09/02/2018

Understanding Insurance Key Performance Indicators (KPIs)

In the complex and dynamic world of insurance, success hinges on meticulous monitoring and strategic decision-making. Key Performance Indicators (KPIs) serve as the compass and map for insurance companies, providing crucial insights into their operational efficiency, financial health, and overall market standing. These quantifiable measures are not merely numbers; they are the vital signs of a business, highlighting areas of strength and pinpointing opportunities for improvement. By effectively tracking and analysing a range of insurance KPIs, companies can navigate the intricacies of the industry, optimise performance, and ensure sustainable growth.

The insurance landscape is vast, encompassing sales, claims management, underwriting, finance, and customer service. Each of these facets presents unique challenges and opportunities, and a comprehensive understanding of performance requires a tailored approach to measurement. This article will delve into the essential insurance KPIs across key departments, offering a clear breakdown of what they are, why they matter, and how they can be effectively implemented. We will also explore the importance of robust reporting solutions, such as BI dashboards, in transforming raw data into actionable intelligence.

Sales KPIs: Driving Revenue and Growth

The sales department is the engine room of any insurance company, responsible for generating revenue and expanding the customer base. Effective sales KPIs are critical for evaluating the performance of sales teams, identifying top talent, and refining sales strategies. Here are some fundamental sales KPIs that every insurance company should monitor:

- Quote Rate: This is a foundational metric that measures the number of quotes a sales representative provides against the number of leads they have contacted. It offers a direct insight into the activity levels and outreach effectiveness of the sales team.

- Quota Rate: A step beyond the quote rate, the quota rate assesses how well sales staff are meeting their established sales targets. It is crucial for management to set realistic quotas to maintain motivation and prevent demoralisation. This KPI helps in understanding the attainability of sales goals and identifying potential training needs.

- Contract Rate: This metric focuses on the conversion of leads into actual policyholders. It measures the percentage of contacted leads that result in a binding contract, indicating the sales team's ability to close deals effectively.

- Number of Referrals: Gauging the number of new clients acquired through referrals from existing clients is a powerful indicator of customer satisfaction and organic growth. It reflects client loyalty and the company's ability to generate positive word-of-mouth marketing.

- Bind Rate: The bind rate quantifies the success of converting quotes into finalised, legally binding policies. A high bind rate signifies a skilled sales team capable of overcoming objections and effectively communicating the value proposition.

- Percentage Pending: This KPI tracks the proportion of policies that are awaiting approval at any given time. A high percentage pending can signal a bottleneck in the workflow, potentially impacting efficiency and client satisfaction.

- Sales Growth Rate: This overarching metric measures the increase or decrease in sales over a specific period. It is most insightful when broken down into new policies and policy renewals, providing a clearer picture of overall business momentum.

- New Policies per Agent: Identifying individual agent performance is vital for recognising top performers and fostering healthy competition. This metric highlights which agents are most effective at acquiring new business.

- Retention Rate: Acquiring new customers is often more expensive than retaining existing ones. The retention rate measures the percentage of policies that are renewed, underscoring the company's ability to maintain client relationships and deliver ongoing value.

- Policies In-Force per Agent: This metric provides an aggregate view of policy distribution across the sales force. When analysed alongside retention and growth rates, it can help pinpoint inefficiencies in sales management or agent support.

By focusing on these sales KPIs, insurance companies can cultivate a high-performing sales culture, drive revenue, and achieve sustainable growth.

Claims KPIs: Ensuring Efficiency and Customer Satisfaction

The claims department is at the forefront of customer interaction, particularly during times of need. Efficient and fair claims processing is paramount to maintaining customer trust and loyalty. The following KPIs are essential for monitoring the effectiveness of the claims handling process:

- Average Cost Per Claim: This metric provides the average financial outlay for each claim processed. It is crucial for pricing strategies, financial forecasting, and identifying potential areas for cost reduction. Analysing this by claim type or policy segment can offer deeper insights.

- Claim Frequency: This KPI measures the likelihood of a loss occurring based on the number of outstanding policies. It is instrumental in managing cash flow, assessing risk exposure, and setting appropriate premiums.

- Components of Claim Costs (CCC): This metric breaks down the various costs associated with settling a claim, including legal fees, administrative expenses, and settlement time. Analysing CCC helps identify inefficiencies within the claims process and target areas for cost optimisation.

- Average Time to Settle a Claim: The speed at which claims are settled significantly impacts customer satisfaction and retention. While complexity can influence settlement time, a consistent effort to minimise this duration is vital. This KPI can be segmented by policy type to understand variations.

- Client Satisfaction: While often measured through surveys, client satisfaction is perhaps best reflected in retention and renewal rates. High satisfaction leads to repeat business and positive referrals, acting as a crucial indicator of overall service quality.

- Problem Resolution Rate: This KPI assesses the efficiency with which customer issues are resolved. Prolonged problem resolution can escalate costs and damage customer relationships.

- Calls Handled within 24 Hours: Measuring the proportion of incoming calls addressed within a 24-hour window indicates the responsiveness and capacity of the claims resolution team. This should be considered alongside the total volume of calls received.

- Underwriting Cycle Time: This metric tracks the duration it takes for the underwriting department to process policy applications. Delays in underwriting can lead to lost business and decreased client satisfaction, highlighting the need for streamlined processes.

- Claims Ratio: Calculated by dividing the total claims paid by the total earned premiums, the claims ratio offers a high-level view of profitability and risk. Anomalies in this ratio can signal potential issues like increased fraud or difficulties in the claims submission process.

By diligently tracking these claims KPIs, insurance companies can enhance their claims handling efficiency, improve customer experience, and mitigate financial risks.

Financial KPIs: Ensuring Profitability and Stability

The financial health of an insurance company is the bedrock upon which its sustainability rests. Financial KPIs provide a clear view of profitability, efficiency, and overall financial stability. Key financial metrics for the insurance industry include:

- Expense Ratio: This KPI measures the total expenses incurred by the company relative to the premiums it generates. It helps assess operational efficiency and identify whether premiums are adequately priced or if cost-saving measures are needed.

- Average Policy Size: By dividing total collected premiums by the number of policies issued, this metric provides insight into the average revenue generated per policy. It also aids in understanding the company's risk profile, as larger policies can carry greater risk.

- Loss Ratio: The loss ratio, calculated by dividing total claims payouts by total premium revenue, is a critical indicator of underwriting profitability. A high loss ratio might suggest that premiums are set too low, while a low ratio could indicate issues with claims processing or reporting.

- Average Revenue Per Client: This metric helps determine the profitability of acquiring and serving individual clients, informing decisions about customer acquisition costs.

- Cost Per Quote: This KPI quantifies the expenses associated with generating a quote for a potential client. Understanding this cost is crucial for optimising sales processes and ensuring that quoting activities are financially viable.

- Cost Per Bind: This metric measures the incremental cost of securing a new policy, essentially representing the price of acquiring a new customer.

- Cost Per Bind by Vertical: Building on the cost per bind, this KPI segments acquisition costs by product line or industry vertical. This allows companies to identify which verticals are most profitable and which may require strategic adjustments.

- Net Profit Margin: This fundamental metric measures the overall profitability of the company by dividing net income by total revenue. A healthy net profit margin, often considered to be above 10%, is a strong indicator of financial success.

- Administrative Costs Per Policy: A more granular view of expenses, this KPI scrutinises the administrative costs associated with managing each policy. It helps pinpoint inefficiencies in administrative processes that can impact policy profitability.

Monitoring these financial KPIs is essential for sound financial management, ensuring the long-term viability and profitability of the insurance business.

Developing and Implementing Effective Insurance KPIs

Creating impactful insurance KPIs requires a strategic and thoughtful approach. Simply adopting generic metrics may not align with the unique objectives and operational structure of a specific company. To develop truly effective KPIs, consider the following principles:

- Define Clear, Measurable Goals: Every KPI must be tied to a specific, quantifiable objective. Vague or subjective goals will not yield actionable insights.

- Adopt a Holistic View: Consider how a KPI might impact other business units or the company as a whole. KPIs should ideally contribute to the overall strategic direction of the organisation.

- Align with Company Processes: Integrate new KPIs into existing company processes to minimise resource strain and maximise efficiency. This also helps in identifying and rectifying inefficient workflows.

- Foster a Supportive Company Culture: Create an environment where KPIs are understood, embraced, and seen as tools for improvement rather than mere metrics for judgment. Positive reinforcement and recognition can significantly boost engagement.

- Prioritise Data Compilation and Reporting: The value of a KPI lies in its ability to be tracked and interpreted. Investing in robust reporting solutions, such as KPI dashboards, is crucial for streamlining data analysis and making informed decisions.

- Make Informed Decisions: Ultimately, the purpose of KPIs is to provide the data necessary for making sound business decisions that drive performance and mitigate risks.

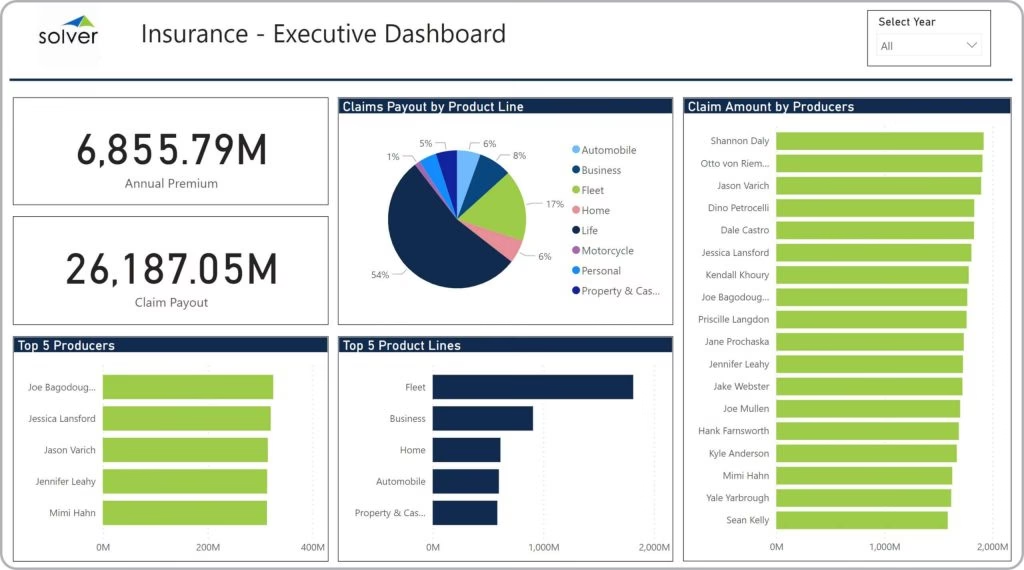

The Power of Insurance KPI Dashboards

Managing and analysing the vast amount of data associated with insurance KPIs can be a daunting task. This is where Business Intelligence (BI) dashboard solutions become invaluable. An insurance KPI dashboard offers a centralised, visual, and interactive platform for monitoring key metrics in real-time.

The benefits of using a BI dashboard for insurance KPIs are numerous:

- Automated Data Collection: BI software can interface with existing ERP and other systems to automatically extract and consolidate data, eliminating manual data entry and reducing errors.

- Centralised Data Repository: All critical data is stored in a single, accessible location, saving time and improving collaboration among teams.

- Prebuilt KPI Templates: Many BI solutions offer pre-designed KPI templates tailored for the insurance industry, allowing for rapid implementation and customisation.

- Real-time Reporting: Dashboards provide instant updates, enabling quick responses to changing market conditions or internal performance trends.

- Enhanced Visibility: They offer a consolidated view of premiums, claims, sales, and financial performance, providing a comprehensive overview of business health.

- Risk Mitigation and Fraud Detection: By visualising patterns and anomalies in data, dashboards can help identify potential risks and instances of insurance fraud.

- Forecasting and Scenario Planning: Historical data presented on dashboards can be used to forecast future scenarios and plan accordingly.

Choosing the Right BI Tool

Selecting the appropriate BI tool is crucial for maximising the effectiveness of your insurance KPI dashboard. Factors to consider include hosting preferences, budget, target audience, and primary use cases. Popular options include:

- Trevor.io: A no-code solution praised for its ease of use, allowing for the creation of interactive dashboards with drag-and-drop functionality. It offers unlimited users and ad-hoc queries.

- Apache Superset: An open-source BI tool suitable for tech-savvy users who require extensive customisation through SQL scripting. However, it has a steeper learning curve and lacks dedicated customer support.

- Geckoboard: Known for its visually appealing interface and white-labelling capabilities, making it ideal for sharing metrics with external stakeholders like brokers. Its multi-device adaptability is also a significant advantage.

By leveraging a suitable BI dashboard solution, insurance companies can transform their KPI management, driving efficiency, profitability, and informed decision-making.

Frequently Asked Questions

What is a KPI dashboard?

A KPI dashboard is a visual, interactive display of key business data and performance metrics. It provides users with up-to-date information, enabling them to make informed decisions without needing to constantly request data from technical teams.

What are KPIs for insurance?

Insurance KPIs are critical metrics used by insurance companies to assess their performance across various business functions. Common examples include average time to settle claims, average cost per claim, new and renewed gross written premiums, return on equity (ROE), and average policy size.

What does ROE mean in insurance?

ROE, or Return on Equity, is a financial metric used to evaluate an insurance company's profitability in relation to its shareholders' equity. It measures how effectively the company generates profits for its stockholders. An ROE of around 10% is generally considered standard for insurance companies.

How do I create a KPI dashboard in Excel?

While it's possible to create a KPI dashboard in Excel, it often requires advanced product expertise to make it truly interactive and dynamic. Manual data updates are typically necessary, which can be time-consuming and prone to errors. For more robust and scalable solutions, using a dedicated no-code BI tool like Trevor.io is often recommended for its ease of use and automated capabilities.

If you want to read more articles similar to Insurance KPIs: Measure Your Success, you can visit the Automotive category.