21/05/2018

Understanding PCP Car Finance: A Comprehensive Guide

The popularity of Personal Contract Purchase (PCP) car finance has surged in recent years, with approximately 80% of new and used car purchases in the UK utilising this method. While PCP can offer the allure of driving a better car for a lower monthly cost, it's crucial to understand the intricacies involved. Many buyers are unaware of the potential significant costs and penalties that can arise if they wish to end their agreement early or at its conclusion. This guide aims to cut through the jargon and help you make the most informed decision about whether PCP car finance is the right choice for you.

- What Exactly is PCP Car Finance?

- Should You Consider Buying a Car On PCP?

- How Does PCP Actually Work?

- Key Considerations and Potential Pitfalls

- Choosing the Right Contract Term

- Alternative Car Finance Options

- Buying Directly from Manufacturer PCP Offers

- Is PCP Suitable for Used Cars?

- What Happens When You Give a Car Back After PCP?

- Frequently Asked Questions

What Exactly is PCP Car Finance?

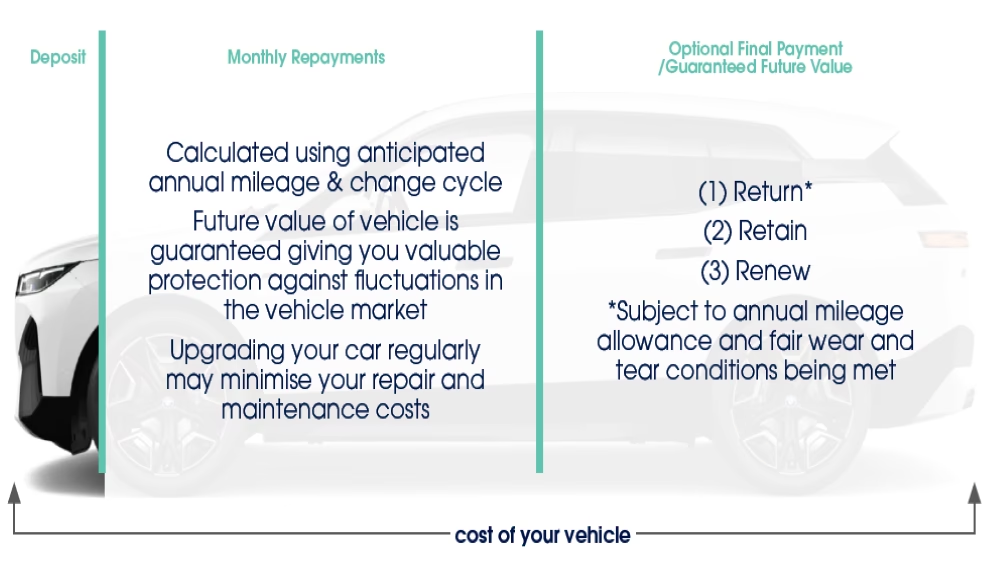

PCP, or Personal Contract Purchase, is a form of car finance that gained significant traction in the late 2000s. Its rise coincided with changes in how company cars were taxed, making it an attractive option for both small businesses and individual consumers. Essentially, PCP blends the concept of leasing a vehicle for personal use with the traditional hire-purchase model of buying a car through regular instalments.

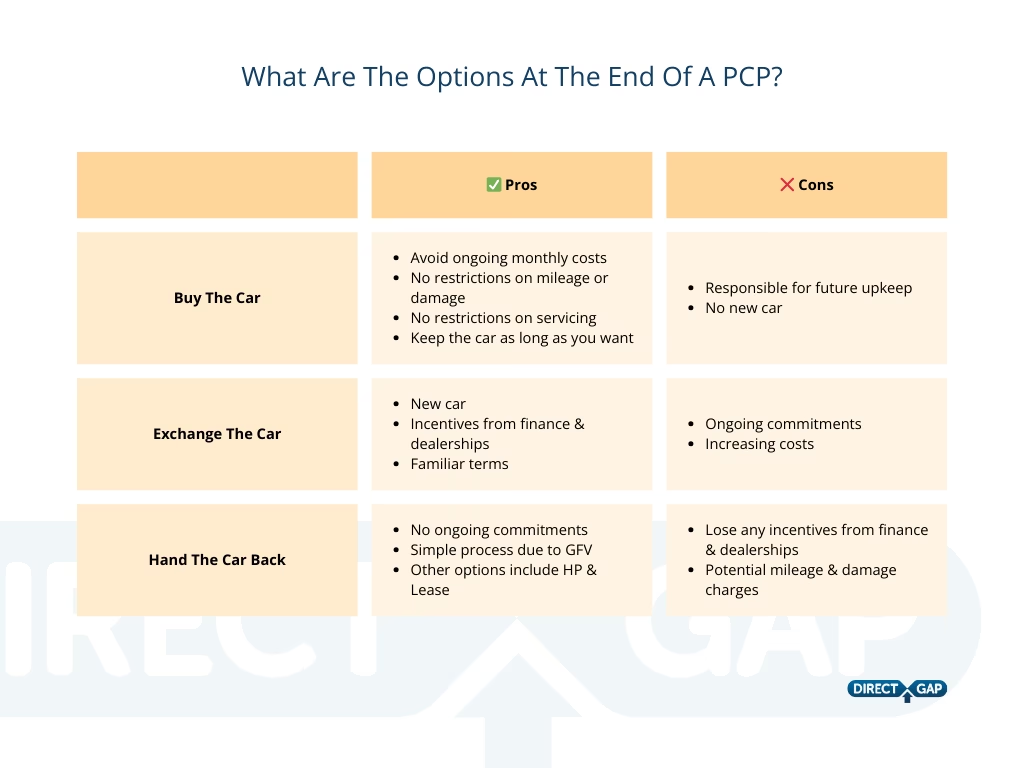

Instead of paying equal instalments to own your car outright over a set period, PCP involves an initial deposit followed by lower monthly payments. At the end of the contract term, you are presented with several options. You can choose to pay a final 'balloon' payment to own the car outright, hand it back without further obligation, sell it, or trade it in for a new vehicle. The decision to swap your car will depend on the Guaranteed Minimum Future Value (GMFV) that was established at the beginning of your PCP agreement.

The GMFV represents the lowest estimated value of your car at the end of the contract. While it's an estimate, if your car is worth more than the GMFV, you can utilise this equity as a deposit towards your next vehicle. Conversely, if its value is less than the GMFV, you can simply return the car. In the UK, a significant majority of PCP customers, around 80%, opt to return their cars at the end of their contract and sign up for a new deal, while the remaining 20% settle the final payment to own their current vehicle.

Should You Consider Buying a Car On PCP?

The decision to opt for PCP car finance is highly personal and depends on your individual circumstances and preferences. If your goal is to have a new car every few years, PCP can enable you to access a higher quality vehicle for a more manageable monthly outlay. This has been a significant factor in the increased popularity of premium brands and SUVs, even during economic downturns.

However, it's vital to adhere to the terms and conditions of your PCP agreement. These typically include mileage restrictions, adherence to the manufacturer's service schedule, and the requirement to repair any damage to the vehicle. Exceeding mileage limits can incur charges, often between 7-10 pence per mile, meaning an extra 1,000 miles could cost you an additional £100. It's also wise to confirm whether essential costs like car tax are included for the duration of your contract to avoid unexpected payments at the end.

If your ultimate aim is to own your car outright at the end of any finance agreement, PCP might not be the most suitable option. The GMFV, set at the outset, can result in a substantial final payment. Your financial situation or the car's actual value might have changed significantly by then, potentially making this final payment unmanageable.

To mitigate these risks, consider using services that allow you to sell your car and settle any outstanding finance, potentially putting more money back in your pocket.

How Does PCP Actually Work?

A typical PCP car finance deal shares similarities with traditional hire purchase or vehicle leasing agreements, with the key addition of the final balloon payment option if you wish to keep the car. The three core components of a PCP agreement are:

- The Deposit: This is the upfront payment you make to initiate the PCP deal.

- The Loan Amount: This is the sum you borrow and repay through monthly instalments over the contract period.

- The Final Payment (GMFV): This is the amount you pay at the end of the contract to take ownership of the car.

An Example PCP Contract

Let's illustrate with a hypothetical £20,000 PCP car finance deal for a car estimated to be worth £10,000 after five years:

- Your Deposit: A 10% deposit would be £2,000, paid before any manufacturer contributions.

- The Loan Amount: You would borrow and repay £8,000 plus interest. Assuming a 5% APR over 60 months, the total interest paid would be approximately £1,033.79, resulting in monthly payments of around £150.56. The total repayment for the loan amount would be £11,033.79.

- The Final Payment: The GMFV would be £10,000, plus any applicable interest. You might also incur an 'option to purchase fee' of around £150 to cover the transfer of ownership.

Understanding APR Rates

APR (Annual Percentage Rate) rates are influenced by the UK's economic climate and financial markets, and the rate you are offered is a reflection of your creditworthiness. Shopping around for 0% APR deals, making larger deposits, and taking advantage of manufacturer contributions can potentially lead to significant savings.

A typical low APR might be around 5.5%, meaning a £10,000 loan could cost approximately £11,423.63 in repayments over 60 months. A moderate APR of 14.9% would increase the total cost of a £10,000 loan to around £13,951.59. At a higher APR of 20.9%, the total repayment for the same loan could reach £15,607.36. This highlights the critical importance of thorough research when selecting a PCP deal.

Key Considerations and Potential Pitfalls

When evaluating PCP car finance deals, several factors require careful attention:

- The Deposit Amount: Investigate whether manufacturers offer 'deposit contributions' as part of their finance packages. These can range from £500 to £2,000 or more and can significantly reduce your overall cost. A larger personal deposit can also be beneficial.

- The APR Rate: Scrutinise the interest charged on both the loan amount and the final balloon payment. While a low APR can seem appealing, ensure that the dealer isn't recouping costs through a higher initial deposit or final payment. Typical APRs can vary widely, from 5% to over 20%, especially for used cars.

- The Final GMFV Amount: Assess the realism of the car's projected final value. Used car values can fluctuate, and a significant drop could leave you out of pocket if you intend to buy the car. If you're switching to a new PCP deal, a higher-than-expected car value can provide valuable equity for your next purchase, but a lower value can mean a financial loss. Remember that the final payment often includes interest and an administration fee.

- Agreement Conditions: Be mindful of mileage limits and the condition requirements for returning the car. Exceeding mileage, failing to adhere to the service schedule, or neglecting necessary repairs can lead to substantial charges at the end of the contract.

- Insurance Implications: Standard car insurance typically pays out the agreed value of the car at the time of theft or write-off. In a PCP deal, this might not cover the outstanding finance amount, leaving you in a deficit. Consider 'Gap Insurance,' which can bridge this shortfall by covering the difference between the car's market value and the amount owed on finance.

Choosing the Right Contract Term

The optimal length for your PCP agreement depends on your personal circumstances. Most contracts range from 36 to 60 months. Generally, a longer term results in lower monthly payments. However, it's important to remember that ending a PCP deal early can incur additional costs.

A three-year contract offers advantages such as exempting you from MOT tests during the initial period and keeping you within the manufacturer's warranty, potentially reducing repair costs. However, longer terms mean more can change during the agreement, including used car values, making predictions more challenging, especially for used vehicles.

Alternative Car Finance Options

PCP is not the only avenue for financing a car. Traditional options like hire purchase, personal car loans, and leasing can sometimes offer more cost-effective solutions, whether or not you intend to own the car at the end of the agreement.

- Personal Car Loans: Available from banks and building societies, these offer simplicity, immediate ownership, and often lower interest rates over 1-7 years. The downsides include potentially higher monthly payments and the fact that you don't benefit from depreciation.

- Hire Purchase (HP): While less popular than PCP, HP is still used by many car buyers. The primary benefit is outright ownership at the end of the agreement with no large final payment. Monthly costs are higher to reflect the full purchase price. Until the final payment is made, you are legally hiring the car and it can be repossessed if payments are missed.

- Leasing: Primarily aimed at businesses, leasing involves long-term car rental. Mileage and damage costs can be higher than with PCP, and gap insurance may be necessary. For private owners, it can be a reasonable option for accessing higher-end vehicles that hold their value, but the total cost can approach that of buying the car outright, especially for lower-value models.

Buying Directly from Manufacturer PCP Offers

Manufacturer PCP offers can be very attractive, often featuring subsidised 0% finance or substantial deposit contributions. They may also include additional incentives like upgrades or higher specifications. However, these deals can sometimes tie you to a specific manufacturer. If you have a negative experience or simply wish to switch brands, you might incur greater costs when returning the car or ending the agreement.

Is PCP Suitable for Used Cars?

While initially focused on new, premium vehicles, PCP deals are now widely available for used cars. Factors such as slowing new car sales, strong used car values, and low-interest rates can make buying a nearly-new used car on PCP more affordable than an older car purchased outright. A key advantage of PCP for used cars is lower monthly payments, as the steepest depreciation has already occurred, meaning the car retains more of its value throughout the agreement.

However, sourcing older vehicles on PCP can be more challenging as car values become less predictable after about eight years. Increased wear and tear can also lead to higher maintenance costs, which must be factored in alongside the agreement's terms.

What Happens When You Give a Car Back After PCP?

When you return a car at the end of a PCP agreement, the primary factor is the GMFV. If the car's actual market value meets or exceeds the GMFV, you can simply hand it back without further financial obligation (assuming you've met all contractual terms). If the car's value is higher than the GMFV, you can use the 'equity' (the difference) as a deposit for a new car. If the car's value is less than the GMFV, you would typically need to pay the difference to settle the finance, unless you choose to trade it in for a new vehicle where the dealer might absorb some of the shortfall.

Frequently Asked Questions

Q1: Can I end my PCP agreement early?

Yes, you can usually end a PCP agreement early, typically after you have paid half of the total amount due (including the GMFV). This is known as voluntary termination. However, there may be penalties or fees associated with early termination, so it's essential to check your contract terms.

Q2: What if I exceed the mileage limit on my PCP?

Exceeding the agreed mileage limit will result in charges, usually calculated per mile over the limit. These charges can add up significantly, so it's crucial to be realistic about your annual mileage when setting up the contract.

Q3: Do I need to get my car serviced at a main dealer with PCP?

While PCP agreements often stipulate adherence to the manufacturer's service schedule, it doesn't always mean you must use a main dealer. However, using an independent garage that follows the manufacturer's servicing guidelines is generally acceptable. Check your contract for specific requirements.

Q4: What happens if my car is written off during a PCP agreement?

If your car is written off, your standard car insurance will pay out its market value. If this amount is less than the outstanding finance (including the GMFV), you will be liable for the difference. This is where gap insurance becomes particularly valuable.

Q5: Can I buy the car at the end of the PCP term?

Yes, you have the option to buy the car by paying the GMFV (plus any final fees). This is one of the primary benefits of PCP, offering flexibility in how you conclude the agreement.

If you want to read more articles similar to PCP Car Finance: Your Options Explained, you can visit the Automotive category.