14/11/2014

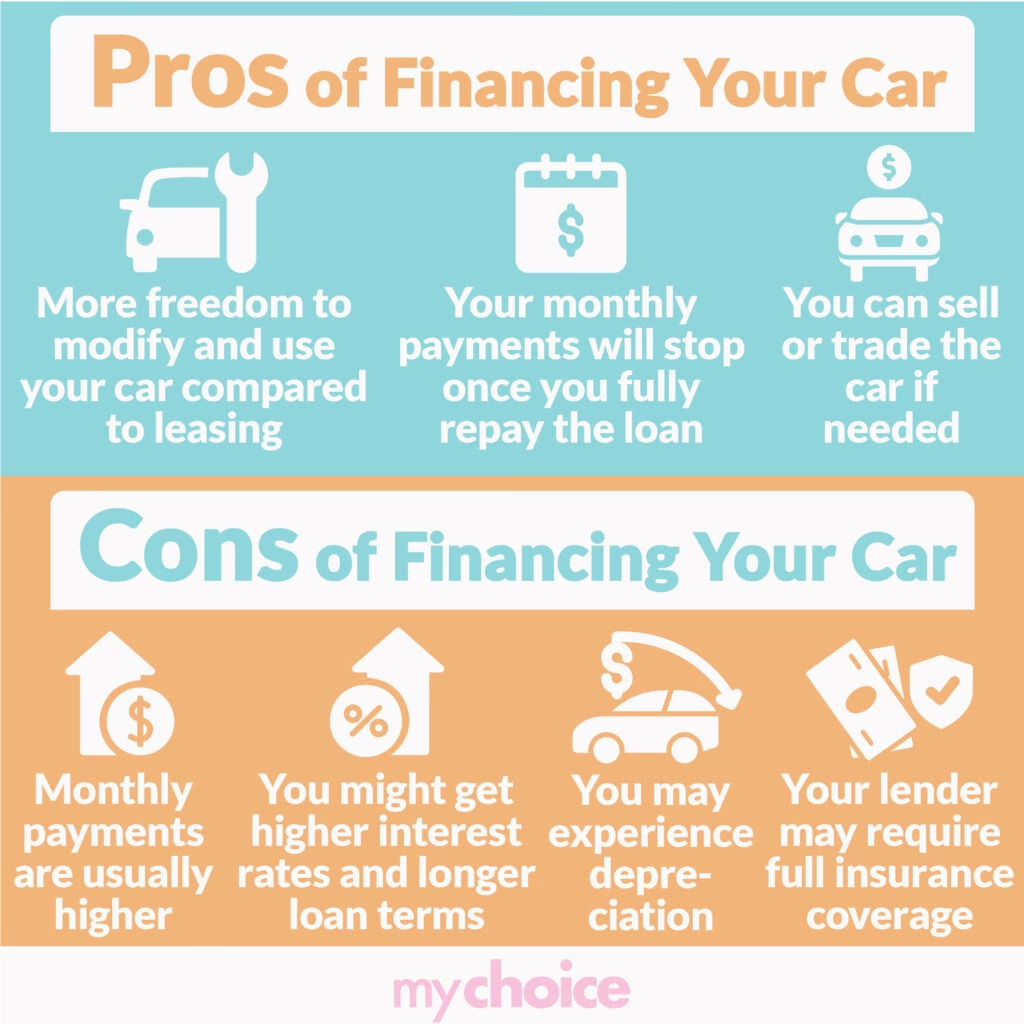

Owning a car in the UK can bring immense freedom, but when financial circumstances shift unexpectedly, the burden of car finance payments can quickly become overwhelming. Whether it’s due to job loss, unforeseen expenses, or simply a change in your personal situation, finding a responsible way out of a finance agreement is crucial. This is where Voluntary Termination, or VT, comes into play – a powerful statutory right for UK consumers that can offer a much-needed escape route.

Today, we're diving deep into the intricacies of Voluntary Termination of car finance. We'll explore precisely what it is, your fundamental rights under the Consumer Credit Act, and the practical steps involved. More importantly, we'll dissect the financial impacts, helping you understand the nuances of this process so you can make an informed decision that's truly best for your future.

- What is Voluntary Termination of Car Finance?

- Voluntary Termination vs. Voluntary Surrender: A Crucial Distinction

- Your Rights Under the Consumer Credit Act 1974

- Common Reasons to Consider Voluntary Termination

- How Voluntary Termination Car Finance Works in Practice

- How Long Does Voluntary Termination Take?

- Financial Drawbacks and Considerations of Voluntary Termination

- Does Voluntary Termination Affect Your Credit Score?

- Frequently Asked Questions About Voluntary Termination

- Last Thoughts

What is Voluntary Termination of Car Finance?

At its core, Voluntary Termination (VT) is a legal mechanism that allows you to end your car finance agreement before its official contract end date. This option isn't a new loophole; it has been a safeguard for UK drivers since the enactment of the Consumer Credit Act of 1974. It provides a vital safety net for individuals facing significant financial changes, ensuring they aren't trapped in an unaffordable contract.

When you choose VT, your finance contract is officially terminated, and you are required to return the vehicle to the finance provider. Crucially, this means you cannot keep the car. The primary benefit of VT is that it limits your financial liability, providing a structured and legally protected way to hand back a vehicle you can no longer afford, without facing the full brunt of remaining payments.

Voluntary Termination vs. Voluntary Surrender: A Crucial Distinction

While their names might sound similar, Voluntary Termination and Voluntary Surrender are vastly different concepts with distinct financial implications. Understanding this difference is paramount to avoiding future charges and making the right decision.

Voluntary Surrender

Voluntary surrender occurs when you simply return the car to the finance company because you can no longer afford it, but without invoking your specific rights under the Consumer Credit Act. In this scenario, you hand back the vehicle, but you remain fully liable for any outstanding loan balance. This often includes any shortfall that arises if the car is sold at auction for less than the amount you still owe. Voluntary surrender can, therefore, leave you with a significant debt and potentially a negative mark on your credit file, as it’s often viewed as a failure to meet your contractual obligations.

Voluntary Termination (VT)

Conversely, Voluntary Termination is a statutory right. If you successfully exercise VT, your financial liability is legally capped. Specifically, your obligation is limited to 50% of the Total Amount Payable under the agreement, plus any arrears you might have. Once this threshold is met and the car is returned, you are not obligated for any further payments. This legal cap is the key differentiator, protecting consumers from open-ended debt.

Here’s a quick breakdown to highlight the differences:

| Feature | Voluntary Termination (VT) | Voluntary Surrender |

|---|---|---|

| Legal Basis | Consumer Credit Act 1974 (Section 99) | Informal agreement with lender |

| Liability Cap | Capped at 50% of Total Amount Payable + arrears | Full remaining loan balance + any shortfall after sale |

| Car Return | Required | Required |

| Credit Impact | Appears on credit file; generally not negative if criteria met | Can negatively impact if balance unpaid |

| Control | Consumer's statutory right | Lender's discretion |

| Purpose | Legal exit when affordability issues arise | Returning car, but still owing money |

Understanding this fundamental difference is crucial. Opting for voluntary surrender when you could have qualified for VT can lead to significant and avoidable financial burdens. Always ensure you are clear about which option you are pursuing when communicating with your finance provider.

Your Rights Under the Consumer Credit Act 1974

The Consumer Credit Act 1974 is the cornerstone of consumer protection in the UK regarding credit agreements. Voluntary Termination is specifically enshrined under Section 99 of this Act. This section grants consumers the unequivocal right to terminate regulated hire-purchase (HP) or conditional sale agreements before the final payment is due.

The primary criterion for exercising this right is that you must have paid at least 50% of the Total Amount Payable under the agreement. It's vital to understand what "Total Amount Payable" means here. It's not just the sum of your monthly payments; it includes the original vehicle cost, all interest charges, and any additional fees (such as an option to purchase fee in a PCP agreement) outlined in your contract. For example, if your total amount payable over the lifetime of the agreement is £20,000, you must have paid at least £10,000 to qualify for VT.

What if you haven't quite reached the 50% threshold? The Act allows you to make a lump sum payment to cover the difference and reach this threshold. Once that payment is made, you become eligible to proceed with the termination. This flexibility ensures that the right to VT remains accessible even if you're slightly short of the required payment at the time you need to terminate.

It's important to note that while this is a consumer right, you must fulfil these terms and conditions to be eligible. The finance company cannot refuse your request if you meet the criteria, though they may try to discourage you or make the process seem more complex than it is.

Common Reasons to Consider Voluntary Termination

Voluntary Termination is primarily a solution for affordability issues. It's not a convenient way to get a new car or simply change your mind about your current vehicle. The reasons for considering VT typically revolve around significant and often unforeseen financial shifts:

- Job Loss or Reduced Income: Losing your employment or experiencing a substantial reduction in your income can make regular car payments unsustainable.

- Significant Unexpected Costs: A major home repair, medical emergency, or other large, unforeseen expense can strain your finances to the point where car payments become a luxury you can no longer afford.

- Big Change in Financial Circumstances: This could encompass a range of situations, such as separation or divorce leading to a single income, or needing to support a new dependent.

- No Longer Needing the Car: While less common for affordability, if your lifestyle changes (e.g., moving to an area with excellent public transport, or working from home permanently) and the car becomes an unnecessary expense, VT offers a way out.

- Other Affordability Issues: Any other situation where maintaining the payments genuinely becomes a hardship.

The key takeaway here is that VT is a protective measure for consumers facing genuine financial hardship. It's not intended as a 'get out of jail free' card for those who simply fancy a new model or have buyer's remorse.

How Voluntary Termination Car Finance Works in Practice

Voluntary Termination is an option available for both new and used cars financed through regulated Personal Contract Purchase (PCP) or Hire Purchase (HP) agreements. The general steps to apply and initiate the VT process are relatively straightforward, provided you are organised and clear in your communication:

- Review Your Finance Agreement: Start by thoroughly checking your contract. Identify the 'Total Amount Payable' and calculate 50% of that figure. Also, assess your car's condition. Document any existing damage with photos or videos, as this will be important later.

- Contact the Finance Company: Clearly state your intention to terminate your agreement under Section 99 of the Consumer Credit Act 1974. It's best to do this in writing, either by letter or email, so you have a clear record of your communication. Keep a copy for your records.

- Settle Any Outstanding Payments: If you haven't yet reached the 50% threshold, you'll need to make a payment to cover the difference. Ensure this payment is clearly reconciled with the finance company. If you have any arrears, these will also need to be cleared to qualify for VT.

- Arrange Vehicle Return: The finance company will then provide instructions for returning the vehicle. This might involve dropping the car off at a specified location or arranging for collection services. Be present during the handover and ensure a full vehicle inspection is conducted and documented by both parties.

To ensure a smoother transition, it's crucial to maintain clear and consistent communication with your finance provider. Keep a meticulous record of all phone calls (including dates, times, and names of people you spoke to), emails, and letters. This documentation will be invaluable if any disputes arise.

Voluntary Termination for PCP Agreements

PCP (Personal Contract Purchase) agreements can be more complex when it comes to the 50% threshold for VT. In a PCP agreement, your monthly payments largely cover the depreciation of the vehicle and interest. A significant portion of the total finance amount is deferred to the end of the agreement in the form of a large lump sum, often called a 'balloon payment' or 'Guaranteed Minimum Future Value' (GMFV).

Because of this structure, even if you are halfway through your contract term, you may find that your monthly payments alone have not yet reached 50% of the Total Amount Payable (which includes the balloon payment, interest, and fees). For example, on a £20,000 Total Amount Payable PCP, halfway through a 4-year term, you might have only paid £7,000 in monthly instalments. To qualify for VT, you would need to pay the remaining £3,000 to reach the £10,000 (50%) threshold.

It's important to understand that any payments you make beyond the 50% threshold will not be refunded. So, if you've paid £12,000 of a £20,000 total, you won't get the £2,000 difference back. This is why it's crucial to assess whether VT is the most financially beneficial option, especially if you're close to or have exceeded the 50% mark and the car's market value is strong.

Voluntary Termination for HP Agreements

HP (Hire Purchase) agreements are generally much simpler when it comes to Voluntary Termination. With HP, your repayments are spread more evenly across the entire term of the agreement, covering both the capital cost of the car and the interest. There isn't a large balloon payment deferred to the end.

Consequently, when you reach the halfway point of your HP contract term, it's highly likely that you will have automatically qualified for the 50% rule payment requirement. For example, if you have a 4-year HP agreement, you will typically have paid 50% of the total amount payable by the end of year 2. Similar to PCP, if you are slightly short of the 50% mark, you can pay the difference to become eligible.

How Long Does Voluntary Termination Take?

Once you formally apply for Voluntary Termination and meet all the necessary criteria, the process itself should be relatively quick. The finance company is legally obliged to facilitate the termination once you’ve exercised your right under the Consumer Credit Act.

However, it's not uncommon for finance companies to be less than enthusiastic about VT, as it means they lose out on future interest payments. Some may inadvertently (or intentionally) lengthen the application time by requesting additional information, making the process seem complicated, or trying to steer you towards voluntary surrender. They might also try to arrange collection at an inconvenient time or dispute the car's condition.

To speed up the process and ensure a smooth experience, it's essential to:

- Be Clear and Assertive: State unequivocally that you are exercising your right to Voluntary Termination under Section 99 of the Consumer Credit Act 1974.

- Understand Your Rights: Know the difference between VT and surrender, and don't be swayed by suggestions that you're liable for more than the 50% cap.

- Meet All Requirements: Ensure you’ve paid the 50% threshold and that any arrears are cleared before you initiate the process.

- Document Everything: As mentioned, keep records of all communications, dates, and times. Take detailed photos and videos of the car's condition before handover.

If you feel the finance company is unduly delaying or obstructing your right to VT, you can seek advice from organisations like Citizens Advice or the Financial Ombudsman Service.

Financial Drawbacks and Considerations of Voluntary Termination

While Voluntary Termination offers a vital escape route, it's important to be aware of the potential financial consequences and ensure you've considered all angles before proceeding.

- Penalties for Excessive Wear and Tear or Mileage: When you return the vehicle, it must be in a reasonable condition for its age and mileage, accounting for what's known as 'fair wear and tear'. This includes minor scuffs, small chips, or general ageing. However, any damage beyond fair wear and tear (e.g., large dents, deep scratches, broken components, or significant interior damage) or exceeding the agreed mileage limit in your contract may incur additional charges. The finance company will typically conduct an inspection upon return. It is crucial to document the car's condition thoroughly before handover to dispute any unfair charges.

- Impact on Your Credit File: This is a point of common confusion. Voluntary Termination itself does not inherently harm your credit score. It will, however, appear on your credit file as a 'Voluntary Termination' entry. While this isn't a negative mark in the same way a default or missed payment would be, future lenders reviewing your credit history may view it as a sign that you previously had financial difficulties or were unable to maintain a finance agreement to its full term. This *could* potentially influence their decision-making when you apply for credit in the future, even if your score itself hasn't dropped. It's a flag, rather than a penalty.

- Equity Considerations: If you have paid significantly more than 50% of the total amount payable, or if the car's current market value is substantially higher than the remaining balance you owe, exercising VT might not be the most financially advantageous option. In such cases, you might have 'positive equity' in the vehicle. It could be more beneficial to sell the car privately or to a dealership, use the proceeds to pay off the outstanding finance, and potentially walk away with some cash. With VT, any payments beyond the 50% threshold are not refunded, so you forgo any potential equity. Always calculate your position carefully.

Does Voluntary Termination Affect Your Credit Score?

As touched upon, this is a frequently asked question with a nuanced answer. No, Voluntary Termination does not, by itself, negatively impact your credit score in the same way a missed payment, default, or County Court Judgment (CCJ) would. It is a legal right, not a failure to meet your obligations.

However, it will be recorded on your credit report, typically under the account history with the finance provider. Future lenders, when assessing your creditworthiness, will see this entry. While it doesn't lower your numerical score, they may interpret it as an indicator of past financial strain or a reduced ability to see a contract through to its natural conclusion. Some lenders might be more cautious when offering you credit in the future, particularly for car finance, as they might perceive a higher risk. It's a data point they will consider as part of their overall assessment of your financial reliability.

Frequently Asked Questions About Voluntary Termination

Can I voluntarily terminate my agreement if I have missed payments?

Generally, no. To exercise your right to Voluntary Termination, your account should be up to date. If you have arrears (missed payments), you will typically need to clear these before the finance company will process your VT request. The 50% rule only applies to the principal and interest, not outstanding arrears.

Can I voluntarily terminate a used car finance agreement?

Yes, absolutely. Voluntary Termination applies to any regulated hire-purchase or conditional sale agreement, regardless of whether the car was new or used at the time of purchase, provided it falls under the Consumer Credit Act 1974.

What if the finance company tries to refuse my request?

If you meet all the criteria (primarily the 50% paid threshold and cleared arrears), the finance company cannot legally refuse your request for Voluntary Termination. They may try to dissuade you or delay the process. If you encounter resistance, reiterate your rights under Section 99 of the Consumer Credit Act 1974. If they continue to refuse or create unreasonable obstacles, you should escalate your complaint through their internal complaints procedure and, if unresolved, contact the Financial Ombudsman Service (FOS).

Will I get any money back if I’ve paid more than 50%?

No, unfortunately, you will not receive a refund for any amount paid over the 50% threshold when you voluntarily terminate. This is a common misconception. The 50% rule caps your liability; it doesn't entitle you to a refund for overpayment. If you believe your car is worth significantly more than the outstanding finance, selling it privately or trading it in might be a better option, as you could potentially recover some of that equity.

What condition does the car need to be in for VT?

The vehicle must be in a "reasonable condition" for its age and mileage, allowing for fair wear and tear. This means minor scratches, small chips, and general wear that would be expected. However, significant damage (e.g., large dents, major mechanical faults not due to normal use, ripped interior, non-functioning electrics) or excessive mileage beyond the agreed limit in your contract will likely result in additional charges. It's always wise to have the car professionally cleaned and ensure it's in the best possible condition before handover to minimise potential charges.

Last Thoughts

Voluntary Termination is a powerful and essential statutory right for UK car finance consumers. It provides a legal and structured way to walk away from a car finance agreement without incurring major penalties, provided you follow the rules and understand your obligations.

It's not a decision to be taken lightly, and it requires careful consideration of your financial situation, the specifics of your finance agreement, and the potential implications. By going through the process carefully, meeting all the requirements, and understanding any financial impacts along the way, you can navigate challenging circumstances with confidence and make an informed choice that safeguards your financial well-being.

Remember, knowledge is power. Arm yourself with the facts, understand your rights, and don't hesitate to seek independent advice if you're unsure. This safeguard exists to protect you, and knowing how to use it correctly can make all the difference when life throws unexpected financial curveballs your way.

If you want to read more articles similar to Voluntary Termination: Your Car Finance Exit, you can visit the Automotive category.