28/07/2009

Navigating the world of car protection can feel like a complex journey through a labyrinth of jargon. Many motorists in the UK often find themselves scratching their heads when trying to distinguish between a manufacturer's warranty, an extended vehicle service contract, and their standard car insurance policy. While all three are designed to offer peace of mind and financial security for your vehicle, they serve distinctly different purposes and come into play under very different circumstances. Understanding these distinctions is crucial for making informed decisions about how to best protect your investment and avoid unexpected out-of-pocket expenses.

- Unpacking the Core Differences: Warranty vs. Service Contract

- Warranty/Service Contract vs. Car Insurance: A Crucial Distinction

- Understanding Car Warranty and Service Contract Coverage Types

- Understanding Car Insurance Coverage

- Do You Really Need Both?

- How to Choose a Good Vehicle Service Contract

- Frequently Asked Questions

- Conclusion

Unpacking the Core Differences: Warranty vs. Service Contract

Let's begin by clarifying the relationship between a car warranty and a vehicle service contract. In essence, a vehicle service contract is often referred to as an extended warranty. The primary difference lies in their origin and how they are acquired. A manufacturer's warranty is an assurance provided by the car manufacturer, included in the purchase price of a new vehicle (and sometimes a certified used car). It's a guarantee that the manufacturer will cover the cost of repairs for certain mechanical defects or failures within a specified period or mileage.

On the other hand, a vehicle service contract, or extended warranty, is a separate agreement that you purchase. It kicks in once the original manufacturer's warranty expires, extending the period of protection against mechanical breakdowns. This means while your original warranty is often 'free' (included in the car's price), an extended warranty is a product you actively buy. These contracts are designed to cover mechanical failures, much like a warranty, but they are offered by various providers, including car dealerships and independent third-party companies. The terms, coverage, and cost can vary significantly between providers, making it essential to read the fine print.

Warranty/Service Contract vs. Car Insurance: A Crucial Distinction

Perhaps the most significant area of confusion arises when comparing car warranties (and service contracts) with car insurance. Despite both offering financial protection for your vehicle, their fundamental roles are entirely different. Car insurance is primarily designed to cover damages and injuries resulting from accidents or other unforeseen events like theft or vandalism. It protects you against the financial fallout of incidents on the road, particularly liability for damage you cause to others.

Conversely, a car warranty or service contract focuses solely on mechanical failures. If your car breaks down due to a faulty component, such as a transmission issue or an engine problem, a warranty or service contract would typically cover the repair costs. It's about ensuring the ongoing mechanical reliability of your vehicle, not protecting against accidental damage. Think of it this way: if your car suffers a breakdown due to a manufacturing defect, your warranty steps in. If your car is involved in a collision, your insurance policy is what you'll turn to.

Comparative Overview: Car Warranty vs. Car Insurance

To further illustrate these differences, consider the following comparison:

| Feature | Car Warranty / Service Contract | Car Insurance |

|---|---|---|

| Purpose | Covers mechanical failures and defective parts. | Covers damage and injuries (liability, collision, comprehensive) from accidents, theft, vandalism, etc. |

| When It Applies | When your car experiences a mechanical breakdown. | When your car is damaged in an accident or other covered event. |

| Legal Requirement | Not legally required in the UK. | Legally required for all drivers in the UK. |

| Typical Coverage | Regular wear and tear (for some plans), defective parts, major components (engine, gearbox). | Damage to your vehicle, damage to other vehicles/property, medical expenses for injuries. |

| Average Cost (Estimated) | £800 - £3,500 (total for extended, depending on coverage/term). | £400 - £1,500+ (per year, highly variable). |

| Payment Structure | One-off payment or monthly instalments (for extended). | Monthly, quarterly, or annual premiums. |

| Term Length | Varies (e.g., 1-5 years or up to a certain mileage). | Typically 6 months to 1 year. |

| Providers | Car manufacturers, dealerships, third-party companies. | Insurance companies, brokers. |

Understanding Car Warranty and Service Contract Coverage Types

When considering an extended warranty or service contract, it's vital to understand the different levels of coverage available. These plans are not one-size-fits-all, and what's covered can significantly impact the value you receive.

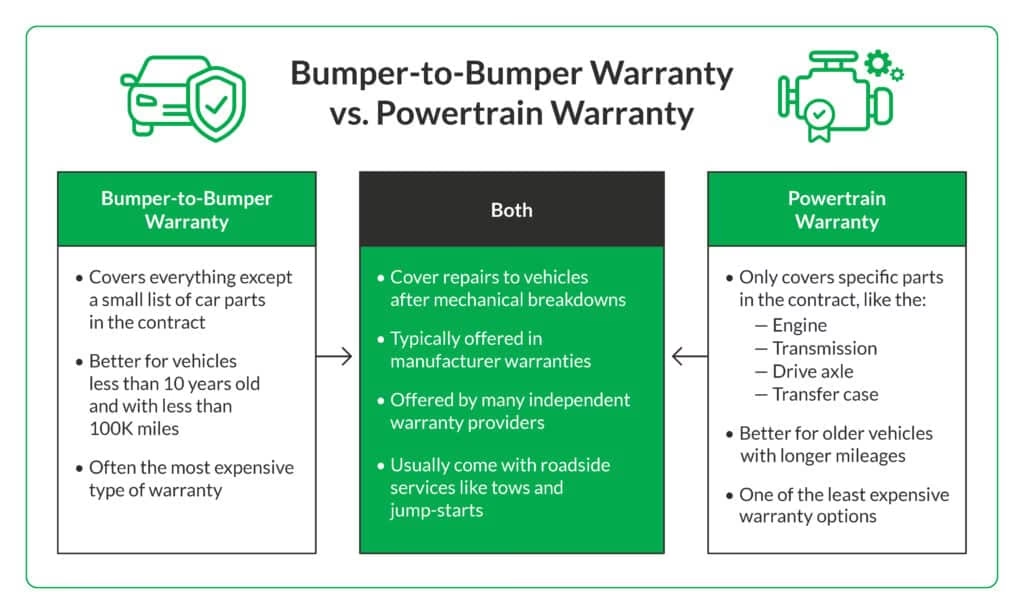

- Drivetrain Warranty: This is often the most basic level of coverage. It focuses on the components that deliver power from the engine to the wheels. This typically includes the transmission, axles, and driveshaft. It's a good option for those seeking protection for the most expensive parts related to propulsion but doesn't cover much else.

- Powertrain Warranty: Stepping up from drivetrain, a powertrain warranty expands coverage to include the engine in addition to the drivetrain components. The engine and gearbox are typically the most costly repairs, making this a popular choice for many motorists. It's a more comprehensive plan than drivetrain but still leaves many other vehicle systems uncovered.

- Bumper-to-Bumper Warranty (Exclusionary Plans): This is generally the most comprehensive type of coverage you can purchase. Often referred to as 'exclusionary' plans, they cover all major vehicle systems and components, except for a specific list of items that are explicitly excluded in the contract. It's usually easier for the contract to list what isn't covered than what is, giving you a broad scope of protection. Items typically excluded are wear-and-tear components like brake pads, tyres, windscreen wipers, and routine maintenance items.

- Corrosion Warranty: Specifically designed to cover rust and other environmental factors that might lead to corrosion on the vehicle's bodywork or frame. This is often included as a separate, longer-term part of a manufacturer's warranty, but specific extended policies might also offer it.

- Wrap Policy: A wrap warranty is designed to 'wrap around' an existing powertrain warranty. For example, if your manufacturer's powertrain warranty is very long, but the bumper-to-bumper portion is shorter, a wrap policy extends the bumper-to-bumper coverage to match the length of the powertrain warranty. This ensures that you have comprehensive protection for a longer period, aligning different coverage terms.

The average cost of an extended warranty in the UK can vary significantly, but often ranges from £800 to £3,500 for the total policy. Many providers offer the option to break down this cost into monthly payments, making it more manageable. These policies remain valid until your vehicle reaches a set mileage limit or a specific amount of time has passed, whichever comes first.

Understanding Car Insurance Coverage

Car insurance is a legal necessity for all drivers in the UK, mandated by the Road Traffic Act. It's designed to protect drivers, passengers, other motorists, and pedestrians in the event of an accident. The level of coverage you choose will dictate what is financially protected.

- Third-Party Only (TPO): This is the minimum legal requirement. It covers injury to other people and damage to their property (including their vehicle) if you're involved in an accident that's your fault. It does not cover any damage to your own vehicle or your own injuries.

- Third-Party, Fire and Theft (TPFT): This covers everything included in TPO, plus it protects your vehicle if it's stolen or damaged by fire.

- Comprehensive Coverage: This is the most extensive type of car insurance. It includes everything from TPFT, plus it covers damage to your own vehicle, even if the accident is your fault. It often includes cover for medical expenses, personal belongings, and sometimes a courtesy car while yours is being repaired.

- Collision Coverage (often part of Comprehensive): Pays for damage to your vehicle if you are in an accident or hit an object, regardless of fault.

- Uninsured Motorist Coverage: While less common as a standalone in the UK than in some other countries (due to mandatory insurance), some comprehensive policies may offer protection if you're involved in an accident with an uninsured driver.

- Medical Payments Coverage: Covers medical bills for you or your passengers if you're injured in an accident, regardless of fault. This is often part of comprehensive policies or available as an add-on.

- Gap Coverage: If your car is written off or stolen, your insurer will pay out its current market value. If this value is less than what you still owe on a finance agreement, gap insurance covers the 'gap' between the two amounts, preventing you from being out of pocket.

The cost of car insurance in the UK is highly variable, influenced by factors such as your age, driving history, vehicle type, postcode, and even where you park your car. Lenders will almost certainly require comprehensive coverage if you are financing your car, ensuring their asset is protected until the loan is fully repaid.

Do You Really Need Both?

The simple answer is that nearly all drivers in the UK are legally required to have car insurance, but a car warranty or extended service contract is entirely optional. However, having both can provide a robust financial safety net and significant peace of mind, especially if you own an older vehicle no longer covered by a manufacturer's warranty.

Car insurance protects you against the unpredictable and potentially catastrophic costs of accidents, theft, or fire. Without it, you could face immense financial liability. A car warranty, on the other hand, protects you from the inevitable: mechanical failures. All cars, regardless of how well they are maintained, will eventually experience component wear and tear or unexpected breakdowns. For an older car, where the likelihood of a major component failure increases, an extended warranty can be an invaluable asset, potentially saving you thousands in repair bills.

Many extended warranty plans also come with beneficial perks such as roadside assistance, breakdown cover, and rental car reimbursement, which can prove incredibly handy during a vehicle breakdown. Ultimately, the decision to purchase an extended warranty depends on your personal risk tolerance, your vehicle's age and reliability, and your financial planning strategy. It's about weighing the cost of the policy against the potential cost of unexpected repairs.

How to Choose a Good Vehicle Service Contract

If you decide an extended warranty is right for you, choosing the right one requires careful consideration. Here are some pointers:

- Understand the Coverage Levels: As discussed, differentiate between powertrain, drivetrain, and bumper-to-bumper (exclusionary) plans. Ensure the plan covers the parts you're most concerned about. An exclusionary plan is generally the most comprehensive as it lists what's *not* covered, making it clearer.

- Check the Provider's Reputation: Look for reviews and ratings of the warranty provider. Are they known for honouring claims promptly and without hassle?

- Read the Fine Print: Pay close attention to exclusions, limitations, and the claims process. Are there specific components not covered? Are there mileage or age restrictions? Are there specific service requirements to keep the warranty valid?

- Deductibles: Most extended warranties have a deductible per repair visit (e.g., £75 - £250). Factor this into your budgeting.

- Transferability: If you plan to sell your car, a transferable warranty can be a significant selling point.

- Cancellation Policy: Understand if and how you can cancel the policy and if you're eligible for a refund.

- Additional Benefits: Look for plans that include perks like roadside assistance, breakdown recovery, or rental car reimbursement.

Frequently Asked Questions

Do I need to extend my car warranty?

It is not legally required to extend your car warranty. However, many car owners choose to do so as part of a financial planning strategy. It can provide peace of mind and protect against unexpected, expensive mechanical repairs, especially as your vehicle ages beyond its manufacturer's warranty period. If you're concerned about budgeting for potential large repair costs, an extended warranty can be a worthwhile investment.

What is mechanical breakdown insurance (MBI)?

Mechanical Breakdown Insurance (MBI) is a type of policy that covers repairs for major systems and components of your vehicle, such as the engine and transmission, similar to what a car warranty offers. While car insurance companies typically don't sell extended warranties, a few may offer MBI. It acts as a form of insurance specifically for mechanical failures, rather than accident damage.

Is a car warranty the same as car insurance?

No, a car warranty is not the same as car insurance. A car warranty or service contract pays for repairs to your car due to mechanical breakdowns or defective parts. Car insurance, on the other hand, covers financial liabilities and damages to your vehicle or others' property resulting from accidents, theft, fire, or vandalism. They address different types of risks and are distinct financial products.

Do vehicle service contracts cover mechanical repairs after a warranty expires?

Yes, absolutely. This is precisely the primary purpose of a vehicle service contract, often referred to as an extended warranty. These contracts are designed to pick up where your car's original factory warranty leaves off, providing continued coverage for mechanical repairs once the manufacturer's guarantee has expired.

Conclusion

In summary, while car insurance is a mandatory legal requirement for driving in the UK, providing protection against accidents and their associated liabilities, a car warranty or vehicle service contract is an optional yet valuable form of protection against mechanical breakdowns. Understanding the distinct roles of each is paramount for any car owner. Car insurance protects you from the financial fallout of unforeseen incidents like collisions, while a warranty safeguards your finances against the inevitable wear and tear and potential failure of your car's intricate mechanical components. For comprehensive peace of mind, many motorists find that a combination of both provides the most robust financial protection for their beloved vehicle.

If you want to read more articles similar to Car Protection: Warranty, Service Contract & Insurance, you can visit the Automotive category.