06/10/2007

As a responsible driver in the United Kingdom, you're likely aware of the twin pillars of vehicle legality: a valid MOT certificate and comprehensive car insurance. Both are non-negotiable legal requirements designed to ensure road safety and financial protection. However, a common point of confusion arises when these two obligations seemingly intersect: does an invalidated MOT certificate automatically void your car insurance? It's a question that can cause considerable anxiety, especially if you find yourself in a situation where your MOT has lapsed. While the immediate answer might surprise you, the implications are far more complex than a simple 'yes' or 'no.' Understanding the intricate relationship between your MOT status and your insurance policy is crucial for every UK motorist, not only to remain legally compliant but also to safeguard yourself against potentially devastating financial repercussions in the event of an incident.

- The Legal Landscape: MOT vs. Insurance

- Policy Clauses and Contractual Obligations

- The Impact on Insurance Claims

- Understanding 'Unroadworthy' and Its Implications

- Driving Without an MOT: Penalties Beyond Insurance

- Maintaining Vehicle Roadworthiness: More Than Just an MOT

- Proactive Steps to Ensure Compliance

- Frequently Asked Questions (FAQs)

The Legal Landscape: MOT vs. Insurance

To truly grasp the dynamic between an MOT certificate and your car insurance, it's essential to recognise them as distinct legal entities, albeit ones that share a common goal of road safety. In the UK, the MOT test, or Ministry of Transport test, is a legal requirement under the Road Traffic Act 1988. Its primary purpose is to ensure that vehicles over three years old meet minimum roadworthiness and environmental standards. It's a snapshot in time, assessing critical components like brakes, steering, lights, tyres, and emissions. Failing an MOT or driving without a valid certificate for a vehicle that requires one is a serious offence, punishable by hefty fines and points on your licence.

Conversely, car insurance is also a mandatory requirement under the same Road Traffic Act 1988. Its purpose is fundamentally different: it provides financial protection against liabilities arising from accidents or other unforeseen events. When you purchase car insurance, you enter into a legally binding contract with an insurer. This contract outlines the terms and conditions under which your vehicle is covered. The crucial point here is that these two legal frameworks operate independently. Your insurance policy is a contract for financial risk mitigation, while the MOT certificate is a statutory declaration of vehicle roadworthiness. This separation means that, in most cases, an expired MOT does not automatically trigger the immediate cancellation or voiding of your insurance policy by default.

MOT vs. Car Insurance: Key Distinctions

| Feature | MOT Certificate | Car Insurance Policy |

|---|---|---|

| Purpose | Verifies vehicle roadworthiness and environmental standards at a point in time. | Provides financial protection against liabilities and damages from accidents/events. |

| Governing Law | Road Traffic Act 1988 (for inspections). | Road Traffic Act 1988 (for mandatory cover). |

| Frequency | Annually (for vehicles over 3 years old). | Typically annually, renewed via contract. |

| What's Tested/Covered | Brakes, tyres, lights, steering, suspension, emissions, etc. | Damage to your vehicle, third-party vehicles/property, personal injury, theft, fire. |

| Immediate Impact of Lapsing | Illegal to drive (except to MOT test/repairs). Risk of fines/points. | Policy remains active, but potential for claims issues if conditions are breached. |

Policy Clauses and Contractual Obligations

While an expired MOT doesn't inherently nullify your insurance, the devil, as they say, is in the detail – specifically, the clauses within your insurance policy. When you sign up for car insurance, you agree to abide by certain conditions. These conditions are designed to ensure that the risk profile of your vehicle remains consistent with what the insurer has agreed to cover. Many insurance providers include specific policy clauses in their policy documents that relate to the vehicle's roadworthiness and legal compliance.

For instance, a common clause might state that 'the insured vehicle must be maintained in a roadworthy condition at all times' or 'you must ensure your vehicle holds a valid MOT certificate where legally required.' If such a clause exists in your policy and you are driving without a valid MOT, you are technically in breach of contract. This doesn't mean your policy is instantly void, but it gives the insurer grounds to take action. The insurer might argue that by not having a valid MOT, you have failed to uphold your end of the agreement, potentially increasing the risk they are insuring.

The consequences of such a breach can vary. In less severe cases, they might issue a warning. More seriously, they could cancel your policy, though this is often a last resort and typically comes with prior notification. The most significant implication, however, arises when you need to make a claim. This is where the absence of a valid MOT can become a critical hurdle.

The Impact on Insurance Claims

This is arguably the most critical aspect for any motorist. If you are involved in an accident while driving a vehicle without a valid MOT, and you need to make an insurance claim, the situation becomes significantly more complicated. Even if your policy hasn't been automatically voided, the insurer will launch an investigation into the circumstances of the incident. During this investigation, one of the first things they will check is the legal status of your vehicle, including its MOT validity.

If the insurer discovers that your vehicle did not have a valid MOT certificate at the time of the incident, they may argue that the vehicle was unroadworthy. This is a crucial distinction. While the MOT certificate itself is a legal document, its absence can be indicative of an underlying lack of roadworthiness. If the accident can be directly or indirectly attributed to a defect that an MOT test would have identified – for example, faulty brakes, worn tyres, or steering issues – the insurer has strong grounds to reject your claim entirely.

Even if the absence of the MOT is not directly related to the cause of the accident (e.g., you were rear-ended by another driver), the insurer might still seek to reduce the payout or refuse to pay for your damages, citing your breach of contract regarding the vehicle's roadworthiness. They might argue that by driving an un-MOT'd vehicle, you were operating outside the terms of your agreement, thereby increasing the overall risk. In such a scenario, you could find yourself personally liable for significant repair costs, medical expenses for yourself and third parties, and even legal fees. This financial exposure underscores the immense importance of maintaining a current MOT certificate.

Understanding 'Unroadworthy' and Its Implications

The concept of 'unroadworthy' is central to how an insurer might handle a claim when an MOT is missing. A vehicle is considered unroadworthy if it has defects that make it unsafe to drive on public roads. An MOT test is specifically designed to check for these types of defects. Therefore, if your vehicle doesn't have a valid MOT, it implicitly suggests that its roadworthiness has not been officially confirmed.

However, it's important to note that a vehicle can be unroadworthy even if it has a valid MOT certificate (e.g., a new defect develops the day after the MOT). Conversely, a vehicle could be technically roadworthy but still lack an MOT. The challenge, from an insurance perspective, is proving the former and disproving the latter without the official stamp of an MOT. Without that certificate, the burden of proof shifts heavily onto the policyholder to demonstrate that their vehicle was indeed safe and legal at the time of the incident, which can be an incredibly difficult task, particularly if there are any mechanical issues involved in the accident.

Driving Without an MOT: Penalties Beyond Insurance

Beyond the severe implications for your insurance coverage, driving without a valid MOT certificate carries its own set of significant legal penalties. It is a criminal offence. The police use Automatic Number Plate Recognition (ANPR) cameras, which are linked to the MOT database, making it very easy for them to identify vehicles without a current certificate.

If caught, you could face a fine of up to £1,000. If your vehicle is found to be dangerous, meaning it has a 'dangerous' defect that would cause it to fail an MOT, the fine can increase to £2,500, and you could receive three penalty points on your driving licence. In severe cases, particularly if the dangerous defect contributes to an accident, you could even face a driving ban. These penalties are entirely separate from any action your insurance company might take, highlighting that an MOT is not merely an administrative formality but a fundamental aspect of road safety and legal compliance.

Maintaining Vehicle Roadworthiness: More Than Just an MOT

While the MOT is a crucial annual check, maintaining your vehicle's roadworthiness is an ongoing responsibility. An MOT certificate is only valid for 12 months, and a lot can happen in that time. Regular vehicle servicing, routine checks (like tyre pressure, oil levels, and lights), and promptly addressing any warning lights or unusual noises are all vital.

Think of the MOT as a thorough annual health check-up, but your daily diligence is what keeps your vehicle healthy between those appointments. This proactive approach not only helps ensure you pass your next MOT with ease but, more importantly, keeps you and other road users safe. It also reinforces your position with your insurer that you are a responsible vehicle owner, upholding your end of the policy agreement by maintaining your vehicle.

Proactive Steps to Ensure Compliance

Given the complexities and potential pitfalls, taking proactive steps to ensure your vehicle is always compliant is paramount.

- Check Your MOT Expiry Date: Make it a habit to know when your MOT is due. You can get an MOT up to one month (minus one day) before it runs out and keep the same expiry date. The government also offers a free online tool to check your vehicle's MOT history and expiry date.

- Schedule Your MOT Early: Don't wait until the last minute. Book your test in advance to allow time for any necessary repairs. Many reputable garages offer convenient booking options.

- Review Your Insurance Policy: Thoroughly read your policy documents, paying close attention to clauses related to vehicle maintenance, roadworthiness, and MOT requirements. If anything is unclear, contact your insurer directly for clarification.

- Regular Vehicle Checks: Perform basic checks regularly. Ensure your tyres are correctly inflated and have adequate tread, all lights are working, and fluid levels are correct.

- Address Issues promptly: Don't ignore warning lights or unusual noises. Getting problems fixed quickly can prevent them from escalating and potentially impacting your vehicle's roadworthiness.

Frequently Asked Questions (FAQs)

Q: Can I drive my car to an MOT appointment if its MOT has expired?

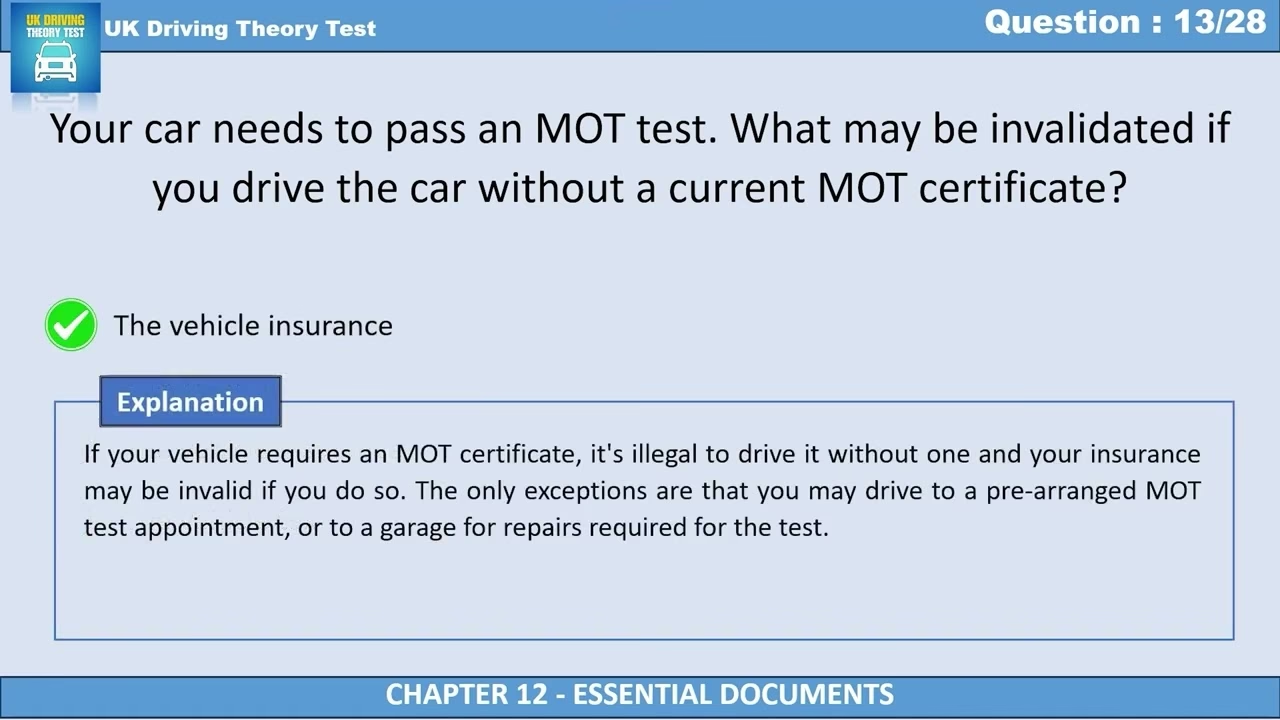

A: Yes, you can. The only circumstance under which you can drive a vehicle without a valid MOT is directly to a pre-booked MOT test, or to a garage for repairs required for its MOT. You must have proof of your appointment. If stopped by the police, you will need to demonstrate that you are on your way to or from the test or repair. Driving for any other purpose with an expired MOT is illegal.

Q: What if my car fails its MOT? Can I still drive it?

A: It depends on the nature of the defects. If your car fails with 'dangerous' defects, you cannot drive it until the dangerous defects have been repaired. Driving a vehicle with dangerous defects is illegal and highly risky. If it fails with 'major' defects, you can drive it away if your previous MOT certificate is still valid and no dangerous defects were found. However, it's always advisable to get the repairs done immediately. If your previous MOT has expired, or if dangerous defects were found, you cannot drive it until the repairs are made and it passes a re-test.

Q: Does my insurance cover me if my MOT expired just yesterday?

A: As discussed, your insurance policy is not automatically voided simply because your MOT expired. However, if you are involved in an incident, and your vehicle is found to have been unroadworthy, or if your policy has a strict clause requiring a valid MOT at all times, your claim could still be rejected or reduced. It's always best to renew your MOT before it expires.

Q: What's the difference between an MOT and a service?

A: An MOT is a legal inspection that checks the roadworthiness of your vehicle at a specific point in time, focusing on safety and environmental standards. It does not involve changing parts or fluids. A service, on the other hand, is routine maintenance performed by a mechanic, which typically includes changing oil, filters, and checking various components for wear and tear. While a service can help your car pass its MOT, they are distinct processes. A service maintains your vehicle's health; an MOT certifies its safety for the road.

Q: How can I check my vehicle's MOT status and history?

A: You can easily check the MOT status and history of any vehicle registered in Great Britain online via the official government website. You'll need the vehicle's registration number (number plate). This service provides details on current MOT status, expiry dates, and previous test results, including any advisories.

In summary, the relationship between an invalidated MOT certificate and your car insurance is more nuanced than a simple voiding of your policy. While your insurance isn't automatically cancelled the moment your MOT expires, driving without a valid MOT is a serious breach of legal requirements and can have severe implications for your insurance coverage, particularly if you need to make a claim. Insurers often include clauses requiring vehicles to be roadworthy and legally compliant, and failing to meet these conditions can lead to claims being rejected, reduced payouts, or even policy cancellation. Beyond insurance, the legal penalties for driving without an MOT are substantial. The safest and most responsible course of action is always to ensure your vehicle has a current and valid MOT certificate. This not only keeps you compliant with UK law but also offers crucial peace of mind that your vehicle is safe to drive and that your insurance will protect you when you need it most. Always review your specific insurance policy terms and conditions, and when in doubt, consult your insurer for definitive guidance.

If you want to read more articles similar to MOT & Insurance: Is Your Car Cover Valid?, you can visit the Insurance category.