18/08/2022

Navigating the world of car finance can often feel like a complex maze, particularly when it comes to understanding your rights as a consumer. Whether you're considering a Hire Purchase (HP) agreement or a Personal Contract Purchase (PCP), knowing where you stand if things go wrong is paramount. For years, advisors and consumers alike have grappled with the intricacies of vehicle purchases and their associated finance, especially when issues arise post-sale. This article aims to shed light on these matters, offering clarity and empowering you with the knowledge to protect your interests.

- The 'Linked Transaction' Principle with HP Finance

- The Consumer Rights Act and Your Recourse

- Proactive Dealership Practices

- Understanding Section 75 of the Consumer Credit Act

- The Role of the Financial Ombudsman Service (FOS)

- Personal Contract Purchase (PCP) Explained

- Key Takeaways for Consumers

- Frequently Asked Questions

The 'Linked Transaction' Principle with HP Finance

Historically, when you purchase a vehicle and finance it using a Hire Purchase (HP) agreement, the transaction is considered a 'linked transaction'. This classification historically placed an obligation on both the supplier (the dealership) and the finance provider. Essentially, if the car you bought developed a fault that could be proven to have existed at the time of sale, both parties could be held jointly liable. This principle isn't exclusive to vehicles; it applies to any goods purchased through such a linked finance arrangement. It was not uncommon for consumers, when faced with a faulty vehicle, to be incorrectly directed by the finance company back to the dealer, with the finance provider claiming the supplier was solely responsible.

However, as experience and guidance from bodies like the Financial Ombudsman Service (FOS) have shown, this isn't always the case. Consumer rights are robust, and the finance company often bears significant responsibility. Imagine a scenario where a car is advertised with, and even confirmed by the salesman to have, six forward gears. Upon delivery, you discover it only has five. Under the 'not as described' clause, you have grounds to reject the car. Crucially, the HP company remains liable, even if they weren't directly involved in the sales negotiation. This might seem counterintuitive, but it underscores the strength of consumer protection in these linked transactions.

The Consumer Rights Act and Your Recourse

Recent clarifications, while aiming to simplify matters, have also introduced nuances. Some legal interpretations suggest a clearer process: the consumer inspects and agrees to the car, then takes out HP or PCP finance. The car is then invoiced to the lender, making the lender the legal owner. The transaction between the lender and the dealer is viewed as a commercial one, not directly governed by the Consumer Rights Act in the same way. Your rights under the Act, in this interpretation, are primarily between you and the lender.

Therefore, if the goods (the car) are faulty, not fit for purpose, or not as described, your case lies against the lender. It's vital not to be deflected back to the supplying dealer; this is the lender's responsibility to resolve. Many lenders, keen to avoid prolonged disputes and potential reputational damage, are opting to unwind the finance, take back the car, and then compel the dealer to repurchase it, often by threatening to withdraw credit facilities. This process, while potentially beneficial for the consumer in getting their money back and returning the vehicle, can lead to disputes between dealers and lenders. Some legal firms advise dealers to challenge these situations, though from the consumer's perspective, the goal is a resolution, which is often achieved by returning the car and obtaining a refund.

Proactive Dealership Practices

To mitigate such issues, some dealerships are adopting more proactive approaches. Rather than strictly adhering to legal minimums, they might offer assurances like, "We value our customers and our cars; if you encounter any problems within the first six months, please let us know, and we'll strive for a satisfactory resolution." While not a legal obligation, such statements can foster goodwill and help avoid costly disputes stemming from faulty vehicles.

Understanding Section 75 of the Consumer Credit Act

A key piece of legislation to be aware of is Section 75 of the Consumer Credit Act 1974. This section provides significant protection for consumers entering into agreements for goods or services costing between £100 and £30,000 where the finance is provided by the supplier as part of the purchase. In such cases, both the supplier and the finance provider are jointly and severally liable for any breach of contract or misrepresentation. This means if the goods are faulty or not as described, you can claim against either the dealer or the finance company.

When Does Section 75 Apply?

- The purchase price must be between £100 and £30,000.

- The finance must be a 'linked transaction' arranged by the dealer at the point of sale. This typically applies to fixed-sum loans.

When Does Section 75 NOT Apply?

- If you arrange finance independently from a bank or building society, it is not considered a linked transaction, and Section 75 protection does not apply.

- Crucially, and perhaps surprisingly to many, Hire Purchase (HP) agreements do not fall under Section 75. The Financial Ombudsman Service clarifies that HP agreements are consumer credit contracts that give the consumer the right, but not the obligation, to buy the goods at the end of the term. Section 75 does not apply to these.

The Role of the Financial Ombudsman Service (FOS)

Despite the complexities and the specific exclusions, the FOS remains a vital resource for consumers. Even when specific legislation like Section 75 doesn't directly apply, the FOS will consider claims from consumers regarding faulty goods, goods not fit for purpose, or goods not as described. Their approach is often sympathetic to consumers, and their services are free of charge. While the FOS has limits on the compensation they can award, their findings can be instrumental in resolving disputes. Furthermore, if you remain unsatisfied with the FOS's decision, you retain the right to pursue legal action against the company concerned, particularly if you believe significant damages are warranted.

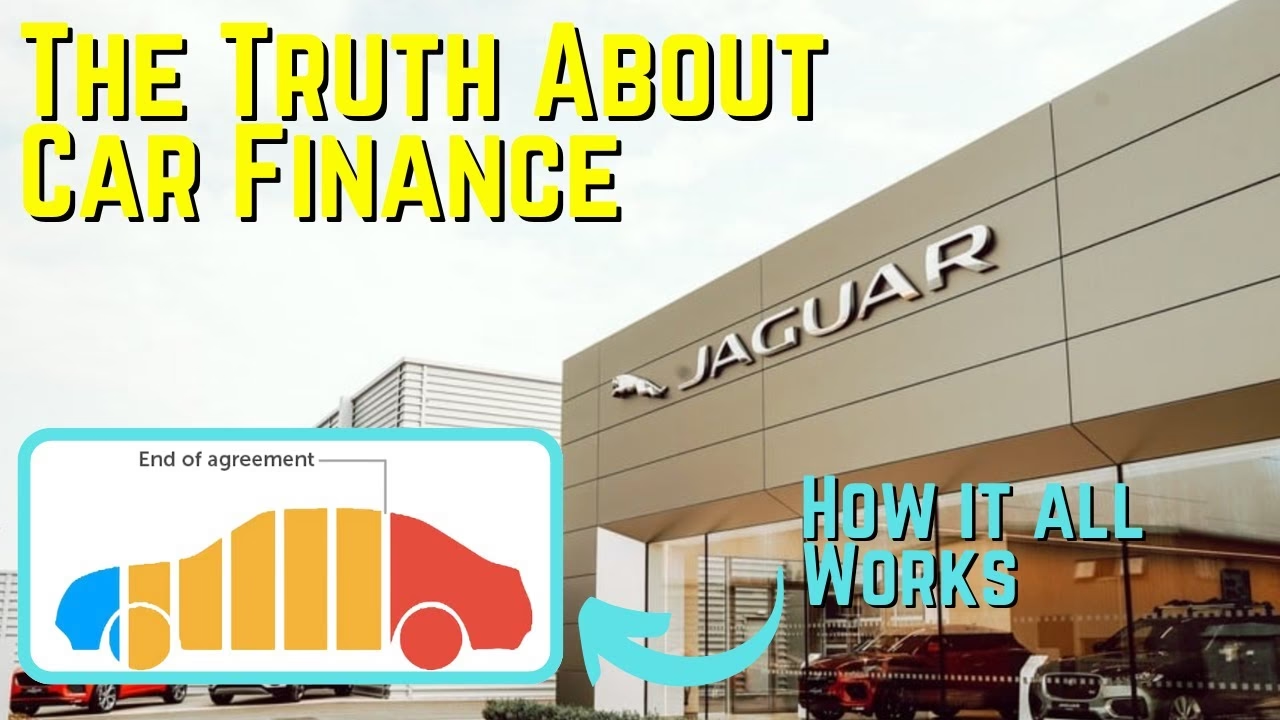

Personal Contract Purchase (PCP) Explained

While the provided text focuses heavily on HP agreements and Section 75, it's important to briefly touch upon PCP. A PCP agreement is a loan for a car, but with a difference. You pay monthly instalments towards the car's depreciation, rather than its full value. At the end of the contract, you have options: pay a Guaranteed Future Value (GFV) lump sum to own the car outright, return the car with no further payments (subject to mileage and condition clauses), or part-exchange the car for a new one.

The 'linked transaction' principle and consumer rights under the Consumer Rights Act generally still apply to PCP agreements in a similar fashion to HP, meaning that if the car is faulty, not as described, or not fit for purpose, you have recourse against the finance provider. The complexities arise with the GFV and the conditions attached to returning the car. Understanding these terms is crucial before signing.

Key Takeaways for Consumers

- Know Your Rights: Familiarise yourself with the Consumer Rights Act 2015 and, where applicable, Section 75 of the Consumer Credit Act 1974.

- Linked Transactions: Understand that finance arranged at the point of sale is often a 'linked transaction', giving you recourse against both the dealer and the finance provider in certain circumstances.

- HP vs. Section 75: Be aware that HP agreements, despite being linked transactions, are not covered by Section 75.

- Lender Liability: If your car is faulty, your primary recourse for issues not covered by Section 75 might be directly with the finance company.

- Use the FOS: The Financial Ombudsman Service is a valuable, free resource for resolving disputes with financial institutions.

- PCP Nuances: Understand all terms and conditions of PCP agreements, especially the GFV and return conditions.

- Don't Be Afraid to Exercise Your Rights: If you believe you have a valid claim, pursue it confidently.

Frequently Asked Questions

Q1: If my car has a fault, can I always reject it?

A1: You can reject a car if it is faulty, not as described, or not fit for purpose within a reasonable time, especially if the fault existed at the time of purchase. Your rights are strongest within the first 30 days, but extend beyond that, particularly if the issue is a breach of contract.

Q2: Am I protected by Section 75 if I bought my car using a PCP deal?

A2: Section 75 generally applies to 'credit agreements' that are fixed-sum loans. PCP agreements are typically structured as hire agreements with an option to purchase. While the 'linked transaction' principle often still applies, giving you rights against the finance provider, PCP deals themselves are not usually covered by Section 75 in the same way as a standard loan.

Q3: What happens if my dealer goes out of business?

A3: If your dealer goes out of business and you have a linked HP or PCP agreement, your finance agreement remains valid. The finance company is still obliged to provide the vehicle or a suitable alternative, and you should continue to make your payments to the finance provider. If the car is faulty, your recourse is still with the finance provider.

Q4: Can I cancel my car finance agreement?

A4: Under the Consumer Credit Act, you have a 'cooling-off' period (usually 14 days) during which you can cancel most credit agreements, including car finance, without giving a reason. After this period, cancellation becomes more complex and may involve early settlement fees.

Q5: What is the difference between HP and PCP?

A5: With HP, you pay off the full value of the car over the agreement term, and you own it at the end. With PCP, you pay off the depreciation of the car, making monthly payments lower. At the end of a PCP, you have the option to buy the car for a pre-agreed amount (GFV), return it, or part-exchange it.

By understanding these principles and knowing your rights, you can approach car finance agreements with greater confidence, ensuring you are well-equipped to handle any issues that may arise.

If you want to read more articles similar to Understanding Car Finance: Your Rights, you can visit the Automotive category.