06/12/2013

Experiencing a car write-off can be a daunting and often confusing ordeal. One moment you're driving along, the next your vehicle is deemed a 'total loss' by your insurer. But what exactly does this mean for you and your car? Can you keep it? Should you? This comprehensive guide will demystify the process of a car being written off in the UK, helping you understand your options and make the best decision for your circumstances.

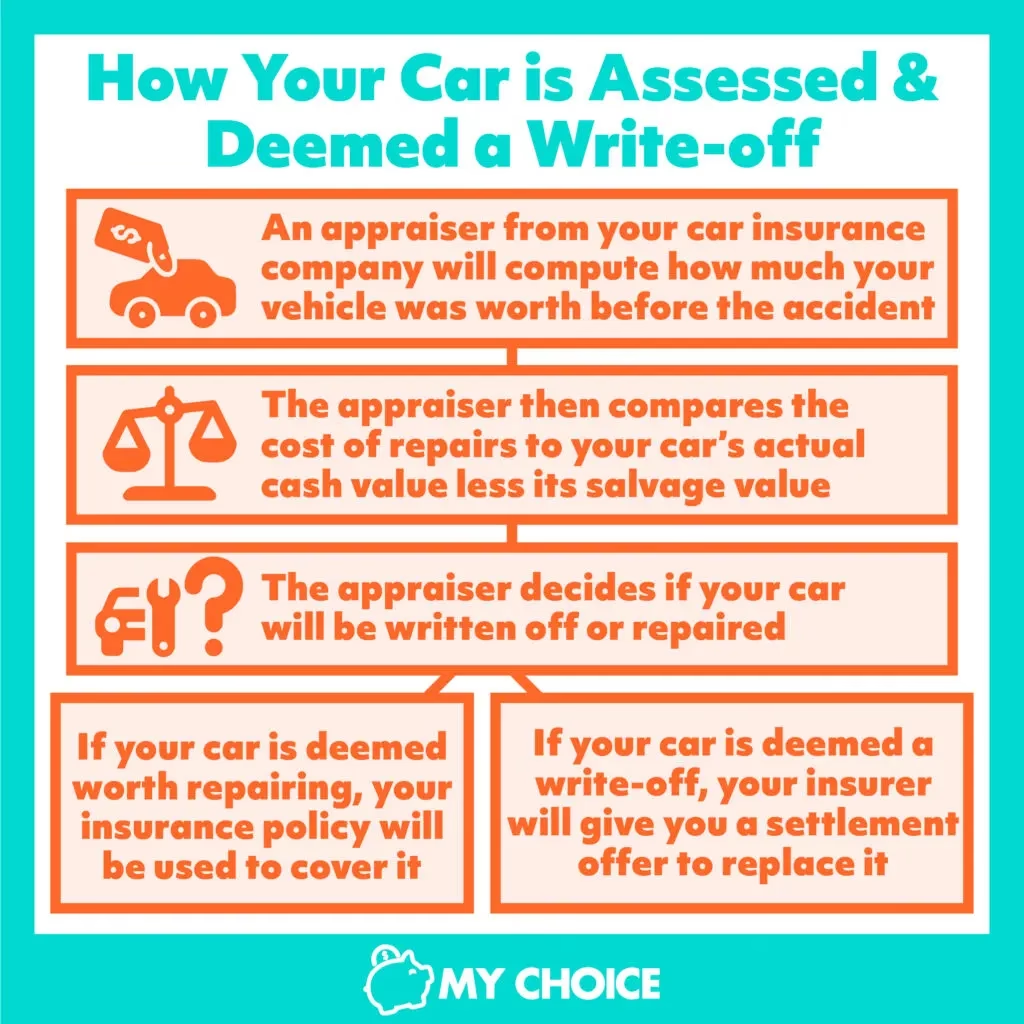

When your car is involved in an incident and suffers significant damage, your insurance company will assess the cost of repairs against the vehicle's market value. If the repair costs, plus other associated expenses like courtesy cars and storage, exceed a certain percentage of the car's value (typically around 60-70%, though this varies by insurer), it's declared an 'economical write-off'. This means it's cheaper for the insurer to pay you the car's value than to repair it. However, a 'write-off' doesn't always mean your car is destined for the scrap heap; it very much depends on the category assigned to the damage.

Understanding UK Car Write-Off Categories

In the UK, the Association of British Insurers (ABI) categorises written-off vehicles based on the extent and nature of the damage, and whether they can safely return to the road. It's crucial to understand these categories as they dictate whether you can keep your vehicle and what steps you'll need to take.

Category A: Scrap Only

Category A signifies the most severe damage. These vehicles are deemed beyond repair and are an immediate safety risk. They must be crushed entirely, with no parts salvaged for re-use, not even for spares. If your car falls into Category A, you absolutely cannot keep it, and your insurer will arrange for its complete destruction.

Category B: Break for Parts

Vehicles in Category B are also severely damaged and considered unsafe for the road. While the body shell must be crushed, some parts of the vehicle that are not structurally compromised can be salvaged and reused. This category means the car itself cannot be repaired and returned to the road, but its components might have value. Like Category A, you cannot keep a Category B vehicle to repair and drive.

Category N: Non-Structural Damage

Category N (formerly Category C, which was superseded in October 2017) indicates that the vehicle has suffered non-structural damage. This could include issues with the braking system, steering, electrics, or cosmetic damage that makes it uneconomical for the insurer to repair. Crucially, a Category N car can be repaired and returned to the road. If your car is written off as Category N, you can keep it, provided you undertake the necessary repairs to make it roadworthy and safe.

Category S: Structural Damage

Category S (formerly Category D, also superseded in October 2017) means the vehicle has suffered structural damage, but it can be repaired and returned to the road. This type of damage affects the vehicle's chassis or other load-bearing areas. Repairs to Category S vehicles are often more complex and require specialist attention to ensure the car's structural integrity is restored. Similar to Category N, you can keep a Category S vehicle, but the repair process is more stringent, and it will require a Vehicle Identity Check (VIC) by the DVLA before it can be re-registered.

Can You Keep a Total Loss Car?

The short answer is: it depends on the write-off category. As established, Category A and B vehicles cannot be kept. However, if your car is written off as a Category N or S, you absolutely have the option to retain it. This decision, however, comes with a set of responsibilities and financial considerations.

Steps to Keep a Category N or S Vehicle:

- Inform Your Insurer: Immediately contact your insurance company and clearly state that you wish to keep the written-off vehicle.

- Pay the Salvage Value: Your insurer will offer you a payout based on the car's market value, minus the salvage value of the vehicle. This 'salvage value' is essentially what the insurer believes the car is worth in its damaged state, or what they would get for it at auction. You will receive the difference.

- Handle the V5C Log Book: Send your vehicle log book (V5C) to your insurance company. However, remember to keep the yellow 'sell, transfer or part-exchange your vehicle to the motor trade' section from it. For Category S vehicles, you will need to send the complete log book to your insurance company, and then apply for a free duplicate log book using form V62 from the DVLA. The DVLA will record the vehicle's write-off category in the new log book. For Category N vehicles, you can generally keep the log book.

- Arrange Repairs: You will be responsible for arranging and funding all necessary repairs to bring the vehicle back to a roadworthy standard. This is where the costs can quickly escalate.

- Independent Inspection: It is highly recommended, and often a requirement for insurance, to have your vehicle inspected by a qualified engineer once repairs are complete. This ensures that the car is safe to return to the road and meets all legal requirements.

- Vehicle Identity Check (VIC) for Category S: If your vehicle is a Category S, you will also need to have a Vehicle Identity Check (VIC) carried out by the DVLA. This check is crucial to ensure the vehicle has not been stolen and confirms its identity before it can be re-registered for road use. Without this, you cannot get a new V5C for a Cat S car.

When to Consider Keeping a Total Loss Car

While the option to keep a Cat N or S vehicle exists, it's not always the most financially sensible choice. There are specific scenarios where retaining a written-off car might be a viable or even desirable option:

- Classic or Specialist Vehicles: If the car is a rare classic, a cherished specialist model, or holds significant historical value, investing in repairs might be worthwhile, especially if its market value is set to appreciate.

- Sentimental Value: For some, a car holds immense sentimental value, perhaps passed down through generations or associated with significant life events. In such cases, the emotional attachment might outweigh the financial implications of repairs.

- DIY Repairs or Discounted Labour: If you possess the mechanical skills to repair the car yourself, or have access to a friend or family member who can do the work at a significantly reduced cost, the repair expenses can be dramatically lowered, making retention more appealing.

- Parts Car: You might decide to keep the vehicle not to drive it, but to strip it for spare parts, either for another identical vehicle you own or to sell the components individually.

- Project Car: For enthusiasts, a written-off car can be an exciting project. This often involves a complete rebuild or customisation, where the initial lower cost of the written-off vehicle provides a cheaper starting point.

The Costs and Considerations of Keeping a Written-Off Car

It is important to note that keeping a written-off vehicle can be both expensive and time-consuming. You will need to pay for the repairs, which could be significant, and you will also need to pay for any required inspections, such as the VIC for Category S vehicles. Additionally, the value of your vehicle will be reduced because it has been written off, making it harder to sell and potentially more expensive to insure in the future.

Key Financial Implications:

- Repair Costs: These can vary wildly depending on the extent of the damage. Even for Category N cars, non-structural damage can still be costly to repair, especially if it involves complex electronics or bodywork. For Category S, structural repairs require specialist equipment and expertise.

- Inspection Fees: The cost of an independent engineer's inspection and, for Cat S vehicles, the DVLA's VIC inspection, must be factored in.

- Reduced Resale Value: A car with a write-off marker (Cat N or S) on its history will invariably have a lower resale value compared to an equivalent car with a clean history. Buyers are often wary of written-off vehicles.

- Insurance Challenges: Insuring a previously written-off vehicle can be more challenging and potentially more expensive. Some insurers may refuse to cover them, while others might charge higher premiums due to perceived higher risk.

Pros and Cons of Keeping a Written-Off Car

| Pros | Cons |

|---|---|

| Potentially lower overall cost if repairs are cheap/DIY. | Significant and unpredictable repair costs. |

| Maintain sentimental attachment to the vehicle. | Reduced resale value due to write-off marker. |

| Opportunity for a project car or parts donor. | Higher insurance premiums or difficulty obtaining cover. |

| Avoid the hassle of finding a new car immediately. | Time-consuming repair and inspection process. |

| Control over repair quality (if done well). | Potential for hidden damage or future issues. |

How to Sell a Car If It's Written Off

The process of selling a written-off car depends entirely on whether you've kept it after the initial write-off decision or if your insurer has taken ownership.

If Your Insurer Takes Ownership:

When your vehicle is written off and your insurance company pays you the current market value, they typically take ownership of the damaged vehicle. They will then arrange for its disposal, either by scrapping it (Category A or B) or selling it on to salvage buyers (Category N or S) for repair or parts. In this scenario, you don't 'sell' the written-off car; you receive a payout and transfer ownership to the insurer. You must send your V5C log book to your insurance company, keeping the yellow 'sell, transfer or part-exchange' section for your records, and inform the DVLA that your vehicle has been written off. Failure to notify the DVLA can result in a £1,000 fine.

If You Keep a Category N or S Vehicle and Later Sell It:

If you decide to keep your Category N or S written-off vehicle, repair it, and return it to the road, you are free to sell it at a later date, just like any other car. However, there are crucial considerations:

- Honest Disclosure: You are legally obliged to disclose that the vehicle was previously a write-off (Category N or S) to any prospective buyer. Failure to do so could lead to legal action against you for misrepresentation.

- Value Impact: As mentioned, the write-off marker will significantly impact the car's resale value. Be prepared for offers well below what a similar, non-written-off vehicle might fetch.

- Documentation: Keep meticulous records of all repairs, invoices, and inspection reports (especially for Cat S vehicles, including the VIC certificate). This documentation will help reassure potential buyers about the quality of the repairs and the car's roadworthiness.

- Selling Channels: Selling a written-off car can be more challenging through traditional channels. You might find more success with specialist dealers who deal with salvage vehicles, or through online auction sites where buyers are specifically looking for project cars or vehicles at a reduced price.

What About Gap Insurance?

When your car is declared a total loss, your standard motor insurance policy will typically pay out the market value of your vehicle at the time of the incident. This amount can often be significantly less than what you originally paid for the car, especially if you bought it new or on finance, due to depreciation. This is where Gap Insurance comes in.

Gap Insurance (Guaranteed Asset Protection) is designed to cover the 'gap' between your motor insurer's payout and either the original purchase price of your vehicle or the outstanding finance balance. There are a few different types of policies, depending on how you funded your vehicle:

Combined Return to Invoice (RTI) Gap Insurance:

If you paid cash for your vehicle, paid a sizeable deposit, or financed it, Combined RTI Gap cover will pay out the shortfall between the cost of your vehicle and the market value at the point of claim. This means you'd get back the original purchase price, ensuring you're not out of pocket due to depreciation. This cover protects you whether you use your vehicle for private or business use.

Lease/Contract Hire Gap Insurance:

If you leased your vehicle or it's under a contract hire agreement, this type of Gap Insurance will cover you for the shortfall on your lease agreement after your motor insurer settlement. This is crucial as you're often liable for the remaining lease payments even if the car is written off. Some policies even allow you to transfer your cover to a new vehicle within a certain period if you change your car.

Understanding Gap Insurance is vital for financial peace of mind, as it can prevent significant financial loss should your vehicle be declared a total loss.

Frequently Asked Questions About Car Write-Offs

Q: What does 'total loss' mean for a car?

A: 'Total loss' means that the cost of repairing your car, plus other associated costs like recovery and storage, is deemed to be more than its market value at the time of the incident. Your insurer will then 'write off' the car and pay you its market value, rather than funding the repairs.

Q: Can I get insurance on a written-off car?

A: Yes, it is possible to get insurance on a Category N or S written-off car once it has been repaired and deemed roadworthy. However, some insurers may be reluctant to offer cover, or they might charge higher premiums due to the car's history. It's essential to disclose its write-off status to any prospective insurer.

Q: Do I have to tell DVLA if my car is written off?

A: Yes, absolutely. Your insurance company will usually handle this notification if they take possession of the vehicle. However, if you decide to keep a Category N or S vehicle, you are responsible for ensuring the DVLA is informed and that the correct procedures for updating the V5C log book are followed. Failure to notify the DVLA can result in a fine of up to £1,000.

Q: Is a Cat N car safe to drive after repair?

A: A Category N car can be safe to drive after repair, provided the repairs have been carried out to a professional standard and the vehicle has been thoroughly inspected by a qualified mechanic to ensure its roadworthiness and safety. While the damage was non-structural, proper repair is still crucial.

Q: Is a Cat S car safe to drive after repair?

A: A Category S car can be safe to drive after repair, but it requires more stringent checks due to the original structural damage. It must undergo professional structural repairs and pass a DVLA Vehicle Identity Check (VIC) to confirm its identity and ensure it's safe for the road. Once these steps are completed, it can be driven safely.

Conclusion

Understanding what happens when your car is written off is crucial for navigating what can be a stressful situation. While a 'total loss' declaration might sound like the end of the road for your vehicle, for Category N and S write-offs, there's a clear path to getting your car back on the road, albeit with significant considerations. Weighing the financial implications, the time commitment, and the sentimental value is key to making an informed decision. Always prioritise safety and ensure any repairs are carried out to the highest standard, and remember the importance of notifying the DVLA and understanding your insurance options, including Gap Insurance, for complete peace of mind.

If you want to read more articles similar to Car Written Off? Your UK Guide to Total Loss, you can visit the Vehicles category.