30/12/2021

When the unexpected happens on the road, a car accident can instantly turn your day upside down. Beyond the immediate shock and concern for safety, one of the first questions that often springs to mind is: 'How long do I have to make a claim?' Whether it's sorting out car repairs or addressing personal injuries, navigating the aftermath of an accident can feel overwhelming. Understanding the specific time limits and best practices for filing a claim in the UK is absolutely vital to ensure you receive the compensation you're entitled to.

While your initial instinct might be to get everything sorted as quickly as possible, there are nuanced considerations regarding when and how to file a claim. In some instances, a brief delay might actually work in your favour, allowing for a more comprehensive assessment of damages. However, waiting too long can severely jeopardise your claim. This guide will walk you through the various timelines, legal requirements, and practical advice to help you manage your car accident claim effectively in the United Kingdom.

- Understanding UK Car Accident Claim Timelines

- The Immediate Aftermath: Notifying Your Insurer

- To Wait or Not to Wait? Weighing the Pros and Cons of Filing a Claim

- Specific Claim Types and Their Legal Deadlines

- Protecting Your Claim: Essential Steps After an Accident

- When to Seek Expert Legal Advice: The Role of a Solicitor

- Comparative Overview: Vehicle Damage vs. Personal Injury Claims

- Frequently Asked Questions About Car Accident Claims

- What happens to my insurance costs after making an insurance claim?

- What if my policy's window to file a claim is too short?

- Can I claim if the accident was partly my fault?

- What happens if I miss the six-year deadline for vehicle damage or three-year deadline for personal injury?

- Can I claim through my own insurance and recover the excess?

- Is vehicle damage compensation taxable?

- What if I no longer own the car?

- Can I claim for a leased or financed vehicle?

- Conclusion

Understanding UK Car Accident Claim Timelines

The UK legal system provides specific timeframes within which you can make a claim following a car accident. It's crucial to differentiate between the time you have to *notify* your insurer and the legal deadlines for *filing* a formal claim. Generally speaking, there are two primary categories of claims, each with its own statutory limitation period:

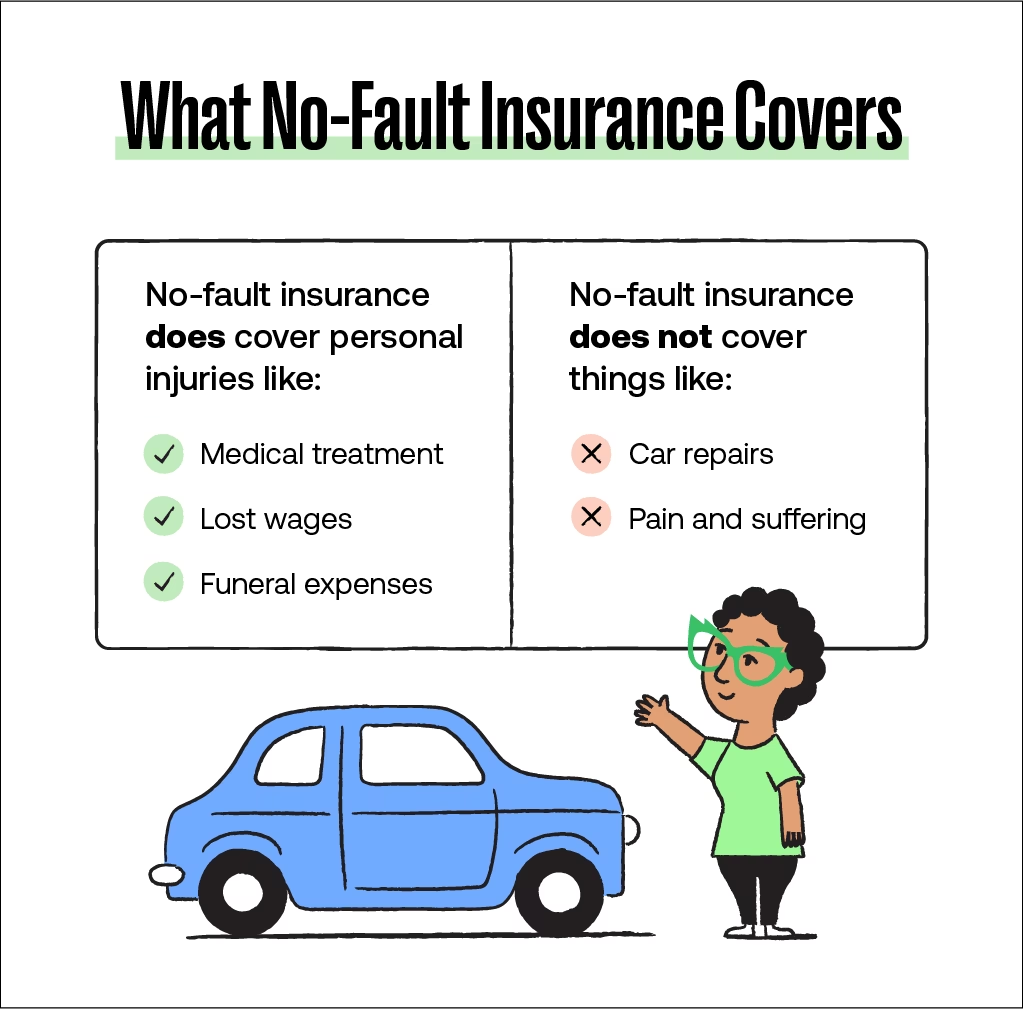

- Vehicle Damage Claims: For damage to your car or other property, the general legal limit in England and Wales is six years from the date of the accident. This extended period allows you to seek reimbursement for repair costs, the vehicle's market value if written off, and other related expenses caused by another driver's negligence.

- Personal Injury Claims: If you've sustained injuries in the accident, the time limit for making a personal injury claim is typically three years from the date of the accident, or from the date you became aware of your injuries (if they weren't immediately apparent). This shorter period underscores the importance of seeking medical attention promptly and initiating the claims process for injuries without undue delay.

While these are the legal maximums, it's incredibly important to note that your insurance provider will almost certainly have a much shorter notification period stipulated in your policy. Failing to inform them within their specified timeframe, which can be as short as 24-48 hours, could invalidate your claim entirely. Always check your policy documents for these specific terms.

The Immediate Aftermath: Notifying Your Insurer

Even if you're not entirely sure whether you'll make a claim, or if the damage seems minor, the golden rule after any car accident is to inform your insurer as soon as possible. Most policies require notification within 24 hours of an incident. This isn't necessarily about filing the full claim immediately, but rather about keeping your insurer 'in the loop' about any changes to your circumstances that might affect your policy.

Why is this so important? Insurers need to be aware of potential liabilities or incidents that could lead to a claim down the line. Delaying notification could be seen as a breach of your policy terms, potentially leading to your claim being denied, even if it's otherwise valid. While the legal deadline for filing a claim can be years away, the window for initial notification is often very narrow.

When it comes to the actual *filing* of the claim – that is, submitting all the necessary documentation and details for assessment – a good rule of thumb is to do so within two weeks of the accident. As time progresses, it becomes increasingly difficult to gather relevant information. CCTV footage might be deleted, witness memories can fade, and the scene of the accident might change, all of which can hinder your case. Swift action helps preserve crucial evidence and ensures a smoother process.

To Wait or Not to Wait? Weighing the Pros and Cons of Filing a Claim

While prompt notification to your insurer is essential, the decision of when to formally file your comprehensive claim can involve a delicate balance. There are legitimate reasons why some individuals might consider waiting a short period before submitting all the details, alongside significant risks associated with prolonged delays.

Pros of Waiting (Carefully!)

- More Comprehensive Claim: Most insurance providers will only allow you to file one claim per accident. If you rush the process, you might overlook or forget to include items or aspects of damage that insurance would have covered. Waiting a short period can allow for a thorough assessment of all vehicle damage, personal property damage, and potential hidden issues that may not be immediately apparent. This ensures you make the most of your available coverage.

- Accurate Assessment of Full Damage Cost: The true cost of fixing a damaged vehicle, especially if there's structural damage, can take weeks or even months to fully assess. Waiting allows mechanics to conduct a complete inspection, identify all necessary repairs, and provide accurate estimates. This helps ensure your claim covers the full extent of the financial outlay required to restore your vehicle to its pre-accident condition.

Cons of Waiting Too Long

- Delayed Reimbursement or Payment: This is perhaps the most immediate drawback. If you need your vehicle repaired quickly or are facing mounting medical bills, delaying the claim process simply pushes back the date you'll receive payment or reimbursement. Depending on your financial circumstances, this could cause significant hardship.

- Possible Late Bill Payments and Credit Score Impact: Should you delay filing your claim and it results in the late payment of important charges or medical bills, you could face penalties. In severe cases, past-due payments might be reported to credit reporting agencies, which can negatively impact your credit score and future financial standing.

- Loss of Crucial Evidence: As mentioned, time erodes evidence. Witness statements become less reliable, CCTV footage is overwritten, and the physical scene of the accident might be altered. The longer you wait, the harder it becomes to gather compelling evidence to support your claim, especially if liability is disputed.

- Increased Complexity and Scrutiny: Insurers may view delayed claims with greater suspicion, potentially leading to increased scrutiny and a more complex, drawn-out investigation process. This can add stress and difficulty to an already challenging situation.

Specific Claim Types and Their Legal Deadlines

Understanding the specific legal deadlines for different types of claims is paramount. While insurer notification periods are often much shorter, these statutory limits dictate the absolute maximum time you have to initiate legal proceedings.

Vehicle Damage Claims: The Six-Year Window

In England and Wales, you generally have six years from the date of the car accident to make a claim for property damage. This includes damage to your vehicle, personal belongings within the vehicle, and any other property affected. This timeframe applies to civil claims and allows you to seek reimbursement for repair or replacement costs if another driver was at fault. This limit is set out in the Limitation Act 1980.

What you can claim for under vehicle damage typically includes:

- Repair costs or the full market value if your car is deemed a 'write-off' (beyond economical repair).

- Hire car costs incurred while your vehicle is being repaired or until a replacement vehicle is sourced.

- Towing and recovery charges from the accident scene.

- Loss of use or inconvenience due to not having your vehicle.

- Personal property damaged in the vehicle (e.g., phones, glasses, luggage).

- Excess recovery if you claimed through your own insurer but the other driver was at fault.

If the accident was the other driver's fault, their insurance company should cover your damages. If liability is admitted, you can often file the claim directly through their insurer. If you use your own insurance, your provider may reclaim the costs on your behalf from the at-fault party's insurer.

Personal Injury Claims: The Three-Year Deadline

If your accident resulted in personal injury, you must bring the injury claim within three years from the date of the accident or from when you became aware of your injuries (the 'date of knowledge'). While you can still claim for vehicle damage within the longer six-year limit, it is almost always more efficient and advisable to handle both claims concurrently, especially if they stem from the same incident. A solicitor can help ensure both parts of your case are filed correctly and on time.

Exceptions to the Rule: When Timelines Differ

There are some important exceptions to these standard time limits, primarily designed to protect vulnerable individuals:

- Minors (under 18): For individuals under 18 at the time of the accident, the three-year limit for personal injury claims (and six years for property damage) only begins on their 18th birthday. This means they have until their 21st birthday (for personal injury) or 24th birthday (for property damage) to make a claim.

- Mental Capacity: If the claimant lacks mental capacity (e.g., due to severe brain injury from the accident), there may be no time limit for making a claim until they regain capacity. A 'litigation friend' (often a family member or guardian) can bring the claim on their behalf.

- Unknown Third Party: If the other driver fled the scene (a 'hit-and-run') or is untraceable, your claim may be handled by the Motor Insurers’ Bureau (MIB). The MIB is a non-profit organisation funded by insurers that compensates victims of uninsured and untraced drivers. However, strict deadlines apply to MIB claims, typically within three years for personal injury and property damage, and often much sooner for initial notification.

Protecting Your Claim: Essential Steps After an Accident

Regardless of whether you plan to claim immediately or slightly later, taking the right steps at the scene and in the days following the accident is absolutely paramount to preserving your right to claim. Here's what you should do:

- Take photos: Capture clear photos of the damage to all vehicles involved, the accident scene, road conditions, and any relevant road signs or markings.

- Exchange details: Get the other driver's name, address, phone number, vehicle registration, and insurance information. Also, note down details of any witnesses.

- File a police report: Especially for hit-and-run cases, serious accidents, or if there are injuries, notify the police. A police report can be valuable evidence.

- Contact your insurer: Notify them of the incident as soon as possible, ideally within 24 hours, even if you're unsure about making a claim.

- Keep records: Maintain meticulous records of all communications, repair estimates, invoices, medical reports, and any other expenses incurred as a result of the accident.

Having thorough documentation will significantly strengthen your case, should you decide to proceed with a claim, whether immediately or later within the legal timeframes.

When to Seek Expert Legal Advice: The Role of a Solicitor

For straightforward claims involving minor damage and clear liability, you might feel comfortable managing the claim yourself or directly with your insurer. However, a solicitor can be an invaluable asset in several situations:

- The other party denies fault: If liability is disputed, a solicitor can gather evidence, negotiate on your behalf, and represent you if the case goes to court.

- You're also claiming for injury: Personal injury claims can be complex, involving medical assessments, loss of earnings, and long-term care needs. A solicitor ensures you receive fair compensation for all aspects of your injury.

- The insurer delays or disputes payment: If you encounter difficulties with your own insurer or the third-party insurer, a solicitor can intervene and push for a resolution.

- The accident involved an uninsured or untraced driver: Dealing with the MIB has specific rules and deadlines that a solicitor can help you navigate.

Legal support ensures you don't settle for less than you're entitled to and that all aspects of your claim are handled correctly within the appropriate timeframes.

Comparative Overview: Vehicle Damage vs. Personal Injury Claims

| Claim Type | Standard Legal Time Limit (England & Wales) | Key Considerations |

|---|---|---|

| Vehicle Damage | 6 years from accident date | Covers repairs, write-off value, hire car, towing, personal property. Can be filed separately or with injury claim. |

| Personal Injury | 3 years from accident date or date of knowledge | Covers medical costs, lost earnings, pain and suffering. Often advisable to handle with vehicle damage claim. |

| Minors | From 18th birthday (3 years for PI, 6 years for VD) | Time limit starts when claimant turns 18. |

| Mental Incapacity | No time limit until capacity regained | Claim can be brought by a 'litigation friend'. |

| Uninsured/Untraced Driver (MIB) | Generally 3 years (strict notification rules apply) | Specific rules and procedures with the Motor Insurers’ Bureau. |

Frequently Asked Questions About Car Accident Claims

What happens to my insurance costs after making an insurance claim?

Typically, your insurance premiums will increase after making a claim, especially if you were deemed at fault. You might also lose any 'no-claims discount' you've accumulated. However, if you have 'accident forgiveness' on your policy, you're usually protected from an increase due to a previous safe driving record. It's always best to speak to your provider to understand the potential impact on your rate and whether it's more cost-effective to pay for minor damages out of pocket.

What if my policy's window to file a claim is too short?

Many insurance providers reserve the right to set their own time limits for filing claims. If you feel your provider has set an unfair or unusually short time limit, you should speak with an agent about a possible compromise or other options that might help you file in time while still getting the cover you need. In exceptional circumstances (e.g., hospitalisation), insurers may offer extensions, but these are at their discretion.

Can I claim if the accident was partly my fault?

Yes, you may still be entitled to partial compensation, depending on your level of responsibility for the accident. This is known as 'contributory negligence'. Your compensation will be reduced by the percentage you were deemed at fault.

What happens if I miss the six-year deadline for vehicle damage or three-year deadline for personal injury?

If you miss these statutory deadlines, your claim is likely to be 'time-barred', meaning you've lost your legal right to pursue it. Courts rarely accept claims filed after the deadline unless there are truly exceptional circumstances, such as the claimant being a minor or lacking mental capacity at the time.

Can I claim through my own insurance and recover the excess?

Yes. If the other driver is at fault, you can claim through your own comprehensive insurance policy. Once liability is settled and the other party's insurer accepts fault, your insurer will typically recover your excess from them and return it to you. This can be a quicker way to get your car repaired, but it might temporarily affect your no-claims bonus until the excess is recovered.

Is vehicle damage compensation taxable?

No. Compensation received for property damage in car accidents is generally not taxable in the UK, as it is intended to restore you to your pre-accident financial position, not to generate profit.

What if I no longer own the car?

You can still claim for the damage if you owned the car at the time of the accident and can provide documentation to prove the loss or cost of repair/replacement at that time. The claim is based on the damage incurred when you owned the vehicle.

Can I claim for a leased or financed vehicle?

Yes. If your vehicle is leased or financed, you can still claim for damage. However, the legal owner of the vehicle is typically the finance company or leasing company. You may need to claim on their behalf, or they may pursue the claim directly, depending on the terms of your agreement. Always inform your finance or leasing company immediately after an accident.

Conclusion

Navigating the aftermath of a car accident requires a clear understanding of your rights and the time limits for making a claim. While the UK legal system provides up to six years for vehicle damage and three years for personal injury, acting promptly is always the wisest course of action. Immediate notification to your insurer, thorough documentation of the scene and damages, and prompt medical attention for injuries are all critical steps that can significantly strengthen your position.

While there can be minor advantages to taking a short period to assess the full extent of damage, the risks of significant delay—such as loss of evidence, increased scrutiny, and financial hardship—far outweigh these benefits. If you find yourself in a complex situation, with disputed liability, significant injuries, or issues with uninsured drivers, do not hesitate to seek expert legal advice from a solicitor. By being proactive and informed, you can protect your rights and ensure you receive the compensation you're entitled to, helping you move forward after an accident with confidence.

If you want to read more articles similar to Car Accident Claims: UK Timelines Explained, you can visit the Insurance category.