18/10/2025

Navigating the intricacies of Value Added Tax (VAT) in the UK can often feel like deciphering a complex code, and indeed, it involves understanding various 'T-codes' used in accounting software. Among the most commonly misunderstood are T0 and T9. While they might seem similar at first glance, their distinctions are fundamental to accurate record-keeping and compliant VAT returns. Getting them wrong can lead to errors, penalties, and unnecessary headaches for your business. This article aims to demystify these two crucial codes, providing a clear understanding that will empower you to manage your VAT obligations with confidence.

Understanding VAT codes is not just about ticking boxes; it's about ensuring your business accurately accounts for its income and expenditure, correctly calculates its VAT liability, and avoids any discrepancies that could attract HMRC's attention. Whether you're a seasoned business owner or just starting out, a solid grasp of T0 and T9 is indispensable for maintaining financial health and adhering to regulations.

- Understanding the UK VAT System: A Brief Overview

- Deep Dive into T0: Zero-Rated Items

- Deep Dive into T9: Non-Vatable Items

- The Crucial Distinction: T0 vs T9

- Comparative Table: T0 vs T9

- Common Pitfalls and How to Avoid Them

- When Should I Use T9 on My VAT Return?

- Frequently Asked Questions (FAQs)

- Conclusion

Understanding the UK VAT System: A Brief Overview

Before diving into T0 and T9, it's helpful to briefly recall the purpose of VAT in the UK. VAT is a consumption tax added to most goods and services sold by VAT-registered businesses. Businesses charge VAT on their sales (output VAT) and can reclaim VAT on their purchases (input VAT). The difference is what they either pay to or reclaim from HMRC.

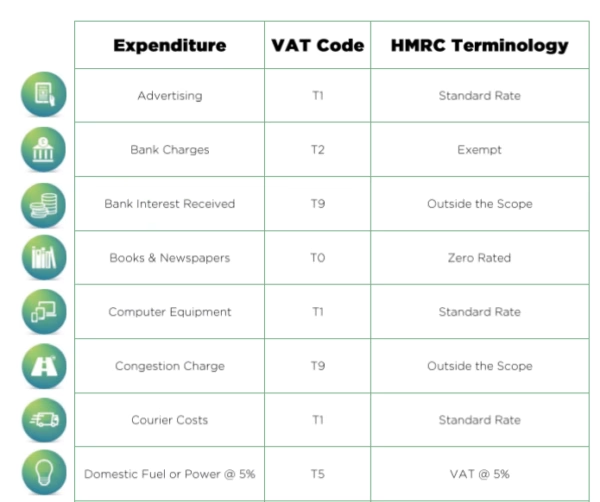

Accounting software uses various 'T-codes' to categorise transactions for VAT purposes. These codes dictate how a transaction is treated in your VAT return, specifying whether VAT is applicable, at what rate, and if it's reclaimable. Most common is T1 (Standard Rated, currently 20%), but others like T2 (Exempt) also play a significant role. The confusion often arises with items where no VAT is charged, leading us to T0 and T9.

Deep Dive into T0: Zero-Rated Items

The T0 VAT code is used for transactions that are zero-rated. This is a critical distinction: zero-rated does not mean 'no VAT'. Instead, it means that while the items are technically subject to VAT, the rate applied is 0%. The key implication is that while you charge 0% VAT on your sales of zero-rated items, you can still reclaim any input VAT you paid on purchases related to making those zero-rated sales.

What Qualifies as Zero-Rated?

HMRC specifies a range of goods and services that fall under the zero-rated category. Common examples include:

- Most food items (excluding catering, hot takeaways, sweets, crisps, alcoholic drinks, and soft drinks)

- Books, newspapers, and magazines

- Children's clothing and footwear

- Public transport (train, bus, tube fares)

- New build houses (first sale)

- Some specified health services and medicines (though many are exempt, not zero-rated)

- Exports of goods from the UK to non-EU countries

For a business selling zero-rated goods, you must still record these sales in your accounts and report them on your VAT return in Box 6 (total value of sales and other outputs excluding VAT). Even though no output VAT is charged, the transaction is still within the scope of VAT.

Deep Dive into T9: Non-Vatable Items

The T9 VAT code is used for transactions that are non-vatable. This means the transaction is entirely outside the scope of UK VAT. There is no VAT charged, and crucially, there is no input VAT to reclaim. These are not sales or purchases that HMRC is interested in for VAT purposes, other than for a complete picture of your business's turnover in some cases.

What Qualifies as Non-Vatable?

Non-vatable items are typically those that fall outside the definition of a 'supply' for VAT purposes or are specifically excluded by law. Common examples include:

- Wages and salaries paid to employees

- Dividends paid to shareholders

- Donations received (if there's no supply of goods or services in return)

- Statutory fees (e.g., MOT tests, vehicle registration fees, road tax)

- Local authority rates (council tax, business rates)

- Insurance premiums (these are exempt from VAT, but often treated as T9 for simplicity in software as no VAT is involved for the payer)

- Bank charges and interest (as per the source provided, these are typically exempt but often coded T9 in software for practical purposes as no VAT is charged or reclaimed)

- Purchases from non-VAT registered businesses

- Private transactions (e.g., selling a personal car not used for business)

For non-vatable transactions, neither output nor input VAT is relevant. They should not typically appear in the VAT boxes (Boxes 1-9) of your VAT return, although the net value might contribute to your overall turnover figure for accounting purposes.

The Crucial Distinction: T0 vs T9

The core difference between T0 and T9 lies in whether the transaction is *within the scope of VAT* but at a 0% rate (T0) or *entirely outside the scope of VAT* (T9). This distinction has significant implications for your VAT return and your ability to reclaim input VAT.

Think of it this way: a zero-rated item (T0) is like a regular VATable item, but with a special 0% rate. An item coded T9 is not subject to VAT at all; it's as if VAT doesn't even exist for that particular transaction.

This is particularly important for input VAT. If you incur costs related to making zero-rated supplies (T0), you can generally reclaim the input VAT on those costs. However, if you incur costs related to non-vatable items (T9), there is no input VAT to reclaim because no VAT was ever involved in the first place.

Impact on Your VAT Return

This is where the practical difference becomes most apparent:

- T0 (Zero-Rated) Sales: The net value of these sales must be included in Box 6 of your VAT return ('Total value of sales and other outputs excluding VAT'). This is because they are still considered 'outputs' within the VAT system, even if no VAT is charged.

- T9 (Non-Vatable) Sales/Purchases: These transactions generally do not appear in any of the VAT boxes (Boxes 1-9) on your VAT return. They are outside the scope. While your accounting software will record them, they don't contribute to your calculated VAT liability or reclaim.

Misclassifying a T0 item as T9, or vice versa, can lead to incorrect VAT calculations, potentially resulting in underpayments or overpayments to HMRC, which can trigger investigations and penalties. Therefore, accuracy is paramount.

Comparative Table: T0 vs T9

| Feature | T0 (Zero-Rated) | T9 (Non-Vatable) |

|---|---|---|

| Definition | Within the scope of VAT, but at 0%. | Outside the scope of VAT entirely. |

| VAT Charged? | Yes, at 0%. | No VAT involved. |

| Input VAT Reclaim? | Yes, input VAT on related purchases can generally be reclaimed. | No, there is no input VAT to reclaim as no VAT was ever charged. |

| VAT Return (Sales) | Net value included in Box 6. | Not included in VAT boxes (1-9). |

| VAT Return (Purchases) | Input VAT amount included in Box 4. Net value in Box 7. | Not included in VAT boxes (1-9). |

| Examples | Most food, children's clothes, books, exports. | Wages, MOTs, road tax, bank charges, donations, purchases from non-VAT registered entities. |

| HMRC Interest | High – part of your VATable turnover. | Low – not part of VATable turnover. |

Common Pitfalls and How to Avoid Them

One of the most common areas of confusion is distinguishing between zero-rated (T0) and exempt (T2 or EX in some systems). While both involve no VAT being charged on the sale, the key difference is input VAT recovery. For exempt supplies, you generally cannot reclaim input VAT on related purchases, whereas for zero-rated supplies, you can. Non-vatable (T9) is distinct from both, as it's not even subject to VAT law.

- Misunderstanding 'Exempt': Items like insurance, education, and certain financial services are 'exempt'. This means you don't charge VAT on them, and you generally cannot reclaim input VAT on costs related to making exempt supplies. This differs from T0 (where you can reclaim) and T9 (where there's no VAT to reclaim anyway). While some accounting software might lump some exempt items under T9 for practical purposes (e.g., bank charges), it's crucial to understand the underlying legal distinction.

- Partial Exemption Rules: If your business makes both VATable (standard, reduced, or zero-rated) and exempt supplies, you may fall under partial exemption rules. This impacts how much input VAT you can reclaim. Correctly coding T0 and T9 items is essential for accurate partial exemption calculations.

- Inaccurate Software Setup: Ensure your accounting software is correctly set up with the appropriate VAT codes for common transactions. If in doubt, consult the software's documentation or a qualified accountant.

- Lack of Documentation: Always keep clear records and documentation for all transactions, especially those coded T0 or T9, to justify their treatment if questioned by HMRC.

When Should I Use T9 on My VAT Return?

This is a frequently asked question. The direct answer regarding the *VAT boxes* (Boxes 1-9) on your official VAT return is: you generally do not use T9 for entries in these boxes. This is because T9 transactions are outside the scope of VAT. They don't contribute to your output VAT, input VAT, or net sales/purchases for VAT calculation purposes.

However, you *will* use the T9 code within your accounting software (e.g., Sage, Xero, QuickBooks) to categorise specific transactions. While these T9 transactions won't populate Box 1, 2, 3, 4, 5, 8, or 9 on your VAT return, their net value *might* be included in Box 6 or 7 if they represent part of your total turnover or expenditure that your accounting software tracks. For example, wages paid (T9) are part of your business expenses, but they have no VAT implication. The software records them, but they are filtered out for the VAT-specific boxes.

So, you use T9 *in your internal accounting system* to correctly classify non-vatable items, ensuring they are excluded from VAT calculations. This internal classification prevents them from erroneously appearing in your VAT return boxes where only VATable (including zero-rated) supplies should be.

Frequently Asked Questions (FAQs)

Q1: Is T0 the same as Exempt (T2)?

No, they are different. T0 (zero-rated) means VAT is charged at 0%, and you can usually reclaim input VAT on related purchases. Exempt (often T2 in Sage) means the supply is outside the scope of VAT for charging purposes, and you generally cannot reclaim input VAT on purchases related to making exempt supplies. Non-vatable (T9) is completely outside the scope of VAT, with no input VAT involved.

Q2: Can I reclaim VAT on purchases coded T9?

No. By definition, T9 items are non-vatable, meaning no VAT was ever charged on them in the first place. Therefore, there is no VAT to reclaim.

Q3: What happens if I use the wrong VAT code?

Using the wrong VAT code can lead to incorrect VAT calculations. If you underpay VAT, HMRC may charge interest and penalties. If you overpay, you'll be missing out on money your business could have reclaimed. It can also lead to discrepancies in your accounts that make audits more difficult.

Q4: How do I know which code to use for a specific transaction?

Always refer to HMRC's official guidance on VAT rates and categories. If you're unsure, especially for complex transactions, it's best to consult a qualified accountant or VAT specialist. For common items, your accounting software's default settings or a quick search can often provide clarity.

Q5: Do I need to keep records for T0 and T9 transactions?

Absolutely. While T9 transactions don't directly impact your VAT liability, they are still part of your business's financial records. All transactions, regardless of their VAT treatment, must be recorded accurately for tax purposes and general financial management. For T0 transactions, detailed records are crucial to justify the zero-rated treatment and any associated input VAT claims.

Conclusion

Mastering the difference between T0 (zero-rated) and T9 (non-vatable) is more than just an accounting chore; it's a fundamental aspect of sound financial management for any UK business. While both codes signify that no VAT is charged to the customer, their underlying legal definitions and implications for input VAT recovery and VAT return reporting are vastly different. Zero-rated items are still within the VAT system, just at a 0% rate, allowing for input VAT recovery, whereas non-vatable items are entirely outside its scope, with no VAT implications whatsoever.

By meticulously applying the correct codes, you ensure your VAT returns are accurate, avoid potential penalties, and maintain clear, compliant financial records. When in doubt, always err on the side of caution and seek professional advice. Your business's financial health depends on it.

If you want to read more articles similar to UK VAT Codes: Decoding T0 and T9 Explained, you can visit the Automotive category.