10/10/2013

It's a fact of life that sometimes, things don't quite go to plan. When it comes to banking and building societies, this can manifest in various ways, from unexpected charges to unsatisfactory customer service. Fortunately, you have avenues available to address these issues. This guide will walk you through the essential steps for lodging a complaint about your bank or building society, from understanding your rights to escalating your concerns if you're not satisfied with the initial resolution. We'll cover what to expect, how to effectively communicate your grievance, and the crucial role of the Financial Ombudsman Service (FOS).

- Your Rights When Dealing with Banks

- Understanding Discrimination in Banking

- What to Do When Things Go Wrong

- The Bank's Complaints Process

- Tips for Making an Effective Complaint

- Escalating to the Financial Ombudsman Service (FOS)

- Using Claims Management Companies

- Considering Legal Action

- Switching Banks: An Alternative Solution

- Further Assistance and Information

Your Rights When Dealing with Banks

Beyond the specific terms and conditions of your account, UK law mandates certain standards of service from your bank or building society. They are legally obliged to provide their services with:

- Reasonable care and skill: This means they must operate responsibly, maintain accurate financial records, and act with a degree of professionalism. For example, they should process your transactions accurately and protect your account information diligently.

- Timely execution: If a specific timeframe for a service isn't agreed upon, it must be completed within a reasonable period. What's considered reasonable can vary; for instance, a decision on a loan application should typically be provided within a few working days.

- Agreed price: If a price for a service has been set, that's what you should be charged. If no definite price was agreed, the charge must be fair and reasonable.

Failure to meet these standards can provide grounds for a complaint, potentially to the Financial Ombudsman Service.

Understanding Discrimination in Banking

It is against the law for any bank or building society to discriminate against you based on protected characteristics such as race, sex, disability, religion, or sexuality. If you believe you have been treated unfairly due to any of these reasons, you may have recourse through the Financial Ombudsman Service. In some cases, legal action might also be an option, though this would necessitate seeking professional legal advice.

It's important to note that there are specific, lawful circumstances where differentiation might occur. For example, certain accounts might have age restrictions. However, any discrimination outside of these legally defined exceptions should be challenged.

What to Do When Things Go Wrong

Before lodging a formal complaint, it's crucial to ascertain that the problem genuinely stems from the bank's actions or omissions. For instance, if you share your bank card and PIN with someone and they misuse it, the bank is generally not liable. Many minor issues can be resolved swiftly through direct communication.

If a problem cannot be resolved informally, or if you are dissatisfied with the service received, you should initiate the bank's formal complaints procedure. This is a structured process designed to address customer grievances.

The Bank's Complaints Process

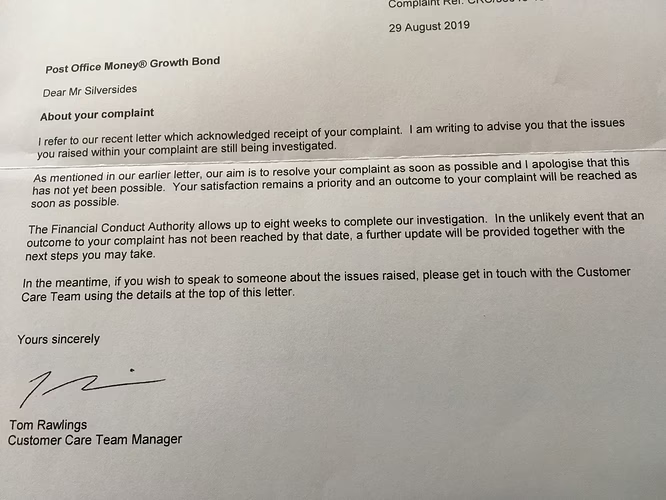

All banks and building societies are legally required to have a documented complaints procedure. This document outlines how customers can make a complaint and should be readily available in branches or on the institution's website. If you cannot locate this information, you are entitled to request a copy from the bank.

It is vital to follow the steps outlined in their procedure. The bank must investigate your complaint thoroughly and provide you with a clear response, typically within eight weeks. This response could be:

- An initial response: This often provides an opportunity for you to respond if you remain unsatisfied.

- A final response: This represents the bank's definitive decision on your complaint.

- A holding response: If the investigation is ongoing and they cannot provide a final answer within eight weeks, they may send a response indicating this. This response should also inform you of your right to escalate the complaint to the Financial Ombudsman Service. At this point, you can choose to allow the bank more time or immediately refer the matter to the FOS.

If the bank fails to respond within the eight-week timeframe, or if you are unhappy with their final response, you can then escalate your complaint to the Financial Ombudsman Service.

Tips for Making an Effective Complaint

Whether you complain in person, over the phone, or in writing, adopting a strategic approach can significantly improve the chances of a positive outcome. Here are some key tips:

1. Act Promptly

Contact the bank or building society as soon as you identify the problem. This gives them the earliest opportunity to rectify the situation and ensures you don't miss any crucial time limits for escalation.

2. Keep Records

Maintain a detailed record of all your interactions. This includes the date and time you contacted them, the name of the person you spoke to, and a summary of the conversation. This documentation is invaluable if you need to take your complaint further.

3. Gather Evidence

Collect all relevant documentation that supports your complaint. This might include bank statements, cheque stubs, correspondence (emails, letters), and any other paperwork that substantiates your claim.

4. In-Person Complaints

If you visit a branch, ask to speak to the person responsible for your account or the branch manager. Request a copy of any documents you hand over, and make notes of who you spoke with and what was discussed. Follow up with a written summary if possible to create a clear paper trail.

5. Written Complaints

Clearly mark your letter or email with the word 'Complaint' at the top. This helps ensure it is directed to the appropriate department. Send copies of your supporting documents, never the originals. Clearly explain the issue, including all relevant facts, dates, and names. Be calm but firm in your tone.

6. State Your Desired Outcome

Clearly articulate what you expect the bank to do to resolve the issue. This could include a refund, an apology, or compensation for any losses incurred. Be specific about any compensation you are seeking.

7. Proof of Postage

Consider sending important letters via recorded delivery. This provides proof that your complaint was received by the bank.

Escalating to the Financial Ombudsman Service (FOS)

If your bank or building society fails to resolve your complaint satisfactorily, or if they exceed the eight-week response period, you have the right to refer your case to the Financial Ombudsman Service (FOS). The FOS is an independent body set up to resolve disputes between consumers and financial services firms.

Key Rules for FOS Complaints:

- You must have first attempted to resolve the issue directly with your bank or building society through their complaints procedure.

- The firm has up to eight weeks to provide a final response.

- You must submit your complaint to the FOS within six months of receiving the bank's final response, or within six months of the eight-week period expiring if no response was received.

The FOS can investigate a wide range of issues, from unfair charges to mis-selling of financial products.

Using Claims Management Companies

You may encounter firms, often called claims management companies or claims assessors, who offer to handle your complaint to the Ombudsman for a fee. It's important to understand that you do not need to pay for this service. The Financial Ombudsman Service itself provides a free helpline and assistance with their process.

If you do decide to use a claims management company, meticulously review their terms and conditions, paying close attention to the fees involved. It is advisable to take the agreement away to read and seek independent advice before committing.

In England and Wales, these companies must be authorised by the Financial Conduct Authority (FCA). You can verify their authorisation on the FCA's website. If you are dissatisfied with the service provided by a claims management company, you can lodge a complaint with the Claims Management Ombudsman, which offers a free and independent dispute resolution service.

Considering Legal Action

Taking a bank or building society to court should be considered a last resort, typically only pursued if the Financial Ombudsman Service cannot resolve your complaint. Before embarking on legal action, carefully assess the strength of your evidence and the financial standing of the institution. Pursuing a company with no assets is generally unproductive.

Legal action against financial institutions is rare, and it is highly recommended to seek expert legal advice before proceeding. Crucially, if you choose to take a matter to court before complaining to the Ombudsman, you will forfeit your right to involve the FOS at a later stage.

Switching Banks: An Alternative Solution

If your dissatisfaction stems from ongoing poor service or a mismatch between your needs and the bank's offerings, you might consider switching to a different provider. Thoroughly research the services and facilities offered by other banks and building societies to ensure they better meet your requirements before making the move.

Further Assistance and Information

For comprehensive guidance on banking products and financial matters, consult the resources available from:

- The Money Advice Service: Their website offers a wealth of information on various financial products and services.

- The Financial Ombudsman Service (FOS): If your bank's internal complaints process has not yielded a satisfactory outcome, the FOS is the next step. You can contact their consumer helpline on 0800 023 4567 or 0300 123 9 123 for assistance and to initiate a complaint.

By understanding your rights and following the correct procedures, you can effectively address any issues you encounter with your bank or building society.

If you want to read more articles similar to Complaining About Your Bank, you can visit the Automotive category.