15/03/2005

Value Added Tax, or VAT, is a consumption tax levied on most goods and services sold in the United Kingdom. It's a significant source of revenue for the government, and understanding its intricacies is crucial for businesses operating within the UK, as well as for consumers making purchases. This article will delve into the current VAT rates, explain what they apply to, and provide insights into how VAT works.

- The Standard VAT Rate

- Reduced VAT Rate

- Zero-Rated VAT

- VAT Exempt Supplies

- VAT Registration Threshold

- How VAT is Calculated

- When do VAT rates change?

- Common Mistakes and Considerations

- Frequently Asked Questions (FAQs)

- Q1: Do I have to charge VAT if my business turnover is below the registration threshold?

- Q2: What's the difference between zero-rated and exempt VAT?

- Q3: Can I charge VAT on my sales if I'm not VAT registered?

- Q4: What happens if I pay VAT on goods I buy for my business but my business is VAT exempt?

- Q5: Where can I find the most up-to-date information on VAT rates and rules?

The Standard VAT Rate

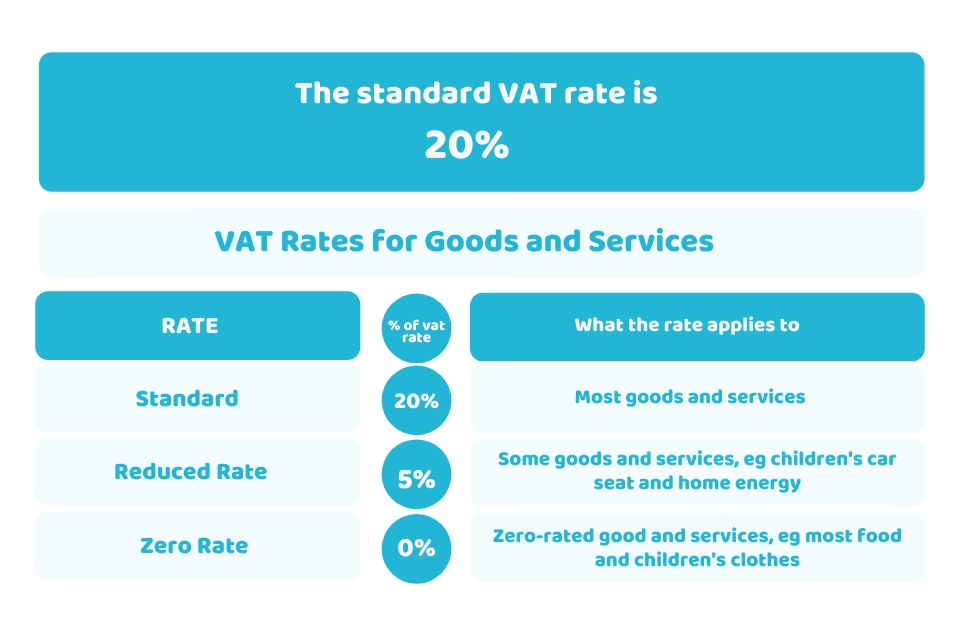

The standard VAT rate in the UK is currently 20%. This is the most common rate and applies to the vast majority of goods and services. If a product or service doesn't fall under a reduced or zero rate, it's safe to assume it will be subject to the standard 20% VAT.

What does the standard rate apply to?

Examples of goods and services charged at the standard rate include:

- Most household goods

- Electrical appliances

- Clothing and footwear (unless specifically exempt or reduced rate)

- Restaurant meals and takeaways

- Hotel accommodation

- Car fuel

- DIY materials

- Most professional services

Reduced VAT Rate

The UK also has a reduced VAT rate of 5%. This rate is applied to certain goods and services that the government considers to be socially important or beneficial. The intention behind the reduced rate is often to make these items more affordable for consumers.

What does the reduced rate apply to?

Key examples of items and services subject to the reduced VAT rate include:

- Domestic fuel and power (e.g., gas and electricity for domestic use)

- Certain energy-saving materials (e.g., solar panels, insulation)

- Children's car seats

- Smoking cessation products

- Mobility aids for the elderly

- Sanitary protection products

- HIV testing kits

- Certain home improvements for energy efficiency

- Some supplies of residential accommodation

Zero-Rated VAT

Perhaps the most distinct category is zero-rated VAT. This is often misunderstood as meaning no VAT is charged, but it's different from exempt supplies. When goods or services are zero-rated, VAT is still charged at a rate of 0%. Crucially, businesses making zero-rated supplies can still reclaim any VAT they have paid on their purchases (input VAT).

What does zero-rated VAT apply to?

The zero rate is typically applied to essential items and services, promoting accessibility and affordability. Common examples include:

- Most food and drink for human consumption (excluding certain items like confectionery, alcoholic drinks, and some hot takeaways)

- Prescription medicines

- Books, newspapers, and journals

- Children's clothing and footwear

- Public transport (e.g., bus and train fares)

- Certain building materials for new homes

- Exports of goods and services outside the UK

VAT Exempt Supplies

While often grouped with zero-rated supplies by consumers, exempt supplies are fundamentally different. For exempt supplies, no VAT is charged, and importantly, businesses making exempt supplies cannot reclaim VAT paid on their business expenses. This means the VAT cost is absorbed by the business.

What are VAT exempt supplies?

Examples of VAT exempt supplies include:

- Most education and vocational training

- Most health services provided by registered practitioners

- Insurance transactions

- Certain financial services

- Burial and cremation services

- Gambling

VAT Registration Threshold

Businesses in the UK are generally required to register for VAT if their taxable turnover exceeds a certain threshold. This threshold is reviewed annually by the government. Currently, the threshold is £85,000. If your business's taxable turnover is below this figure, you are not legally required to register for VAT, although you can choose to do so voluntarily.

Why Register for VAT?

Voluntary registration can be beneficial if your business incurs a significant amount of VAT on its purchases (input VAT). By registering, you can reclaim this input VAT from HMRC, which can improve your cash flow. However, if your customers are primarily individuals who cannot reclaim VAT, charging VAT on your sales might make your prices less competitive.

How VAT is Calculated

The calculation of VAT is straightforward once you know the correct rate. The formula is:

VAT Amount = Net Price x VAT Rate

Total Price = Net Price + VAT Amount

Alternatively, if you know the gross price (the price including VAT), you can calculate the net price by dividing the gross price by (1 + VAT Rate).

Example Calculation:

Let's say you purchase a laptop for £1,000 (excluding VAT). The standard VAT rate is 20%.

- VAT Amount = £1,000 x 20% = £200

- Total Price = £1,000 + £200 = £1,200

If the price you see advertised is £1,200 (including VAT), and you know it's a standard-rated item:

- Net Price = £1,200 / (1 + 0.20) = £1,200 / 1.20 = £1,000

When do VAT rates change?

VAT rates are set by Her Majesty's Treasury and can be changed by the government. Significant changes are usually announced in the national budget. It's essential for businesses to stay updated on any changes to ensure they are applying the correct rates to their sales and correctly accounting for VAT.

Common Mistakes and Considerations

One of the most common mistakes is applying the wrong VAT rate. This can lead to incorrect tax returns, penalties, and interest charges from HMRC. Another is the confusion between zero-rated and exempt supplies, particularly regarding the ability to reclaim input VAT.

Table: VAT Rate Summary

| VAT Rate | Applies To | Reclaim Input VAT? |

|---|---|---|

| 20% (Standard) | Most goods and services | Yes |

| 5% (Reduced) | Domestic fuel, energy-saving materials, children's car seats, etc. | Yes |

| 0% (Zero-rated) | Essential foods, books, children's clothing, exports, etc. | Yes |

| Exempt | Education, health, insurance, financial services, etc. | No |

Frequently Asked Questions (FAQs)

Q1: Do I have to charge VAT if my business turnover is below the registration threshold?

No, if your taxable turnover is below the mandatory registration threshold (£85,000 as of current legislation), you are not required to register for VAT. However, you can choose to register voluntarily.

Q2: What's the difference between zero-rated and exempt VAT?

For zero-rated supplies, VAT is charged at 0%, and the business can reclaim input VAT. For exempt supplies, no VAT is charged, and the business cannot reclaim input VAT on related expenses.

Q3: Can I charge VAT on my sales if I'm not VAT registered?

No, you can only charge VAT on your sales if you are VAT registered. If you are not registered, you cannot add VAT to your invoices.

Q4: What happens if I pay VAT on goods I buy for my business but my business is VAT exempt?

If your business makes exempt supplies, you cannot reclaim the VAT you pay on your business expenses. This VAT becomes a cost to your business.

Q5: Where can I find the most up-to-date information on VAT rates and rules?

The official source for all VAT information in the UK is HM Revenue and Customs (HMRC). Their website (gov.uk) provides detailed guidance, updates, and specific rules for various goods and services.

Understanding VAT is an ongoing process, especially with potential changes in rates and regulations. By staying informed and ensuring accurate application of the correct rates, businesses can maintain compliance and manage their finances effectively. Always refer to official HMRC guidance for the most current and definitive information.

If you want to read more articles similar to Understanding UK VAT Rates, you can visit the Automotive category.