14/04/2018

In the fast-paced world of motoring, not every journey fits neatly into a standard annual insurance policy. Perhaps you're borrowing a friend's car for a weekend trip, test driving a potential new purchase, or even just need a vehicle for a short business stint. This is where temporary car insurance steps in, offering a remarkably flexible and convenient solution for short-term driving needs in the UK.

Unlike traditional annual policies, temporary car insurance is designed specifically for those moments when you only require cover for a limited period, typically ranging from as little as one hour up to 30 days. It provides comprehensive protection, mirroring the robust cover of a full annual policy, but with the distinct advantage of paying only for the exact duration you need. This tailored approach makes it an incredibly cost-effective and practical alternative to more cumbersome options, ensuring you're legally and safely on the road without unnecessary financial burden or long-term commitments.

- What Exactly is Temporary Car Insurance?

- When Do You Need Temporary Car Insurance?

- Understanding Eligibility: Driver and Vehicle Requirements

- Can I Get Temporary Car Insurance on a Friend's Car?

- Can I Get Temporary Car Insurance Without Main Insurance?

- Age and Experience: New Drivers & Temporary Insurance

- Why Might I Be Refused Temporary Car Insurance?

- Comparing Temporary vs. Other Insurance Options

- Frequently Asked Questions About Temporary Car Insurance

- How long does temporary car insurance cover?

- Do I need temporary car insurance if I'm test driving a car?

- Can I use temporary car insurance for business purposes?

- What is the minimum age for temporary car insurance?

- Will a claim on a temporary policy affect the owner's main insurance?

- Can I get temporary cover for a van or motorhome?

- What if I've been refused temporary car insurance?

- How to Check Your Eligibility and Get Covered

What Exactly is Temporary Car Insurance?

At its core, temporary car insurance is exactly what it sounds like: a short-term insurance policy tailored for specific, limited durations. Instead of committing to a full year of cover, you can secure comprehensive insurance for a few hours, days, or weeks. This flexibility is its main appeal, especially when compared to traditional methods of insuring a borrowed vehicle or a car you only use occasionally.

Consider the alternatives: you could ask the vehicle owner to add you as a named driver to their existing annual policy. While this is an option, it often comes with a few drawbacks. Firstly, the owner's premium might increase, and secondly, if you were to be involved in an incident and make a claim, it could directly impact their precious Protected No Claims Discount (NCD). Losing an NCD can significantly increase future premiums for the owner, making it a less appealing option for many.

Another alternative might be to take out a full annual policy on the vehicle and then cancel it when you no longer need it. This is generally the least efficient and most expensive route. You'd likely pay a substantial upfront premium, and then face cancellation fees, administrative hurdles, and potentially a pro-rata refund that doesn't fully compensate for the hassle. Temporary cover, by contrast, removes these complexities, offering a clean, pay-as-you-go solution.

The Key Benefits of Temporary Cover

- Cost-Effectiveness: You only pay for the time you need, making it significantly cheaper for short-term use than an annual policy.

- Protecting NCD: It operates as a standalone policy, meaning any claims made under your temporary cover will not affect the vehicle owner's No Claims Discount on their main policy.

- Flexibility: Cover durations can be highly specific, from just one hour to a full month, adapting precisely to your requirements.

- Ease and Speed: Getting a quote and being covered can often be done online within minutes, providing immediate peace of mind.

- Comprehensive Cover: Most temporary policies offer fully comprehensive cover, giving you the highest level of protection available.

Ultimately, temporary car insurance is a modern solution for modern driving habits, acknowledging that not all vehicle usage fits a year-long mould.

When Do You Need Temporary Car Insurance?

The scenarios in which temporary car insurance proves invaluable are more common than you might think. It's the perfect solution for those instances where your regular insurance doesn't quite fit, or when you're using a vehicle that isn't your own for a limited period. Here are some of the most frequent situations where short-term cover becomes essential:

- Test Driving a Vehicle: If you're looking to buy a car privately, you'll need to test drive it. Your existing policy might not cover you for driving other vehicles, or the seller's policy won't cover you. Temporary test drive insurance ensures you're fully covered for this crucial evaluation. Similarly, if you're selling a car and offering test drives, this cover protects you.

- Borrowing a Friend or Family Member's Car: Whether it's for a weekend trip, a favour, or just while your own car is in the garage, borrowing a car means you need proper insurance. Temporary cover allows you to drive their vehicle legally without putting their NCD at risk or increasing their premiums.

- Business Use: Your existing annual policy might only cover personal use. If you need to use a car for a one-off business trip, for example, driving to a meeting that's not part of your daily commute, temporary car insurance for business use can provide the necessary cover without altering your main policy. (Note: This typically excludes delivery, door-to-door sales, or taxi services).

- Moving House or Transporting Large Items: For those bigger tasks that require a larger vehicle, such as borrowing a van to move furniture or personal belongings, temporary van insurance works in the same flexible way as car cover. It's ideal for those one-off, heavy-duty tasks.

- Collecting or Delivering a Car: If you've just bought a car and need to drive it home before arranging annual cover, or if you're helping someone transport a vehicle, temporary insurance offers immediate protection for the journey.

- Emergencies: Life is unpredictable. If your car breaks down unexpectedly and you need to use a family member's vehicle to get to work or handle an urgent situation, temporary insurance can be arranged quickly to cover you.

- Sharing the Driving on a Long Journey: On extended trips, sharing the driving can make the journey safer and more enjoyable. Temporary cover allows a second driver to be insured for their leg of the journey without hassle.

It's important to note that specific short-term cover is also available for learner drivers, allowing them to practice in a friend or family member's car under a separate, dedicated policy.

Understanding Eligibility: Driver and Vehicle Requirements

While temporary car insurance offers remarkable flexibility, providers do have specific criteria that both the driver and the vehicle must meet to be eligible for cover. These criteria are in place to manage risk and ensure the safety of all parties involved.

Driver Eligibility Criteria:

To secure a temporary car insurance policy, you will typically need to meet the following requirements:

- Age: Most companies offer temporary car insurance for drivers aged between 18 and 75. Some may have slightly different age bands, for instance, learner driver insurance might be available from 17.

- Driving Licence: You will almost certainly need a full Great Britain (GB) driver's licence. Many providers require that you have held this licence for a minimum period, often six months. However, some, like Dayinsure, might reduce this to three months for drivers over 25.

- Permanent UK Address: You must have a permanent residential address in the United Kingdom. This helps insurers verify your identity and assess risk.

- Penalty Points: Insurers usually have a maximum number of penalty points allowed on your licence. This number can vary between providers, so it's crucial to check their specific terms. Generally, a small number of minor points might be acceptable, but a high number or more serious endorsements could lead to refusal.

- Criminal Convictions: Most temporary car insurance providers require that customers do not have any unspent criminal convictions, with the exception of minor motor offences. If you have any convictions, especially unspent ones, it's best to check with the insurer directly or look for specialist policies for convicted drivers.

- Permission from Vehicle Owner: This might seem obvious, but you absolutely must have explicit permission from the vehicle's registered owner to drive their car. Without it, any policy would be invalid.

- Previous Insurance Refusals: If you have previously been refused car insurance by another provider, or had a policy cancelled, this could impact your eligibility for temporary cover.

Vehicle Eligibility Criteria:

Just as there are requirements for the driver, the vehicle itself must also meet certain conditions to be covered by a temporary policy. While these can vary slightly between insurers, common criteria include:

- UK Registration: The vehicle must be registered in Great Britain. Some providers, like Aviva, may extend this to Northern Ireland and the Isle of Man.

- Market Value: There's often a maximum current market value for the vehicle. For example, many insurers set a limit of under £75,000.

- Gross Vehicle Weight (GVW): The vehicle must typically be less than 3.5 tonnes GVW. This excludes larger commercial vehicles or HGVs.

- Engine Size: There might be an upper limit on engine size, for instance, 3999cc or less.

- Modifications: Vehicles with significant engine modifications or body kits (excluding manufacturer-fitted extras or those for mobility assistance) are often excluded.

- Seating Capacity: There's usually a maximum number of seats, commonly eight.

- Vehicle Type Exclusions: Hire or rental vehicles, imported vehicles (unless specifically allowed), and vehicles that have been seized or are in a police compound are generally not eligible for temporary cover.

- Tax and MOT: While temporary insurance doesn't require the main policy, the vehicle itself must be taxed and have a valid MOT certificate (if applicable) at all times.

It's always recommended to thoroughly check the specific eligibility criteria of the chosen temporary insurance provider before proceeding with a quote, as these details are crucial for a valid policy.

Can I Get Temporary Car Insurance on a Friend's Car?

Absolutely, yes! One of the primary uses and benefits of temporary car insurance is its suitability for driving a friend or family member's car. As long as both you (the driver) and the vehicle meet the specific eligibility and underwriting criteria of the insurance provider, and crucially, you have been given explicit permission by the vehicle owner to drive their car, then you should be able to take out a temporary policy on it.

This is a far more advantageous option than being added as a named driver to their existing policy, as your temporary cover operates independently. This means that in the unfortunate event of a claim, the friend's own No Claims Discount remains completely unaffected, protecting their future premiums. Before taking out the policy, always double-check that the car you intend to insure is properly taxed and has a valid MOT certificate, as these are fundamental legal requirements for any vehicle on UK roads.

Can I Get Temporary Car Insurance Without Main Insurance?

Yes, you can. You do not need to hold an annual, or 'main', insurance policy yourself to take out temporary car insurance. This is a common misconception. Temporary car insurance can act as a standalone policy, making it an ideal solution if you are, for example, between annual policies, or if you simply don't own a vehicle yourself but occasionally need to drive someone else's.

However, it is critically important to understand that, under UK law, any vehicle on the road must be insured at all times, or registered as SORN (Statutory Off Road Notification) if it's not being used. While your temporary policy covers you to drive the car, the responsibility for ensuring the vehicle is continuously insured ultimately rests with the vehicle's owner. So, even if you are borrowing it, the owner must maintain their own main insurance policy on the car, or ensure it's SORN, to comply with continuous insurance enforcement rules.

Most temporary policies offer fully comprehensive insurance, providing the same high level of protection you would expect from an annual policy, covering damage to the vehicle, third-party liability, and often, personal injury.

Age and Experience: New Drivers & Temporary Insurance

Navigating the insurance landscape as a young or newly qualified driver can be challenging, but temporary car insurance often provides an accessible pathway to getting on the road.

Can I Get Temporary Car Insurance at 18?

Yes, in most cases, you can. While age limits vary between providers, many temporary car insurance companies, including prominent ones like Dayinsure, do offer cover to drivers from the age of 18. This makes it a viable option for young drivers who might find annual policies prohibitively expensive or restrictive.

It's worth noting that eligibility criteria can sometimes be slightly different for vehicles like vans, motorhomes, or campervans, even for temporary cover. For those still learning to drive, specific learner driver insurance is usually available from age 17 and upwards, allowing supervised practice in a family or friend's car without affecting the owner's policy.

Can I Get Temporary Car Insurance If I've Just Passed My Test?

This depends on the specific terms and eligibility criteria of the insurance provider. Many insurers will require that you have held your full driving licence for a minimum period, often ranging from three to six months. This requirement is typically in place to ensure that drivers have gained some experience beyond their test before being offered certain policies, as new drivers are statistically at a higher risk of accidents.

If you have just passed your test, remember that any temporary learner driver insurance policy you had immediately becomes invalid. It is absolutely crucial that you take out an appropriate and valid insurance policy for full licence holders before driving the vehicle again. Driving on a learner policy after passing your test is equivalent to driving uninsured and carries severe penalties.

Why Might I Be Refused Temporary Car Insurance?

While temporary car insurance is highly accessible, there are instances where an application might be refused. Understanding these common reasons can help you avoid disappointment:

- Being a New Driver: If you've only just passed your test and haven't held a full licence for the minimum required period (e.g., 3 or 6 months), some providers may decline cover due to a lack of driving experience.

- Your Age: Being outside the provider's accepted age range (e.g., under 18 or over 75) will result in a refusal.

- Your Occupation: Certain occupations, particularly those deemed high-risk or requiring specific commercial vehicle insurance (like delivery drivers, taxi drivers, or door-to-door sales), are often excluded from standard temporary policies.

- Having Driving Convictions: A high number of penalty points, or certain serious driving convictions (especially unspent ones), can make you ineligible for cover with many providers.

- Vehicle Modifications: If the vehicle has non-standard modifications, particularly to the engine or significant body kits that aren't factory fitted or for mobility assistance, it might fall outside the accepted criteria.

- Vehicle Value or Type: Vehicles with a market value above a certain threshold (e.g., over £75,000), heavy goods vehicles (HGVs), or those with an engine size exceeding the limit (e.g., over 3999cc) are typically not covered. Likewise, hire or rental vehicles, or those imported from certain countries, are generally excluded.

- Previous Refusals or Cancellations: If you have previously been refused car insurance by another insurer, or had a policy cancelled, this can be a red flag for new providers.

- Incomplete or Inaccurate Information: Providing incorrect or incomplete details during the application process can lead to immediate refusal or policy invalidation.

In most cases, the decision rests with the insurer's underwriters, who assess risk based on their internal criteria. If refused, the company may not be able to provide a detailed explanation beyond stating that the criteria were not met.

Comparing Temporary vs. Other Insurance Options

To further illustrate why temporary car insurance stands out, let's compare it with the other common ways people consider insuring a borrowed vehicle or short-term use:

| Feature | Temporary Car Insurance | Adding as Named Driver (on owner's policy) | Annual Policy (then cancel) |

|---|---|---|---|

| Cost-Effectiveness | Highly cost-effective; only pay for exact time needed (e.g., 1 hour to 30 days). | Can increase owner's annual premium, sometimes significantly, even for short periods. | Pay for full year upfront; cancellation fees and admin charges apply for early termination. |

| No Claims Discount (NCD) | Protects owner's NCD; your claims don't affect their main policy. | Owner's NCD at risk if you make a claim on their policy. | Your NCD may be affected by short-term cancellation or claims made on your own policy. |

| Flexibility & Duration | Highly flexible; cover from 1 hour up to 30 days, tailored to specific needs. | Less flexible; requires owner to contact their insurer, can be administratively cumbersome for short stints. | Designed for 12 months; cancelling early is an administrative hassle and can be costly. |

| Ease of Setup | Quick and easy online process; often covered in minutes. | Requires owner to contact their insurer, provide your details, and wait for confirmation. | More involved setup process; requires detailed information, then a separate cancellation process. |

| Vehicle Ownership | Ideal for driving borrowed vehicles (friends, family). | Used for driving the vehicle owned by the main policyholder. | Generally for vehicles you own or are the main driver of. |

| Cover Level | Typically comprehensive, offering broad protection. | Matches the main policy's cover level (e.g., Third Party, Fire & Theft, or Comprehensive). | Matches the chosen cover level of the annual policy. |

Frequently Asked Questions About Temporary Car Insurance

Here are some common questions prospective users have about temporary car insurance:

How long does temporary car insurance cover?

Temporary car insurance policies can cover durations from as little as one hour up to 30 days. The precise duration you can select will depend on the provider, but this flexibility allows you to perfectly match the cover to your specific needs.

Do I need temporary car insurance if I'm test driving a car?

Yes, it's highly recommended. Your existing annual policy might not cover you for driving other vehicles, especially those not owned by you. Temporary test drive insurance ensures you are legally and comprehensively covered during the test drive, protecting both you and the seller's vehicle.

Can I use temporary car insurance for business purposes?

Yes, many providers offer temporary car insurance that includes cover for business use. However, it's crucial to check the policy's terms carefully, as this typically excludes specific commercial activities like delivery work, door-to-door sales, or taxi services. It's generally for occasional business trips not covered by your main policy.

What is the minimum age for temporary car insurance?

The minimum age for temporary car insurance is typically 18 years old for standard policies. However, some providers offer specific learner driver temporary insurance from the age of 17.

Will a claim on a temporary policy affect the owner's main insurance?

No, a key benefit of temporary car insurance is that it's a standalone policy. Any claims made under your temporary cover will not impact the vehicle owner's No Claims Discount or their main annual insurance premium.

Can I get temporary cover for a van or motorhome?

Yes, many providers offer temporary van insurance and temporary motorhome/campervan insurance, working on the same short-term, flexible basis as car policies. This is ideal for moving house or taking a short trip in a borrowed leisure vehicle.

What if I've been refused temporary car insurance?

If you've been refused, it's likely due to not meeting the eligibility criteria for the driver (e.g., age, licence duration, penalty points, convictions) or the vehicle (e.g., value, modifications, type). Review the provider's specific criteria thoroughly to understand where the issue might lie.

How to Check Your Eligibility and Get Covered

The process for obtaining temporary car insurance is typically straightforward and designed for speed and convenience. Most temporary car insurers provide a clear list of their eligibility criteria directly on their website. It's always best practice to review these carefully before you begin the quote process to ensure you meet all the requirements for both yourself and the vehicle.

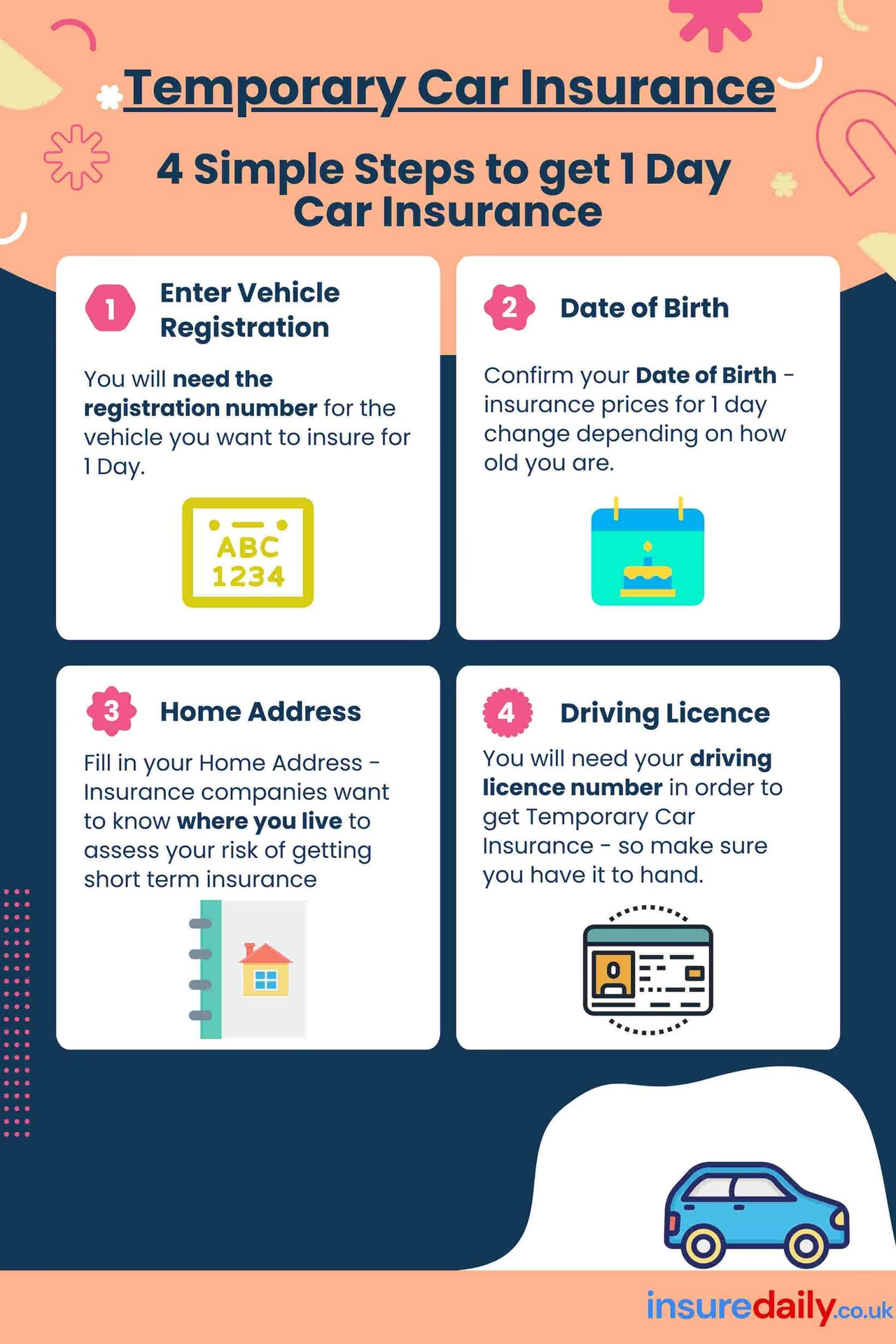

Once you've confirmed your eligibility, getting a quote online is usually a simple matter of inputting a few details about yourself and the vehicle you wish to insure. You'll typically need information such as your driver's licence details, your address, the vehicle's registration number, and the desired duration of cover. Many providers can generate a quote in moments, and if you're happy with the terms, you could be covered and ready to drive within minutes.

In conclusion, temporary car insurance is an incredibly versatile and practical solution for a multitude of short-term driving needs in the UK. It offers the flexibility, cost-effectiveness, and peace of mind that traditional annual policies often cannot provide for intermittent use. Whether you're borrowing a car, test driving a new one, or need a vehicle for a quick business trip, temporary cover ensures you're legally compliant and fully protected without impacting someone else's valuable No Claims Discount.

If you want to read more articles similar to Temporary Car Insurance: Your Flexible UK Guide, you can visit the Insurance category.