05/04/2016

Securing a car on a tight budget can often feel like an impossible task, especially with the rising cost of living. Many believe that getting a reliable set of wheels for under £100 a month is merely a pipe dream. However, with careful planning, understanding of finance options, and knowing where to look, this aspiration is very much within reach for many UK motorists. This guide aims to demystify the process, helping you navigate the world of affordable car finance and potentially put you behind the wheel of a vehicle that fits your budget.

The idea of a car payment below £100 per month is incredibly appealing, and it's a budget point that many people are actively searching for. Platforms like Auto Trader, for instance, often list thousands of vehicles available with monthly finance payments in this bracket. This indicates a significant market for value cars, proving that affordable motoring is a tangible reality across the UK. However, it's crucial to understand the underlying factors that contribute to such low monthly outgoings, as they often involve specific finance terms.

- The Reality of Car Finance Under £100/Month

- Where to Find Your Next Car

- Types of Cars to Expect

- Understanding Car Finance: Key Terms

- Factors Affecting Your Monthly Payment

- Hidden Costs and Ongoing Expenses

- Tips for Finding the Best Deal

- Pros and Cons of Low Monthly Payments

- Comparative Table: How Finance Variables Impact Payments

- Frequently Asked Questions (FAQs)

- Conclusion

The Reality of Car Finance Under £100/Month

When you see a car advertised with a monthly payment of less than £100, it's essential to look beyond the headline figure. These attractive rates are typically based on certain assumptions, which commonly include a substantial deposit, a specific loan term, and an annual mileage limit. For example, many offers, including those often seen on large platforms, might be calculated with a £1,000 deposit, a 36-month (3-year) term, and an annual mileage allowance of 10,000 miles. Altering any of these variables will directly impact your monthly payment. A smaller deposit will increase it, as will a shorter term. Exceeding mileage limits on certain finance types can also lead to additional charges.

The cars typically available at this price point are generally not brand new, nor are they luxury models. They are often smaller, more economical vehicles, or slightly older models that have depreciated in value. This makes them ideal for first-time buyers, those needing a second car for short commutes, or individuals prioritising low running costs over performance or prestige.

Where to Find Your Next Car

The digital age has made finding affordable cars easier than ever. Online marketplaces are your first port of call, offering a vast selection:

- Online Marketplaces: Websites like Auto Trader are invaluable, providing filters to search specifically for cars within your desired monthly budget. They aggregate listings from dealerships across the country, giving you a broad overview of what's available.

- Dealerships: Many franchised and independent dealerships specialise in used cars and offer various finance packages. It's always worth visiting local dealerships to see their stock and discuss finance options in person. They might have deals not widely advertised online.

- Specialist Finance Brokers: Some brokers specialise in helping individuals with various credit histories find car finance. They can often access a wider range of lenders and potentially secure more favourable terms for your specific situation.

- Manufacturer Approved Used Schemes: While potentially slightly higher in price, manufacturer-approved used cars often come with warranties and assurances that can provide peace of mind, potentially offsetting slightly higher monthly payments with reduced risk of unexpected repair costs.

Types of Cars to Expect

When budgeting for under £100 a month, you'll primarily be looking at cars from the smaller end of the spectrum, or slightly older, higher-mileage models. Think city cars and superminis known for their reliability and fuel efficiency. Excellent examples often found in this price bracket include:

- Volkswagen UP! / Skoda Citigo / SEAT Mii: These triplets are popular for their compact size, low running costs, and surprising interior space. The prompt specifically mentioned the Volkswagen UP! 1.0 Move up! Hatchback 5dr Petrol Manual Euro 5 (60 ps), which is a perfect example of what's achievable.

- Ford Fiesta / Vauxhall Corsa: Older generations of these popular superminis are frequently available. They offer a good balance of practicality, driving dynamics, and affordability.

- Toyota Aygo / Peugeot 107/108 / Citroën C1: Another trio of compact city cars, renowned for their reliability and incredibly low running costs, making them ideal for budget-conscious buyers.

- Hyundai i10 / Kia Picanto: These Korean city cars offer excellent value, often coming with generous equipment levels for their price point and known for their solid build quality.

It's important to be realistic. While you might find some excellent deals, don't expect a nearly new luxury saloon. Focus on cars that are mechanically sound, economical to run, and fit your daily needs.

Understanding Car Finance: Key Terms

To make an informed decision, you need to grasp the basics of car finance:

- Personal Contract Purchase (PCP): This is the most common form of car finance. You pay monthly instalments over a set term (e.g., 36 months). At the end of the term, you have three options: return the car, pay a final 'balloon payment' (Guaranteed Future Value or GFV) to own it, or use any equity as a deposit for a new car. PCP deals are popular because they offer lower monthly payments compared to Hire Purchase, as you're effectively only paying for the depreciation of the car during your usage period.

- Hire Purchase (HP): With HP, you pay monthly instalments over a set term, and once all payments (including an 'option to purchase' fee) are made, you own the car outright. Monthly payments are usually higher than PCP for the same car and term, as you're paying off the full value of the vehicle.

- Deposit: An upfront payment made at the start of the finance agreement. A larger deposit generally leads to lower monthly payments.

- Term: The duration of the finance agreement, typically expressed in months (e.g., 36, 48, 60 months). Longer terms can reduce monthly payments but often result in paying more overall interest.

- Annual Percentage Rate (APR): This is the total cost of borrowing, expressed as an annual percentage. It includes interest and any other charges. A lower APR means you pay less over the term of the loan. Your credit score significantly impacts the APR you're offered.

- Mileage Limit (PCP only): The maximum number of miles you're allowed to drive annually without incurring extra charges. Exceeding this limit will result in a per-mile fee, which can add up quickly. Be realistic about your driving habits.

Factors Affecting Your Monthly Payment

Several variables directly influence how much you'll pay each month:

- Vehicle Price: Naturally, a cheaper car will result in lower monthly payments. Focus on the total price of the car, not just the monthly figure.

- Deposit Amount: As mentioned, a larger upfront deposit reduces the amount you need to borrow, thus lowering your monthly payments. Even an extra few hundred pounds can make a noticeable difference.

- Loan Term: Stretching the repayment period over a longer term (e.g., 48 or 60 months instead of 36) will reduce your monthly outlay. However, be aware that you'll pay more interest over the longer period, increasing the total cost of the car.

- APR (Interest Rate): Your credit score plays a significant role here. Individuals with excellent credit scores will typically be offered lower APRs, leading to lower monthly payments. If your credit score is average or poor, you might be offered a higher APR, which will increase your monthly cost. It's advisable to check your credit score before applying for finance.

- Guaranteed Future Value (GFV) (PCP only): This is the predicted value of the car at the end of the PCP term. A higher GFV (meaning the car is expected to depreciate less) will result in lower monthly payments, as you're financing a smaller amount of depreciation.

Beyond the monthly finance payment, owning a car involves several other significant costs. Failing to budget for these can quickly turn an affordable car into a financial burden:

- Car Insurance: This is a mandatory and often substantial expense. Younger drivers, those with points on their license, or those living in high-risk areas will pay more. Always get insurance quotes *before* committing to a car purchase.

- Road Tax (Vehicle Excise Duty - VED): The amount you pay depends on the car's CO2 emissions (for cars registered before April 2017) or a flat rate (for cars registered after April 2017). Cheaper, smaller-engined cars often have lower road tax.

- Fuel: Even an economical car needs fuel. Consider your typical mileage and current fuel prices. A car under £100 a month is likely to be a petrol model, which can be more expensive at the pump than diesel, though diesel cars generally have higher purchase prices.

- Servicing and Maintenance: Cars need regular servicing to stay reliable and safe. Budget for annual services and be prepared for unexpected repairs, especially with older vehicles. A full service history can indicate a well-maintained car.

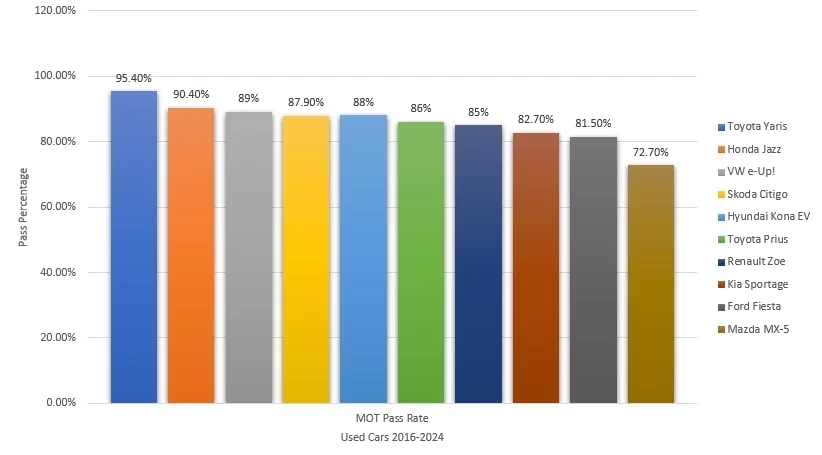

- MOT (Ministry of Transport) Test: Once a car is three years old, it requires an annual MOT test to ensure it meets road safety and environmental standards. Budget for the test fee and any necessary repairs to pass.

- Tyres and Consumables: Tyres wear out, as do brake pads, wiper blades, and other common parts. These are ongoing costs to factor into your budget.

Tips for Finding the Best Deal

- Check Your Credit Score: Before applying for finance, check your credit report with agencies like Experian, Equifax, or TransUnion. A good score improves your chances of securing a lower APR.

- Shop Around for Finance: Don't just accept the finance offered by the dealership. Get quotes from independent finance brokers and your bank or building society. You might find a better deal elsewhere.

- Be Realistic About Mileage: If considering PCP, accurately estimate your annual mileage. Over-estimating might lead to slightly higher monthly payments but avoids costly excess mileage charges. Under-estimating can be very expensive.

- Thoroughly Inspect the Vehicle: Always view the car in person. Check for bodywork damage, inspect the interior, and ensure all electrics work. If possible, take a knowledgeable friend or mechanic with you.

- Request a Test Drive: Drive the car on various road types to assess its handling, braking, and general performance. Listen for any unusual noises.

- Review Service History: A comprehensive service history indicates a car has been well-maintained. This is crucial for older vehicles.

- HPI Check: For peace of mind, consider performing an HPI check. This reveals if the car has been stolen, written off, has outstanding finance, or has been clocked (mileage altered).

- Negotiate: Don't be afraid to negotiate on the price of the car or the terms of the finance. Dealers often have some room for manoeuvre.

Pros and Cons of Low Monthly Payments

While attractive, low monthly payments come with their own set of advantages and disadvantages:

Pros:

- Affordability: Makes car ownership accessible to a wider range of budgets.

- Budget Management: Predictable monthly outgoings make it easier to manage your finances.

- Access to Newer Cars (PCP): PCP allows you to drive a newer car than you might otherwise afford, as you're not paying off the full value.

- Flexibility (PCP): At the end of a PCP term, you have options to suit your circumstances.

Cons:

- Higher Overall Cost (Longer Terms): While monthly payments are lower, you often pay more in total interest over a longer finance term.

- Mileage Restrictions (PCP): Overtight mileage limits can lead to significant charges if exceeded.

- Deposit Required: Most low-payment deals require an upfront deposit, which not everyone has readily available.

- No Ownership (PCP until balloon payment): With PCP, you don't own the car until the final balloon payment is made.

- Limited Choice: The range of vehicles available for under £100 a month will be narrower, typically focusing on smaller, older, or higher-mileage cars.

Comparative Table: How Finance Variables Impact Payments

This table illustrates how different finance structures can affect your estimated monthly payment for a hypothetical car valued at £5,000, assuming a representative APR of 9.9%:

| Deposit | Term (Months) | Estimated Monthly Payment (HP) | Estimated Monthly Payment (PCP)* |

|---|---|---|---|

| £500 | 36 | £145 | £110 |

| £1,000 | 36 | £130 | £95 |

| £500 | 48 | £115 | £85 |

| £1,000 | 48 | £100 | £70 |

| £1,500 | 48 | £85 | £60 |

| £1,000 | 60 | £85 | £55 |

*PCP payments are estimates and depend heavily on the car's GFV and mileage limit. These figures are illustrative and subject to change based on actual APR, specific car, and lender terms.

Frequently Asked Questions (FAQs)

Q: Can I get a brand new car for under £100 a month?

A: It's highly unlikely. New cars typically have higher list prices, meaning monthly payments will almost certainly exceed £100, even with a significant deposit or long term. The cars available in this budget are almost exclusively used vehicles.

Q: What if I have a poor credit score?

A: Getting finance with a poor credit score is more challenging and often comes with a higher APR, meaning higher monthly payments or a larger total cost. Some lenders specialise in subprime car finance, but it's crucial to understand the terms fully. Building your credit score before applying is advisable.

Q: What happens if I exceed the mileage limit on a PCP deal?

A: You will be charged an excess mileage fee, usually a few pence per mile, for every mile over your agreed limit. These charges can add up significantly, so it's vital to be realistic about your driving habits when setting your mileage allowance.

Q: Is it better to choose HP or PCP for a car under £100 a month?

A: It depends on your priorities. If you definitely want to own the car at the end and don't mind higher monthly payments, HP is suitable. If you prefer lower monthly payments and the flexibility to change cars regularly, PCP might be better, provided you're comfortable with the mileage limits and the balloon payment option.

Q: How important is the deposit?

A: The deposit is very important. A larger deposit directly reduces the amount of money you need to borrow, which in turn lowers your monthly payments. It can also sometimes help you secure a better APR.

Q: What's the oldest car I should consider?

A: There's no strict age limit, but generally, cars over 10-12 years old might start incurring more frequent and costly repairs. Focus more on the car's service history, mileage, and overall condition rather than just its age. Reputable dealerships will often only finance cars up to a certain age or mileage.

Q: Should I get a pre-purchase inspection?

A: For any used car, especially one at the lower end of the budget, a pre-purchase inspection by an independent mechanic is highly recommended. It can uncover hidden issues that might save you significant money and stress down the line.

Conclusion

Finding a car for under £100 a month in the UK is certainly achievable, but it requires a strategic approach. By understanding the nuances of car finance, being realistic about the types of vehicles available, and meticulously budgeting for all associated costs, you can make an informed decision that suits your financial situation. Remember to thoroughly research, compare deals, and always account for the hidden expenses that come with car ownership. With due diligence, you can successfully navigate the market and enjoy the freedom of affordable motoring without unexpected financial surprises.

If you want to read more articles similar to Affordable Wheels: Cars Under £100/Month UK, you can visit the Automotive category.