21/09/2004

Discovering your car has been declared a 'write-off' after an accident can be a stressful experience. While your insurer typically arranges for repairs, sometimes the cost of fixing the damage outweighs the car's value, leading to it being classified as a total loss. This article will guide you through the intricacies of car write-offs, from understanding the categories to your responsibilities and how it impacts your insurance.

- What Exactly is a Car Write-Off?

- How Insurers Determine a Write-Off

- Understanding Write-Off Categories

- What Happens When Your Car is Written Off?

- Determining Your Car's Market Value

- Impact on Your Car Insurance

- Can You Keep Your Written-Off Car?

- Insuring a Cat S Car

- Buying a Cat S or Cat N Car: Safety and Considerations

- Selling a Cat S Car

- Car Finance and Write-Offs

- Your Obligation to Inform the DVLA

- Frequently Asked Questions

What Exactly is a Car Write-Off?

A car is typically deemed a write-off, or 'total loss' by insurers, in two main scenarios: when the damage renders it unsafe or unroadworthy, or when the estimated repair costs exceed a significant percentage of the vehicle's current market value. It's important to note that even relatively minor damage can result in a write-off if the car is of low value. The decision is purely based on economic viability for the insurer.

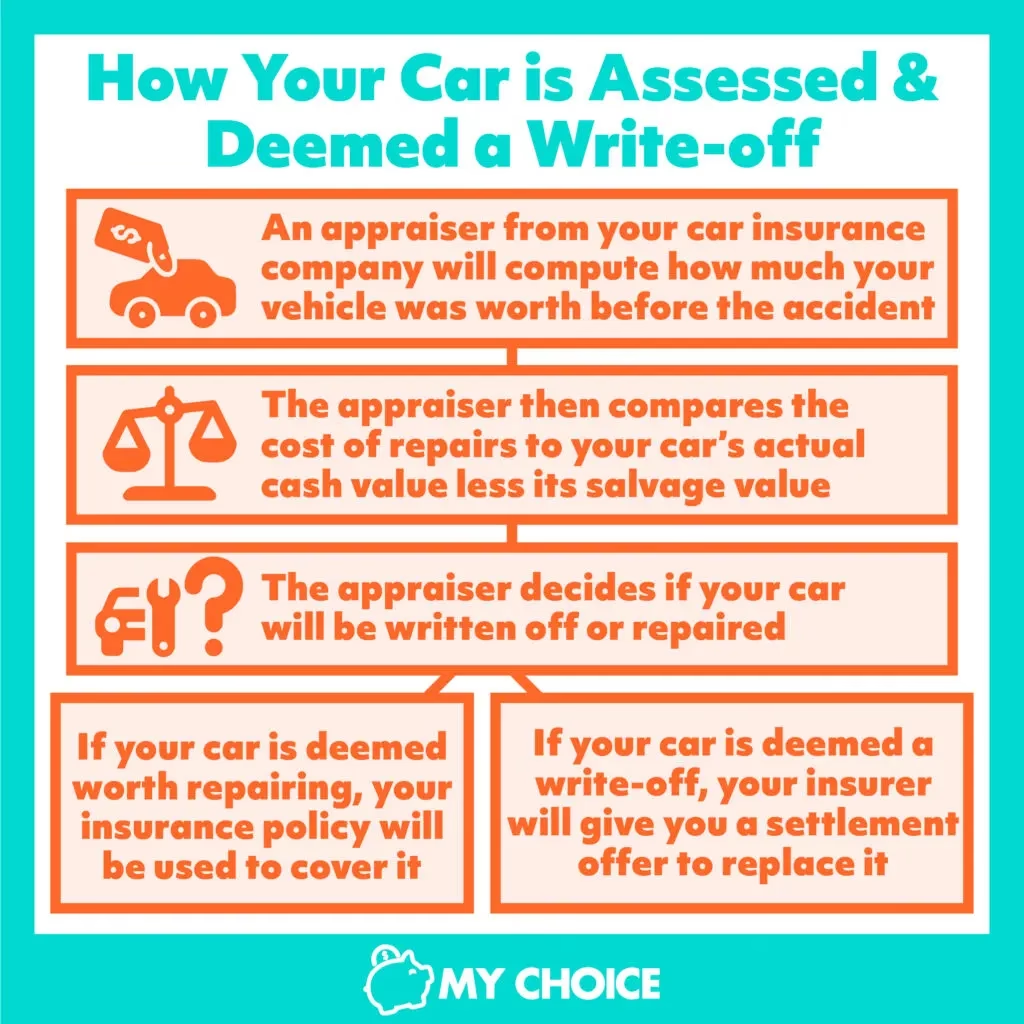

How Insurers Determine a Write-Off

When you file a claim, your insurance company will assess the extent of the damage. They will obtain repair quotes and compare these to the car's pre-accident market value. If the repair bill is higher than, say, 70-80% of the car's value, it's often more economical for the insurer to declare it a write-off. Each insurer may have slightly different thresholds, but the core principle remains the same: is it financially sensible to repair the car?

Understanding Write-Off Categories

Not all write-offs are created equal. The categories indicate the severity of the damage and the car's potential to be returned to the road. Here's a breakdown:

| Category | Definition |

|---|---|

| Cat A | The vehicle is beyond economic repair and cannot be used on the road again. It must be crushed, and no parts can be salvaged. |

| Cat B | The vehicle is also beyond economic repair, but certain parts may be salvaged. The main body shell must still be crushed. |

| Cat S | The car has suffered structural damage, affecting the chassis or frame. It can be repaired, but requires significant work and must be re-registered with the DVLA. Previously known as Cat C. |

| Cat N | The car has suffered non-structural damage and can be repaired. This might include damage to lights, seats, or minor bodywork. Previously known as Cat D. It can be bought back and repaired to be roadworthy. |

What Happens When Your Car is Written Off?

If your car is declared a write-off, several things will happen:

- Policy Cancellation: Your current insurance policy will typically be cancelled. This means you'll lose any entitlement to a courtesy car or the 'driving other cars' extension on your policy.

- Insurer Takes Ownership: The insurer will usually take ownership of the written-off vehicle.

- Settlement Payment: You will receive a settlement amount. This is generally the car's market value before the accident, minus your policy's excess. For example, if your car was worth £5,000 and your excess is £250, you would receive £4,750.

If you accept the settlement and do not wish to buy the car back, you'll need to send your V5C logbook to your insurer and retain the section for 'sell, transfer part-exchange your vehicle to the motor trade'. Crucially, you must also inform the DVLA that your car has been written off.

Determining Your Car's Market Value

Understanding your car's pre-accident market value is key. You can get an estimate by using online car valuation tools. Simply enter your car's registration number and select the 'selling' option. These tools can give you an idea of what you might expect if you were to sell your car privately or part-exchange it at a dealership.

Impact on Your Car Insurance

When your car is written off, your existing insurance policy is cancelled. Depending on who was at fault for the accident, you might also lose some or all of your no-claims bonus. Expect your future car insurance premiums to increase, as your claims history is a significant factor insurers consider. Even if the car wasn't a write-off, being involved in an accident will likely lead to higher insurance costs.

Can You Keep Your Written-Off Car?

The ability to keep your written-off car depends on its category:

- Cat A: These cars cannot be returned to the road by law and cannot be bought back from the insurer.

- Cat B: While the body shell must be crushed, you can technically buy it back to salvage parts. However, this is often only practical for those involved in the motor trade.

- Cat S and Cat N: You can usually buy these cars back from your insurer. However, the responsibility for disposal and repair falls on you. These cars will have lost significant value.

If you wish to buy back a Cat S or Cat N write-off, inform your insurer immediately. Insurers often work with salvage companies, and delays could mean you miss the opportunity. Before committing, it's highly advisable to get an independent mechanic to inspect the car and provide an estimate for repair costs. This will help you decide if buying it back is a sensible financial decision. If you do buy it back, your insurer will pay you the settlement amount minus the car's salvage value.

Insuring a Cat S Car

Insuring a Cat S vehicle is possible, but insurers typically classify them as high-risk. This is due to the significant accident and structural damage it has sustained. Furthermore, accurately determining the market value and condition of a previously written-off car can be challenging for insurers, leading to higher premiums. Some insurers may even refuse to cover Cat S vehicles altogether, so it's crucial to shop around and be upfront with potential insurers.

Buying a Cat S or Cat N Car: Safety and Considerations

When considering buying a previously written-off vehicle, proceed with caution. Dealers are legally obliged to disclose a car's Cat S or Cat N status. While they might seem like a bargain, thorough inspection is essential.

- Cat N: This category signifies non-structural damage. It could range from a damaged door panel to flood damage or issues with steering or brakes. A HPI check is recommended to understand the exact reason for the write-off, and professional inspection is vital to ensure repairs have been carried out safely and correctly.

- Cat S: Structural damage means these cars require professional repair equipment. While there's no legal requirement for post-repair inspection before returning to the road, it's strongly advised to ensure the vehicle's integrity.

Selling a Cat S Car

Selling a Cat S car is legal, provided you clearly declare its status. Buyers may request a third-party inspection to verify the quality of repairs, which could impact your selling price. Alternatively, you can sell it to salvage buyers who are primarily interested in the car's parts.

Car Finance and Write-Offs

If your car is on finance and declared a write-off, the situation can be complex. The settlement amount from your insurer might be less than the outstanding finance balance. This means you could still be liable for loan payments even without the car, or your lender might demand the full outstanding amount. Your options include:

- Negotiating a higher settlement with your insurer by providing evidence of your car's true market value.

- Contacting your finance lender to discuss arrangements for the outstanding debt.

- Utilising gap insurance, a separate policy designed to cover the difference between your car's market value and the amount you originally paid, which can help offset any shortfall in your finance agreement.

Your Obligation to Inform the DVLA

It is a legal requirement to inform the DVLA if your car is written off. You can do this via the GOV.UK website. You'll need your insurance company's details, your car's registration number, and the relevant reference number from your V5C logbook. Failure to notify the DVLA can result in a £1,000 fine. If you keep a Cat S or Cat C write-off, you must also re-apply to the DVLA to re-register it.

Frequently Asked Questions

Q: Do I have to tell my insurance company if my car is written off?

Yes, if your car is written off, your insurer will handle the process. You need to cooperate with them and provide necessary documentation like your V5C logbook.

Q: Can I get a new car insurance policy for a written-off car?

Yes, you can insure a Cat S or Cat N car, but expect higher premiums and potentially fewer insurer options.

Q: What is the difference between Cat S and Cat N?

Cat S indicates structural damage requiring significant repairs, while Cat N signifies non-structural damage, making it generally easier and cheaper to repair.

Q: Will my insurance premium increase after a write-off?

Yes, generally, your insurance premiums will increase after an accident, especially if it results in a write-off, due to the increased risk profile.

Q: What is gap insurance?

Gap insurance covers the difference between your car's market value and the outstanding amount on your finance agreement if it's written off.

If you want to read more articles similar to Your Car's Write-Off: What You Need to Know, you can visit the Cars category.