19/02/2007

- Understanding PCP Car Finance and Early Termination

- What is PCP Finance?

- Your Right to Voluntary Termination

- How Voluntary Termination Works with PCP

- Can You End PCP Early and Keep the Car?

- Voluntary Termination vs. Early Settlement

- What About the Balloon Payment in PCP?

- When Can You Voluntarily Terminate?

- Does Voluntary Termination Affect Your Credit Score?

- What Happens at the End of a PCP Contract?

- FAQs About PCP Voluntary Termination

- Conclusion

Understanding PCP Car Finance and Early Termination

Navigating car finance agreements can sometimes feel complex, and it's not uncommon for personal circumstances to change, leading to a need to exit a contract early. One of the most popular forms of car finance is Personal Contract Purchase, or PCP. This type of agreement offers flexibility, often with lower monthly payments compared to traditional hire purchase, but it also comes with specific terms regarding early termination. If you're wondering 'What happens if I cancel my car contract with PCP?', you're in the right place. This article will delve into the specifics of voluntarily terminating your PCP agreement, your rights, and what you need to consider.

What is PCP Finance?

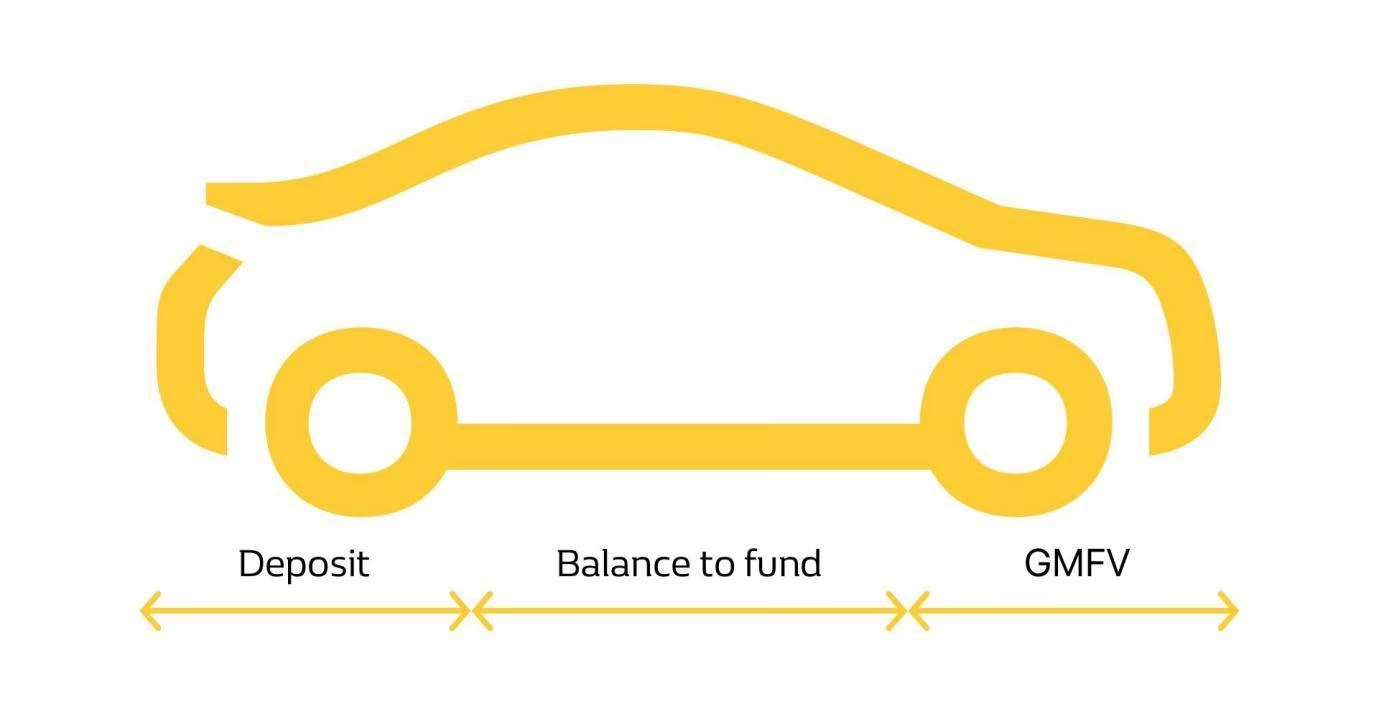

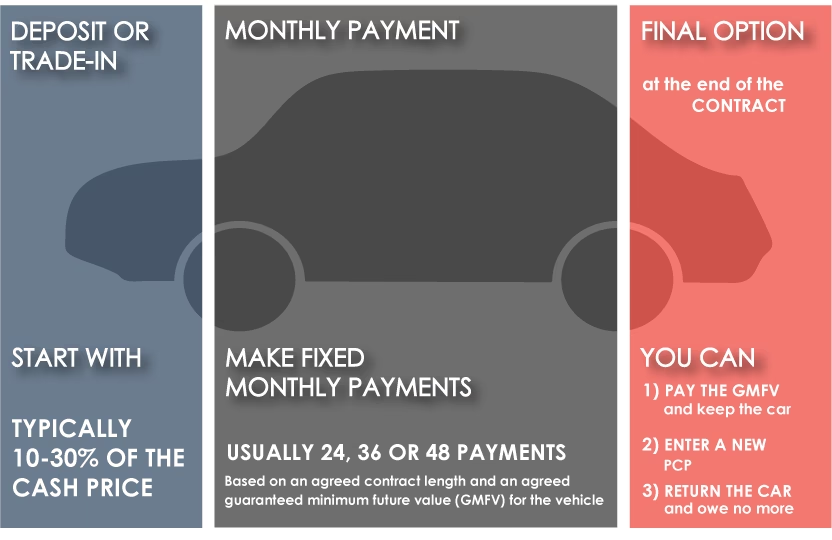

Before we explore early termination, it’s essential to understand how PCP works. With a PCP deal, you typically pay a deposit, followed by a series of monthly instalments. Crucially, these monthly payments don't cover the entire cost of the car. Instead, they cover the depreciation of the vehicle over the contract term, plus interest. At the end of the contract, you usually have three options:

- Pay a large balloon payment (also known as the Guaranteed Future Value or GFV) to own the car outright.

- Hand the car back to the finance company.

- Part-exchange the car for a new one, using any equity towards a new deal.

Your Right to Voluntary Termination

Under the Consumer Credit Act, you have a legal right to end most car finance agreements early. This is known as voluntary termination. This right applies to both Hire Purchase (HP) and Personal Contract Purchase (PCP) agreements, provided they are regulated by the Financial Conduct Authority (FCA).

The key condition for exercising voluntary termination is that you must have paid at least 50% of the total amount payable under the agreement. This 'total amount payable' includes the car's price, interest, and any other charges or fees, but excludes the final balloon payment in a PCP agreement if you were to take ownership.

How Voluntary Termination Works with PCP

To initiate voluntary termination, you need to inform your finance provider in writing. This can be done via email or a formal letter. Once you notify them, you will be liable for up to 50% of the total amount payable.

Let's break down the 50% rule for PCP:

Imagine your car has a total amount payable of £20,000 over a 4-year PCP contract. The 50% mark would be £10,000. This £10,000 represents your total outlay in terms of deposits and monthly payments. If you have already paid £10,000 or more through your regular instalments, you can hand the car back.

What if you haven't paid 50%? If you're part-way through your contract and haven't yet reached the 50% payment threshold, you will need to make a lump sum payment to cover the remaining balance to reach that 50% point. For example, if you've paid £8,000 and need to reach £10,000, you'd need to pay an additional £2,000.

Once you have paid the required amount (either through regular payments or a top-up), you are entitled to hand the car back. Your finance company will then arrange for the vehicle to be collected. They will inspect it to ensure it’s in a reasonable condition, considering its age and mileage. You will be expected to pay for any damage that goes beyond 'fair wear and tear'.

Fair Wear and Tear Explained

Fair wear and tear refers to the expected deterioration of a vehicle due to normal use. Minor scratches, small chips on the windscreen, or slightly worn tyres are generally acceptable. However, significant damage such as large dents, cracked lights, ripped upholstery, or bald tyres will likely be considered beyond fair wear and tear and could incur charges.

Finance companies usually provide a fair wear and tear guide, so it's advisable to check this before returning the vehicle.

Can You End PCP Early and Keep the Car?

Yes, you can end your PCP agreement early and keep the car, but this is different from voluntary termination. This is typically referred to as an 'early settlement'. To do this, you would request an early settlement figure from your finance provider. This figure will include the outstanding balance of the loan, plus any remaining interest, minus any rebates you might be entitled to.

Paying off the early settlement figure means you will own the car outright and your finance agreement will be concluded. This is a good option if you want to keep the car but no longer wish to make monthly payments.

Voluntary Termination vs. Early Settlement

It's important to distinguish between voluntary termination and early settlement:

| Feature | Voluntary Termination | Early Settlement |

|---|---|---|

| Outcome | You hand the car back. | You keep the car and own it outright. |

| Payment Requirement | You must have paid 50% of the total amount payable (or pay up to it). | You pay the outstanding balance plus interest (less rebates). |

| Car Condition | Must meet fair wear and tear standards. | Not applicable, as you are keeping the car. |

| Balloon Payment (PCP) | Included in the 50% calculation if not yet paid. | Paid as part of the settlement figure. |

What About the Balloon Payment in PCP?

The balloon payment, or GFV, is a significant part of a PCP contract. When you voluntarily terminate, the 50% rule applies to the *total amount payable* for the finance. This amount typically includes the monthly payments and the balloon payment if you were to opt for ownership. However, if you are simply handing the car back via voluntary termination, you do not need to pay the balloon payment itself. Instead, your obligation is capped at 50% of the total finance cost.

When Can You Voluntarily Terminate?

You can technically initiate voluntary termination at any point during your agreement, as long as you meet the 50% payment threshold. There's also a statutory 14-day cooling-off period at the very start of your contract, during which you can withdraw from the agreement without penalty.

However, for most people, voluntary termination becomes a viable option when they are more than halfway through their contract, as this is when they would have naturally paid off 50% of the total amount.

Does Voluntary Termination Affect Your Credit Score?

Voluntarily terminating a car finance agreement does not inherently harm your credit score, provided you have met all your obligations. In fact, a record of a mutually agreed-upon termination, where all payments were made on time, can demonstrate responsible credit management. The key is to communicate with your lender and ensure all payments are up-to-date before and during the termination process.

Crucially, failing to make payments and defaulting on your agreement will negatively impact your credit score. If you anticipate difficulties in making payments, it is always best to contact your finance provider as soon as possible to discuss your options. A voluntary termination, handled correctly, is a positive outcome compared to a default.

What Happens at the End of a PCP Contract?

As mentioned, at the end of a standard PCP contract, you typically have three choices:

- Pay the Balloon Payment: If you want to keep the car, you pay the Guaranteed Future Value (GFV) and the car becomes yours.

- Hand the Car Back: If you don't want to keep the car and have met your payment obligations, you can simply return it to the dealer with nothing further to pay (assuming it meets fair wear and tear standards).

- Part-Exchange: If the car's market value is higher than the GFV, you can use this equity as a deposit towards a new car.

Voluntary termination allows you to exit the contract *before* the end, under the 50% rule, without needing to worry about the balloon payment or the car's final market value.

FAQs About PCP Voluntary Termination

Q1: Can I voluntarily terminate my PCP agreement if I'm only a quarter of the way through?

A1: You can initiate the process, but you will need to pay the difference to reach the 50% payment threshold before the termination can be completed.

Q2: What if my car has more than fair wear and tear?

A2: You will be liable for the cost of any repairs needed to bring the car up to the standard expected for its age and mileage. It's wise to get any necessary repairs done yourself before returning it, as finance companies may charge more for these services.

Q3: Does voluntary termination mean I get money back?

A3: No, voluntary termination is about ending your liability. You don't get any of your payments back; it's simply a way to settle your obligation by paying up to 50% of the total amount payable.

Q4: Should I speak to my finance provider before terminating?

A4: Absolutely. While you have a legal right, discussing your situation with your lender can provide clarity on the exact figures and the process involved. They can confirm your 50% point and the next steps.

Q5: What's the difference between voluntary termination and just handing the car back at the end of the contract?

A5: Handing the car back at the end of the contract is one of the standard options. Voluntary termination is an option to exit the contract *early*, provided you've paid at least 50% of the total amount payable.

Conclusion

Understanding your rights regarding voluntary termination for your PCP car finance is crucial. It offers a valuable safety net if your circumstances change. Remember to always review your contract, communicate with your finance provider, and ensure you meet the 50% payment rule. By doing so, you can navigate the early termination process smoothly and responsibly.

If you want to read more articles similar to Ending Your PCP Car Finance Early, you can visit the Automotive category.