22/02/2006

For many car enthusiasts across the UK, personalising a vehicle is part of the joy of ownership. Whether it’s boosting performance, enhancing aesthetics, or adding extra security, modifications offer a way to make a car truly your own. However, this journey of customisation often brings with it a crucial question: how do these changes affect your car insurance? It's a question fraught with potential pitfalls and significant financial implications, and understanding the nuances is vital for any car owner considering an upgrade.

The simple answer is yes, modifications almost always affect your car insurance. But the extent of that impact can vary wildly, depending on the nature of the modification, your insurer, and even how you drive. Failing to inform your insurance provider about any changes, no matter how minor you perceive them to be, can have severe consequences, potentially invalidating your policy and leaving you uninsured in the event of an accident. This comprehensive guide will delve into everything you need to know about car modifications and their intricate relationship with your insurance in the United Kingdom.

- What Exactly Counts as a Car Modification?

- The Golden Rule: Always Declare Your Modifications

- Why Do Modifications Affect Your Insurance Premiums?

- Modifications That Typically Increase Your Premiums

- Modifications That Could Lower or Not Affect Your Premiums

- Comparative Table: Impact of Common Modifications

- The Pitfalls of Undisclosed Modifications

- Seeking Specialist Modified Car Insurance

- Frequently Asked Questions (FAQs)

- Conclusion

What Exactly Counts as a Car Modification?

Before we explore the impact on insurance, it’s important to clarify what constitutes a modification. Generally, any feature or part added to your car that wasn't provided by the manufacturer as standard or as an optional extra at the point of sale is considered an 'aftermarket part' or a modification. This definition is broader than many people might initially assume, encompassing a vast array of changes:

- Performance Enhancements: Anything that alters the car's power, speed, or handling.

- Aesthetic Changes: Visual upgrades that change the car's appearance.

- Safety & Security Features: Additions designed to protect the car or its occupants.

- Practical Additions: Features that improve the car's functionality.

From a simple sticker to a full engine remap, almost anything that deviates from the factory specification falls under the umbrella of a modification. And if it's a modification, your insurer needs to know about it.

The Golden Rule: Always Declare Your Modifications

This cannot be stressed enough: the most important piece of advice for any modified car owner is to always declare any and all modifications to your insurance provider. Ideally, you should do this *before* you make the change. This allows your insurer to assess the impact on your premium and confirm they are willing to cover the modification.

Why is this so crucial? Insurance policies are based on the information you provide about your vehicle at the time of application. If that information changes, and you don't update your insurer, you are effectively driving a car that doesn't match the description on your policy. In the eyes of the law, this can be seen as driving without valid insurance. Should you be involved in an accident, even if it's not your fault, your insurer could refuse to pay out your claim, leaving you with hefty repair bills, potential third-party costs, and a voided policy. It's simply not worth the risk.

Insurance companies assess risk. When you modify your car, you change its risk profile. Here are the primary reasons why modifications influence your premiums:

Increased Value

Many modifications, especially high-end performance parts or custom bodywork, significantly increase the financial value of your vehicle. Should your car be stolen or written off, the insurer would have to pay out more to replace or repair it, including the cost of the modifications. This higher potential payout directly translates to higher premiums.

Safety Concerns & Increased Risk

Insurers can't be certain about the quality or impact of aftermarket parts. They don't know if parts have been fitted correctly, how they'll perform under stress, or if they compromise the car's original safety features. For example, modifications designed to make a car faster inherently increase the risk of accidents. One survey suggested that a higher percentage of modified car drivers have been in accidents. Features like bull bars, while seemingly protective, can increase the risk of injury to pedestrians or cyclists in a collision, raising the insurer's liability.

Theft Risk

Flashy or expensive modifications, such as custom alloy wheels, high-spec sound systems, or unique paint jobs, can make your car more appealing to thieves. A higher risk of theft means a higher chance of the insurer having to pay out, thus increasing your premium.

Performance Enhancements

Any modification that boosts your car's power, speed, or handling capabilities will almost certainly lead to higher premiums. Insurers associate more powerful vehicles with a greater likelihood of being driven aggressively or involved in high-speed incidents. This includes engine remapping, turbocharger additions, sports exhausts, and upgraded suspension systems.

Most modifications will lead to an increase in your insurance costs. Here's a breakdown of common types that insurers view as increasing risk:

- Engine Upgrades: This includes supercharging, turbocharging, ECU (Engine Control Unit) remaps, performance chips, and induction kits. These significantly alter the car's power output.

- Exhaust Systems: Altered exhaust systems, such as cat-back systems, manifolds, or sports exhausts, can increase noise and performance. According to one specialist insurer, exhaust system changes can inflate premiums by around 26%.

- Suspension and Chassis Modifications: Coilovers, air ride systems, adjustable arms, strut braces, and uprated anti-roll bars change the car's handling characteristics, which insurers will want to assess.

- Brake Upgrades: While improved braking might seem safer, upgraded discs, pads, and callipers are often more expensive to replace, increasing the car's value.

- Wheels and Tyres: Non-standard or more expensive wheels (e.g., lightweight alloys) and performance tyres increase value and can be attractive to thieves.

- Bodywork Changes: This covers a wide range, including flared arches, spoilers, valances, bumpers, aftermarket headlights and taillights, carbon fibre parts, and full body kits. These alter the car's appearance and can increase repair costs.

- Paintwork and Aesthetics: Custom paint jobs, vinyl wraps, large decals, stickers, and window tints all deviate from the factory finish and must be declared. Even minor decorative changes can impact premiums.

- Interior Upgrades: Aftermarket seats (especially racing buckets), steering wheels, pedals, enhanced sound systems, and roll cages also count.

It's important to note that the percentage increase will vary significantly between insurers and the specific modification. For instance, while an air filter might push premiums up by 25%, a more significant modification like an aftermarket turbo kit could see a staggering 132% increase with a standard insurer.

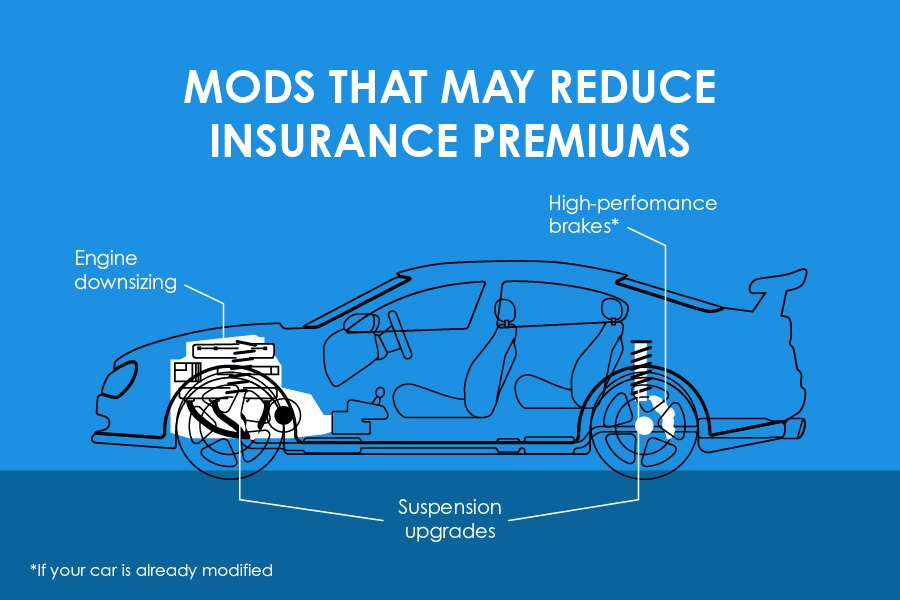

While most modifications lead to higher costs, some can actually be beneficial for your premiums, or at least not increase them. These are typically related to enhancing security or safety:

- Dash Cams: Footage from a dash cam can be invaluable in proving fault in an accident, potentially turning a split liability claim into a no-fault claim. Insurers appreciate this as it can reduce their payouts.

- Enhanced Security Features:

- Steering Wheel Locks: A visible deterrent that makes it harder for thieves to drive off with your car.

- Catalytic Converter Cages (Catlocs): With catalytic converter theft on the rise, these cages make it significantly harder for thieves to steal this valuable component.

- Upgraded Alarms and Immobilisers: If your car doesn't have a modern alarm system or immobiliser as standard, adding one can make it less attractive to thieves.

- Tracking Devices: GPS trackers can dramatically increase the chances of recovering a stolen vehicle, saving insurers the cost of replacement.

- Parking Sensors: These can help prevent minor parking prangs, which account for a significant percentage of insurance claims. While often standard on newer cars, fitting them to an older vehicle could show a reduction in risk.

- Advanced Driver Assistance Systems (ADAS): Systems like pedestrian detection, adaptive cruise control, lane departure correction, and automatic emergency braking are designed to prevent accidents. However, this is a nuanced area. While they enhance safety, these systems are often complex and expensive to repair if damaged, which can offset any premium saving. Always check with your insurer before fitting or relying on ADAS for a premium reduction.

Even with these potentially beneficial modifications, the golden rule still applies: inform your insurer. They may have specific requirements, such as needing security devices to be Thatcham approved, for them to acknowledge the benefit.

Comparative Table: Impact of Common Modifications

| Modification Type | Typical Impact on Premium | Reasoning |

|---|---|---|

| Engine Remap / Tuning Box | Significant Increase | Increased performance, higher accident risk. |

| Aftermarket Exhaust System | Moderate Increase | Potential performance boost, increased noise, aesthetic change. |

| Body Kit / Spoilers | Moderate Increase | Increased vehicle value, higher repair costs, potential theft risk. |

| Alloy Wheels (non-standard) | Moderate Increase | Increased vehicle value, higher theft risk, more expensive to replace. |

| Custom Paint / Wrap | Minor to Moderate Increase | Increased vehicle value, higher repair costs if damaged. |

| Window Tints | Minor Increase | Can affect visibility, aesthetic change. |

| Dash Cam | Potential Decrease / No Change | Provides evidence for claims, potentially reducing insurer payouts. |

| Tracking Device | Potential Decrease | Significantly improves vehicle recovery rate, reducing theft payouts. |

| Upgraded Alarm/Immobiliser | Potential Decrease | Reduces theft risk, making the car less appealing to criminals. |

| Parking Sensors | Potential Decrease / No Change | Reduces risk of low-speed parking accidents. |

The Pitfalls of Undisclosed Modifications

The consequences of not declaring modifications are severe and far-reaching. As mentioned, your policy could be invalidated. This means:

- Claim Rejection: If you're involved in an accident, your insurer can refuse to pay out, leaving you personally liable for all damages, including your own vehicle's repairs, third-party vehicle damage, and any personal injury claims.

- Driving Uninsured: Driving without valid insurance is a serious offence in the UK. It can lead to points on your licence, a significant fine, and even vehicle seizure. This will also make it much harder and more expensive to get insurance in the future.

- Policy Cancellation: Your insurer may cancel your policy, making it difficult to obtain insurance from other providers, as you'll have to declare the cancellation.

It's simply not worth gambling with your insurance. The small saving you might make by not declaring a modification pales in comparison to the financial ruin and legal penalties you could face.

Seeking Specialist Modified Car Insurance

For those with significantly modified vehicles, or if you plan on undertaking extensive customisation, a standard insurance policy might not be the best fit. Mainstream insurers may quote astronomical prices or even refuse to cover heavily modified cars due to their perceived higher risk and complexity.

This is where specialist modified car insurers come in. These companies understand the intricacies of aftermarket parts and the passion behind car customisation. They are often better equipped to:

- Offer more competitive premiums for modified vehicles.

- Accurately value your modifications, ensuring they are properly covered in the event of a claim.

- Provide tailored policies that consider specific types of modifications, such as track-day cover or agreed value policies.

- Have staff who are knowledgeable about various car scenes and modifications.

If your modifications go beyond simple bolt-ons, contacting two or three specialist insurers is highly recommended. They can often provide a more realistic and affordable quote, along with the peace of mind that your unique vehicle and its valuable modifications are adequately protected.

Frequently Asked Questions (FAQs)

Do I need to declare stickers or decals?

Yes, even seemingly minor aesthetic changes like large stickers, decals, or a different paint finish (even if it's the same colour, but not factory standard) should be declared. They change the car's appearance and could affect repair costs or theft risk.

What if I buy a car that's already modified?

If you purchase a car that has already been modified, you are responsible for declaring these modifications to your insurer when you take out your policy. Ensure you get a full list of all aftermarket parts from the previous owner and disclose everything. Failure to do so carries the same risks as modifying the car yourself and not declaring it.

How do I declare a modification to my insurer?

The best way is to call your insurance provider directly. Be prepared to provide specific details about the modification, including its type, cost, and how it might affect the car's performance or value. Some insurers may allow you to declare minor changes online, but a phone call ensures clarity.

Not always. While most performance and aesthetic modifications tend to increase premiums, security and some safety modifications (like tracking devices or dash cams) can sometimes lead to a reduction or no change in your premium. However, the vast majority of modifications will result in an increase.

What happens if I don't declare a modification and my insurer finds out?

If your insurer discovers undeclared modifications, they can void your policy, refuse to pay out on claims, and may even prosecute you for driving without valid insurance. This can lead to fines, points on your licence, and a significant struggle to obtain insurance in the future. It's a risk that is never worth taking.

Conclusion

Modifying your car can be a deeply rewarding experience, allowing you to tailor your vehicle to your exact preferences. However, it's a journey that demands careful consideration of the insurance implications. The relationship between car modifications and insurance is complex, driven by factors such as increased value, altered risk profiles, and potential theft appeal. The overarching message is clear: transparency with your insurance provider is paramount.

By understanding what constitutes a modification, knowing which changes are likely to affect your premiums (both positively and negatively), and always adhering to the golden rule of declaring every alteration, you can enjoy your customised ride with complete peace of mind. For those embarking on significant modifications, exploring specialist modified car insurance options can provide tailored coverage and often better value, ensuring your pride and joy is fully protected on the UK's roads.

If you want to read more articles similar to Car Mods & Insurance: Your UK Guide, you can visit the Automotive category.