Supply Chain | Linear, Hierarchical, Focus on Parts Manufacturing | Interconnected, Collaborative, Global, Focus on Hardware, Software, & Data Solutions |

| Maintenance | Scheduled, Manual, Reactive | Predictive, Autonomous (self-driving to garage), On-Demand, Data-driven |

Frequently Asked Questions (FAQs)

- What is 'Mobility-as-a-Service' (MaaS)?

- MaaS is an integrated, on-demand transportation concept that combines various forms of transport (e.g., public transport, ride-sharing, car rentals, bike-sharing) into a single, seamless service accessible via a digital platform. The goal is to provide users with customised, flexible, and often subscription-based mobility solutions, reducing the need for private car ownership.

- How will car ownership change in the future?

- Car ownership is likely to evolve significantly. While traditional ownership will persist, especially in rural areas, there will be a strong shift towards shared models, fractional ownership, and subscription services in urban environments. Many individuals may choose to access a car only when needed, rather than owning one outright, driven by cost, convenience, and environmental considerations.

- Will traditional car manufacturers become obsolete?

- Not necessarily, but their role will profoundly transform. Traditional manufacturers will need to evolve from simply building cars to becoming comprehensive mobility providers. This involves embracing new technologies, partnering with tech companies, and potentially offering their vehicles as part of larger shared fleets or subscription services. Their expertise in large-scale manufacturing and safety remains invaluable, but it must be combined with software and service capabilities.

- What new jobs will emerge in this evolving ecosystem?

- The transformation will create a wealth of new job opportunities. These include roles for data scientists, AI and machine learning engineers, cybersecurity specialists, urban planners focused on smart cities, fleet managers for autonomous vehicle operations, UX/UI designers for mobility apps, and specialists in vehicle-to-everything (V2X) communication. There will also be a continued need for skilled technicians capable of maintaining complex, high-tech vehicles.

- How will data privacy and security be handled in autonomous cars?

- This is a major challenge and a critical area of development. Robust regulations, advanced encryption, secure data storage protocols, and transparent data usage policies will be essential. Consumers will demand assurances that their personal data, location history, and driving patterns are protected from misuse and cyberattacks. The industry is actively working on global standards and legal frameworks to address these complex issues.

The automotive industry is in the midst of an exhilarating and challenging period of reinvention. The multiplication of its ecosystem signifies a shift from a product-centric model to a service-and-data-centric one. While this transformation brings its share of dangers, particularly for those unwilling to adapt, it also unlocks unprecedented opportunities for innovation, economic growth, and ultimately, a more efficient and sustainable future for mobility-as-a-service. Understanding these changes is crucial for anyone involved in, or impacted by, the evolving world of automotive transport.

If you want to read more articles similar to The Automotive Ecosystem: A Radical Shift, you can visit the Automotive category.