12/10/2009

In the intricate world of UK business, Value Added Tax (VAT) is a constant presence. For mechanics and garage owners, navigating the various VAT rates is not just about compliance; it's about understanding your financial landscape. One particular VAT rate that often causes confusion is 'zero-rated' VAT. While it might seem illogical – a tax that exists but is charged at 0% – it's a vital component of the UK tax system, offering the government flexibility over the cost of goods and services to the end customer. For your garage, understanding this distinction is crucial, not least because it can significantly impact your ability to reclaim input VAT.

Zero-rated VAT means that while a supply of goods or services is still considered 'vatable,' the actual rate of VAT charged to the customer is 0%. This isn't the same as being 'exempt' from VAT, and that distinction is paramount for any business, particularly those in the automotive sector, which primarily deals with standard-rated supplies. Think of it as a special category within the VAT system, where the transaction is recognised for VAT purposes, but no tax is actually added to the price.

- Zero-Rated vs. Exempt vs. Standard-Rated: A Crucial Distinction

- Why Does Zero-Rating Exist? The Government's Flexibility

- Zero-Rated VAT and the Automotive Sector: Niche Applications

- The Importance of Understanding Zero-Rating for Garages

- Input VAT Recovery: A Key Advantage

- Record Keeping and Compliance

- Common Misconceptions and Pitfalls

- Frequently Asked Questions (FAQs)

Zero-Rated vs. Exempt vs. Standard-Rated: A Crucial Distinction

To truly grasp zero-rated VAT, it's essential to differentiate it from other VAT categories. Misunderstanding these can lead to costly errors in your VAT returns and compliance. Here’s a breakdown:

- Standard-Rated VAT: This is the most common rate for goods and services in the UK, currently set at 20%. Most car parts, vehicle repairs, and servicing charges fall into this category. When you charge a customer for a new clutch or an MOT, you'll typically add 20% VAT to the net price.

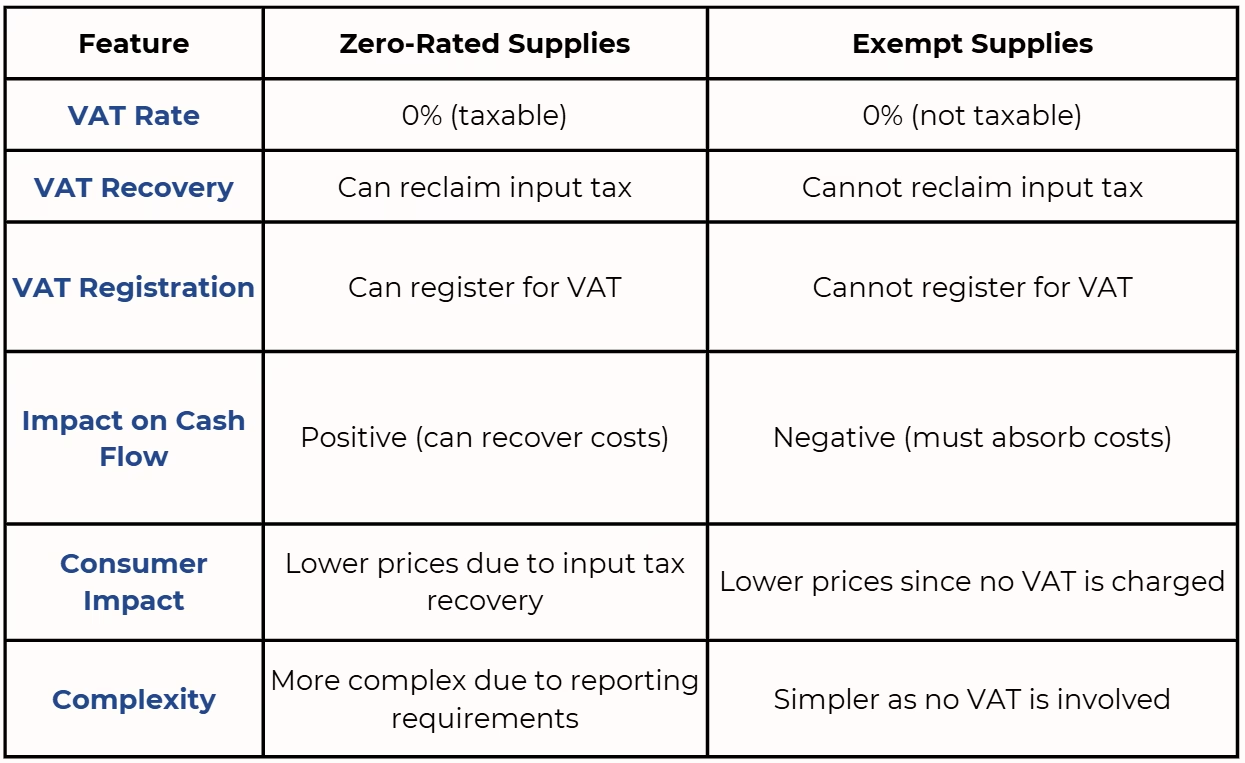

- Zero-Rated VAT: As discussed, this means VAT is charged at 0%. While no VAT is added to the customer's bill, the supply is still considered a taxable supply for VAT purposes. The critical advantage for a business making zero-rated supplies is that they can still reclaim any input VAT they've paid on their purchases related to these supplies. Examples include most food (not restaurant meals), children's clothing, books, and new house construction.

- Exempt VAT: This is where a supply is outside the scope of VAT entirely. No VAT is charged, but crucially, a business making only exempt supplies cannot reclaim any input VAT on purchases related to those supplies. Common examples include insurance, most financial services, and certain types of education or health services. For a garage, understanding this is important because if you were to offer an exempt service, you wouldn't be able to reclaim VAT on the tools or materials used for that specific service.

The table below provides a clear comparison:

| VAT Category | Rate Applied | Input VAT Recovery? | Example (General) | Example (Automotive - Niche) |

|---|---|---|---|---|

| Standard-Rated | 20% | Yes | Electronics, clothing, car repairs | Most car parts & labour |

| Zero-Rated | 0% | Yes | Most food, books, children's clothes | Exported vehicles/parts |

| Exempt | N/A (outside scope) | No | Insurance, financial services | Certain charity-specific supplies (very rare for garages) |

The ability to reclaim input VAT is the defining feature that makes zero-rated VAT immensely beneficial for businesses compared to exempt supplies. It ensures that businesses involved in specific supply chains aren't disadvantaged by VAT on their inputs, even if their outputs are not generating VAT revenue for the government.

Why Does Zero-Rating Exist? The Government's Flexibility

The rationale behind zero-rated VAT is rooted in governmental policy and economic flexibility. It allows the government to influence the cost of essential goods and services without removing them entirely from the VAT system. By zero-rating certain items, the government can effectively make them cheaper for consumers (as no VAT is added), or encourage specific activities without creating a tax burden on the businesses supplying them. For example, zero-rating food makes essential groceries more affordable. For businesses, including potentially your garage, it means that while you don't charge output VAT on these specific supplies, you are still very much part of the VAT chain and can recover your input VAT, which is a significant cash flow advantage.

Zero-Rated VAT and the Automotive Sector: Niche Applications

It's important to clarify upfront: for the vast majority of car maintenance, servicing, and parts sales within the UK, the standard 20% VAT rate applies. Your garage will almost certainly charge 20% VAT on routine repairs, MOTs, and replacement parts. However, there are specific, albeit niche, scenarios where zero-rated VAT can apply within the automotive sector, and understanding these can be crucial for a well-rounded business:

1. Exports of Vehicles or Parts

Perhaps the most common scenario where a UK garage might encounter zero-rated VAT is when exporting vehicles or parts outside of the UK. If you sell a car or a significant batch of spare parts to a customer who is taking them out of the UK, that supply can be zero-rated for VAT purposes. However, strict conditions apply:

- Proof of Export: You must obtain and keep sufficient evidence that the goods have left the UK. This could include transport documents, customs declarations, or evidence of payment from an overseas customer.

- Customer Status: The rules vary slightly depending on whether the customer is an individual, a business in the EU, or a business outside the EU.

For a garage that occasionally deals with international buyers or specialises in classic car sales where buyers might be overseas, mastering the rules for zero-rating exports is vital to avoid incorrectly charging VAT and then having to issue refunds, or worse, incurring penalties from HMRC for non-compliance.

2. Certain Vehicles for Disabled Persons

Under very specific circumstances, the supply of certain vehicles and adaptations for disabled persons can be zero-rated. This is a highly specialised area and typically applies to vehicles designed or substantially adapted for use by a disabled person in a wheelchair, or for specific charities. While not every garage will deal with this, those specialising in vehicle adaptations or mobility solutions must be aware of these rules.

3. Supplies to Charities (Under Specific Conditions)

In extremely limited situations, certain supplies to eligible charities can be zero-rated. This usually applies to specific building works or equipment for medical or veterinary research, or vehicles designed or adapted to carry 12 or more people. It's rare for standard car maintenance to fall into this category, but if your garage undertakes very specific work for a qualifying charity, it’s worth investigating.

It cannot be stressed enough: for your day-to-day operations – fixing a gearbox, replacing brake pads, or performing a routine service – you will almost certainly be charging the standard 20% VAT. The zero-rated scenarios are exceptions, not the rule, for most UK garages.

The Importance of Understanding Zero-Rating for Garages

Even if zero-rated supplies are a small part of your business, understanding them is crucial for several reasons:

- Accurate Invoicing: Incorrectly applying VAT can lead to undercharging (losing profit), overcharging (customer dissatisfaction and potential refunds), or HMRC penalties.

- Correct VAT Returns: Your VAT return must accurately reflect all types of supplies. Misclassifying zero-rated sales as standard-rated or exempt can lead to incorrect declarations.

- Input VAT Recovery: This is arguably the biggest benefit. If you make zero-rated supplies, you can still reclaim the input VAT on all the parts, tools, and overheads related to those supplies. For example, if you export a vehicle, you can reclaim the VAT on the new tyres, servicing parts, and even the fuel used to transport it, provided you have valid VAT invoices. This greatly improves your cash flow compared to making exempt supplies, where input VAT cannot be recovered.

- Avoiding Penalties: HMRC takes VAT compliance very seriously. Errors, especially repeated ones, can result in significant fines.

Input VAT Recovery: A Key Advantage

Let's delve deeper into the significant advantage of input VAT recovery when making zero-rated supplies. When your garage makes a standard-rated supply (e.g., a car service), you charge 20% VAT to your customer (output VAT). You also pay VAT on your purchases, like diagnostic equipment, workshop consumables, and rent (input VAT). At the end of a VAT period, you typically pay HMRC the difference between your output VAT and your input VAT.

Now, consider a zero-rated supply, such as exporting a classic car to a buyer in the USA. You charge 0% VAT to the customer, meaning you have no output VAT from that sale. However, during the restoration and preparation of that car for export, you would have paid 20% VAT on numerous items: specialist parts, paint, tools, potentially even specific shipping materials. Because the export is zero-rated (rather than exempt), you are still entitled to reclaim all that input VAT from HMRC. This is a direct financial benefit, reducing your overall costs and improving your profit margin on such sales. If the supply were exempt, you would not be able to reclaim that VAT, making the transaction less profitable.

Record Keeping and Compliance

Meticulous record keeping is non-negotiable when dealing with zero-rated supplies. For exports, for instance, HMRC requires robust evidence that the goods have actually left the UK. This typically includes:

- A copy of the sales invoice showing the zero-rated VAT.

- Proof of payment from the overseas customer.

- Transport documents (e.g., bill of lading, air freight note, road consignment note) showing the destination outside the UK.

- Customs declarations or export entries.

Without this evidence, HMRC could deem the supply to have been incorrectly zero-rated and demand the VAT you should have charged at the standard rate, plus potential penalties. Regular review of your VAT processes and, if in doubt, seeking professional advice, can save your garage from significant financial headaches.

Common Misconceptions and Pitfalls

- "No VAT means zero-rated": This is a dangerous assumption. Just because a transaction doesn't have VAT added doesn't mean it's zero-rated. It could be outside the scope of VAT entirely, or it could be exempt. The key difference lies in whether input VAT can be recovered.

- Confusing zero-rated with exempt: As detailed, these are fundamentally different for your business's finances. Always verify the correct VAT treatment.

- Assuming all international sales are zero-rated: While many exports are, there are specific rules for different countries (e.g., EU vs. non-EU) and types of goods. Always check current HMRC guidance.

- Not keeping sufficient evidence: For zero-rated supplies, particularly exports, the burden of proof is on your business. Lack of evidence can lead to HMRC reassessing the supply and demanding VAT.

Frequently Asked Questions (FAQs)

- Is standard car servicing zero-rated for VAT?

- No. Standard car servicing, repairs, and the sale of most car parts in the UK are subject to the standard rate of VAT, which is currently 20%.

- Can I zero-rate VAT on car parts I sell to a customer living in another country?

- Yes, provided the goods are physically exported outside the UK and you hold sufficient evidence of export, you can zero-rate the VAT on those parts. Specific rules apply depending on the destination (e.g., EU or non-EU).

- Do I still need to register for VAT if all my supplies are zero-rated?

- Yes. If your taxable turnover (including zero-rated supplies) exceeds the VAT registration threshold, you must still register for VAT. The benefit is that you will then be able to reclaim input VAT on your purchases.

- What happens if I incorrectly zero-rate a supply?

- If HMRC discovers that you have incorrectly zero-rated a supply, they can assess your business for the VAT that should have been charged, plus potential penalties and interest. This is why accurate record-keeping and understanding the rules are so important.

- Does zero-rated VAT apply to electric vehicles or their charging?

- No, not generally. The sale of new or used electric vehicles and the electricity used for charging them are typically subject to standard-rate VAT, just like petrol or diesel vehicles.

In conclusion, while the average UK garage might rarely deal with zero-rated supplies, understanding this concept is paramount for comprehensive financial management. It highlights the nuances of the VAT system and, crucially, underscores your right to reclaim input VAT, a significant financial lever for any business. By distinguishing between zero-rated, standard-rated, and exempt supplies, and by maintaining meticulous records for every transaction, your garage can ensure full compliance with HMRC regulations, optimise its cash flow, and confidently navigate the complexities of the UK tax landscape.

If you want to read more articles similar to Understanding Zero-Rated VAT for UK Mechanics, you can visit the Automotive category.