08/04/2007

It's a stressful situation for any driver: you're involved in a road traffic accident, and the damage to your vehicle is so severe that the insurance company declares it a 'write-off'. Even more disheartening is when the accident wasn't your fault. This means another driver's negligence caused the damage, and you're left without your car and facing a complicated insurance process. But what exactly happens in this scenario, and what are your rights when the blame lies elsewhere? This article will guide you through the process, ensuring you understand your options and how to secure fair compensation.

- Understanding the 'Write-Off'

- Your Rights When It's Not Your Fault

- Navigating the Claim Process: Key Considerations

- Comparison: Your Insurer vs. At-Fault Party's Insurer

- Frequently Asked Questions

- Q1: What if the at-fault driver is uninsured?

- Q2: Can I get a brand new car if mine is written off?

- Q3: How is the pre-accident value calculated?

- Q4: What if I disagree with the category of the write-off (e.g., think it should be repairable)?

- Q5: Do I have to accept the first offer from the insurer?

Understanding the 'Write-Off'

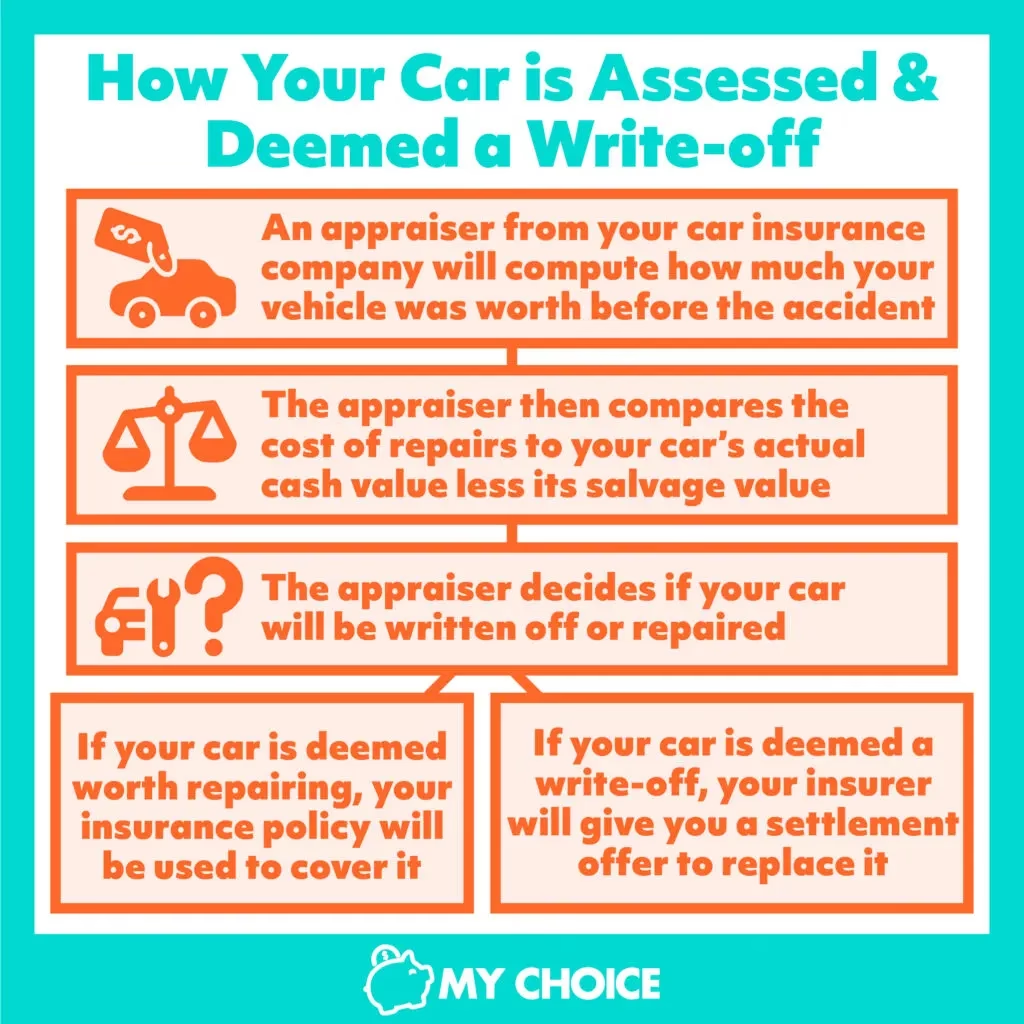

Before delving into the specifics of not-at-fault write-offs, it's crucial to understand what a 'write-off' actually means. In the UK, a vehicle is declared a write-off when the cost of repairing it exceeds its market value. This is often referred to as being 'economically unviable' to repair. Insurers categorise write-offs into two main types:

- Category A: This is the most severe category. The vehicle is considered scrap and must be destroyed. No parts can be salvaged.

- Category B: The vehicle is also badly damaged and cannot be returned to the road. However, some parts may be salvaged for reuse.

- Category S (previously Category C): Structural damage. The vehicle can be repaired, but the cost of repairs was significant. It can be put back on the road after repairs and inspection.

- Category N (previously Category D): Non-structural damage. The vehicle can be repaired, and the damage was not structural. It can be put back on the road after repairs and inspection.

When your car is deemed a write-off, your insurer will offer you a settlement based on its pre-accident market value. This value is determined by factors such as the car's age, mileage, condition, and any optional extras it had. It's important to remember that this is the value of the car *before* the accident occurred.

Your Rights When It's Not Your Fault

The good news when an accident isn't your fault is that you shouldn't be out of pocket. The responsibility for compensating you for your vehicle lies with the insurance company of the driver who caused the accident. This is where the process can differ slightly from a claim made on your own policy.

Instead of your own insurer paying out and then attempting to recover the costs from the other party (which is what happens in a 'first-party' claim), you will typically deal directly with the 'at-fault' party's insurer. This is known as a 'third-party' claim.

Here's what you can expect:

1. Reporting the Accident

The first step, regardless of fault, is to report the accident to the police if there are any injuries or if the road is blocked. You should also exchange details with the other driver, including their name, address, insurance details, and vehicle registration number. If they are unwilling to provide details or admit fault, reporting to the police is even more crucial.

2. Informing Your Insurer

Even though the accident wasn't your fault, it's essential to inform your own insurance company. They can advise you on the best course of action and may even be able to manage the claim on your behalf through a process called 'subrogation'. This means they will handle the communication and recovery from the third-party insurer, which can often be a smoother and quicker process for you.

3. The Write-Off Assessment

The at-fault party's insurer will arrange for an assessment of your vehicle. This assessment will determine if the car is a write-off and its pre-accident value. You have the right to be present during this inspection or to have your own mechanic present to ensure a fair assessment is made.

4. Settling the Claim

Once the vehicle is declared a write-off, the insurer will offer you a settlement amount based on the pre-accident value. This is where you need to be vigilant. The initial offer might not be the best you can get. It's crucial to research the market value of comparable vehicles in similar condition to yours. Websites like Glass's Guide, Parkers, and Auto Trader can be invaluable for this.

If you believe the offer is too low, you should politely but firmly negotiate. Provide evidence of your research to support your valuation. If you are still unable to reach an agreement, you can escalate the complaint through the insurer's internal complaints procedure. If that fails, you can take your complaint to the Financial Ombudsman Service (FOS), which is a free and impartial service.

5. Keeping Your Car (Salvage)

In some cases, you might want to keep your written-off car. This is known as 'taking the salvage'. If you choose this option, the insurer will deduct the salvage value (what the car is worth as scrap) from the settlement offer. For example, if your car's market value is £5,000 and its salvage value is £500, you would receive £4,500 if you keep the car.

However, if your car is a Category A or B write-off, you cannot keep it. If it's a Category S or N, you might be able to keep it, but you'll need to ensure it's properly repaired and inspected before it can be returned to the road.

6. Associated Costs and Losses

When your car is written off, you may be entitled to claim for other losses in addition to the value of your car. These can include:

- Hire Car: If the accident was not your fault, you are generally entitled to a like-for-like replacement vehicle from the at-fault party's insurer while your claim is being settled or your car is being repaired. If your own insurer provides you with a courtesy car, they will usually seek to recover the cost from the third party.

- Loss of Use: In some circumstances, you may be able to claim for 'loss of use' if you rely on your vehicle for business purposes.

- Out-of-Pocket Expenses: Keep receipts for any reasonable expenses incurred as a direct result of the accident, such as taxi fares if you couldn't get a hire car immediately.

Dealing with an insurance claim can be complex. Here are some tips to make the process smoother:

a) Document Everything

Keep meticulous records of all communication with both your insurer and the at-fault party's insurer. Note down dates, times, names of people you spoke to, and what was discussed. Also, keep copies of all letters and emails.

b) Be Patient but Persistent

Third-party claims can sometimes take longer than direct claims with your own insurer, especially if liability is disputed. However, don't let the process drag on indefinitely. Follow up regularly and escalate if necessary.

c) Consider a Claims Management Company

If you find the process overwhelming, you might consider using a specialist car insurance claims management company. They can handle the entire process for you, often securing a better settlement and faster resolution. Be aware of their fees, which are usually deducted from your settlement.

d) Know Your Insurer's Obligations

Your insurer has a duty of care to you. If they are not handling your claim efficiently or fairly, don't hesitate to make your dissatisfaction known.

Comparison: Your Insurer vs. At-Fault Party's Insurer

Here's a brief comparison of what to expect when claiming through your own policy versus the at-fault party's insurer:

| Feature | Claiming via Your Insurer (At-Fault Party's Insurer) | Claiming Directly via At-Fault Party's Insurer (Third-Party Claim) |

|---|---|---|

| Process Initiator | Your insurer | You or your appointed representative |

| Primary Contact | Your insurer | At-fault party's insurer |

| Potential for Faster Resolution | Often yes, if your insurer has good relationships with others. | Can be slower if liability is disputed or insurer is uncooperative. |

| Courtesy Car Provision | Usually provided by your insurer (and they recover costs). | Provided by the at-fault insurer (direct arrangement). |

| Your insurer's Role | Manages the claim and recovers costs. | Your insurer may offer assistance but the primary claim is yours. |

| Risk of Lower Settlement | Less likely if your insurer is proactive. | Higher risk if you don't research and negotiate effectively. |

Frequently Asked Questions

Q1: What if the at-fault driver is uninsured?

If the at-fault driver is uninsured, you will need to make a claim through the Motor Insurers' Bureau (MIB). The MIB is a body set up to compensate victims of uninsured and untraced drivers. Your own insurer might assist you with this process.

Q2: Can I get a brand new car if mine is written off?

Generally, no. You will be compensated based on the pre-accident market value of your specific car. You cannot get a brand-new replacement unless your policy specifically includes a 'new for old' clause, which is rare for cars over a certain age.

Q3: How is the pre-accident value calculated?

Insurers use various sources to calculate this, including industry guides (like Glass's Guide), auction data, and advertisements for similar vehicles. They will consider the car's age, mileage, condition, service history, and any optional extras.

Q4: What if I disagree with the category of the write-off (e.g., think it should be repairable)?

If you believe your car can be repaired economically, you should present your case to the insurer with evidence from a qualified mechanic. If you still disagree, you can seek an independent engineer's report, though this will incur a cost. If the insurer insists on a write-off category, you can escalate your complaint.

Q5: Do I have to accept the first offer from the insurer?

Absolutely not. The first offer is often a starting point for negotiation. Always do your own research into the market value of your vehicle before accepting any offer.

Being involved in an accident where your car is written off, even when it's not your fault, can be a trying experience. However, by understanding your rights, the claims process, and by being prepared to negotiate assertively, you can ensure you receive fair compensation for your vehicle and any other associated losses. Remember to document everything, stay informed, and don't hesitate to seek assistance if you need it.

If you want to read more articles similar to Car Written Off: What Happens When It's Not Your Fault?, you can visit the Insurance category.