23/12/2021

That dreaded moment when your beloved vehicle presents you with an eye-watering repair bill can feel like a punch to the gut. Immediately, the mind races: should I just bite the bullet and pay for the fix, or is this the universe telling me it’s time for a shiny new set of wheels? This isn't just a financial decision; it's a complex interplay of practicality, emotion, and future planning. Navigating this crossroads requires a clear head and a methodical approach, weighing up the pros and cons of keeping your current car on the road versus embracing the often significant financial commitment of a new acquisition.

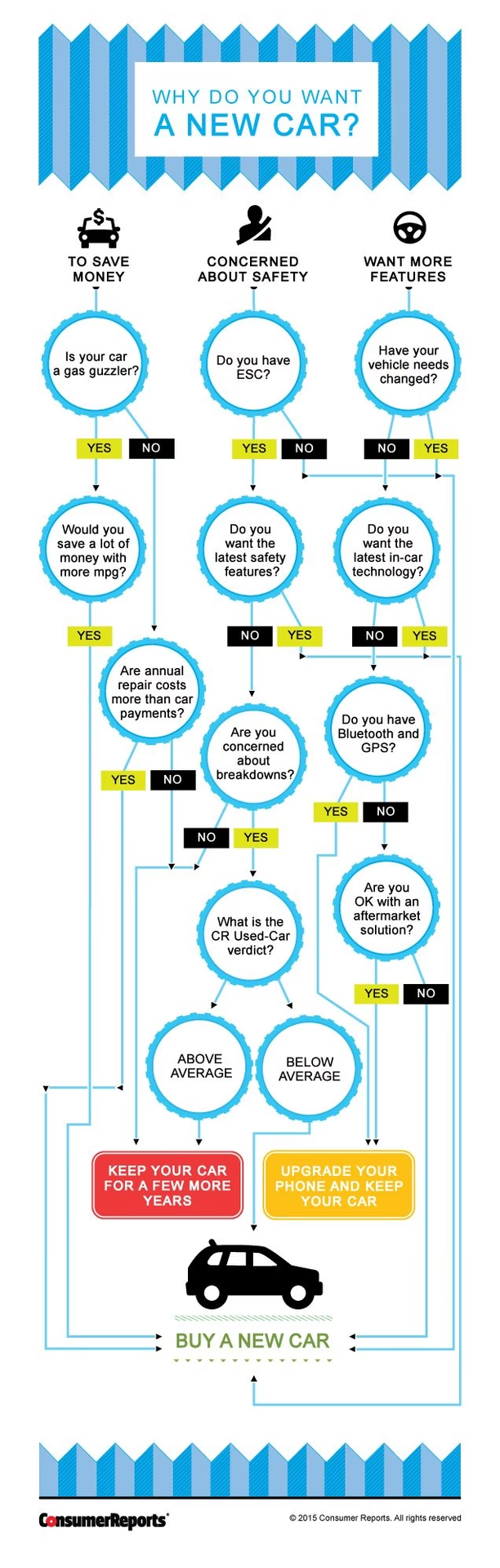

- The Great Debate: Repair or Replace?

- Assessing the Repair Cost vs. Vehicle Value

- Considering Your Current Car's Reliability and Age

- The Financial Implications: Repair vs. New Car Loan

- Table: Repair vs. New Car vs. Used Car (Alternative)

- The 'Total Cost of Ownership' Perspective

- Emotional Attachment and Practicality

- What About a Quality Used Car as an Alternative?

- Frequently Asked Questions (FAQs)

- Q1: What is the '50% Rule' and should I always follow it?

- Q2: How can I accurately estimate future repair costs for my current car?

- Q3: Should I get multiple quotes for the repair?

- Q4: How does car insurance factor into this decision?

- Q5: What if I can't afford either a major repair or a new car?

- Q6: How does depreciation affect my decision to buy new?

- Making Your Decision

The Great Debate: Repair or Replace?

It’s a question as old as motoring itself. When a significant component fails – perhaps the gearbox, engine, or a complex electrical system – the cost can easily run into thousands of pounds. At this point, many drivers automatically consider a new car, assuming it’s the only sensible option. However, this knee-jerk reaction can sometimes lead to a more expensive outcome in the long run. Before you sign on the dotted line for a new car loan, let's delve into the critical factors that should influence your decision.

Assessing the Repair Cost vs. Vehicle Value

One of the most widely cited pieces of advice, often echoed by automotive experts like those at Kelley Blue Book, suggests that if a repair is only a few hundred pounds, it's almost always sensible to fix it. The real dilemma arises when the repair bill starts to creep up, perhaps equalling or exceeding a significant percentage of your car's current market value. A common rule of thumb often bandied about in the industry is the '50% Rule': if the repair cost is more than 50% of the car's current value, or if the annual repair costs exceed the car's value, it might be time to consider moving on. For instance, if your car is worth £4,000 and the repair bill is £2,500, that's over 60% of its value, making a strong case for replacement.

To accurately determine your car's market value, consult reliable online valuation tools or reputable dealerships. Remember to factor in its condition, mileage, and service history. Getting multiple quotes for the repair is also crucial; prices can vary significantly between garages.

Considering Your Current Car's Reliability and Age

How old is your car, and what's its general reliability track record? If your vehicle is relatively young (say, under 5-7 years old) and has generally been dependable, an isolated major repair might just be an unfortunate blip. Modern cars are built to last, and a single costly repair doesn't necessarily mean a cascade of future problems. However, if your car is older, has high mileage, and has been plagued by frequent, increasingly expensive repairs, then this latest bill could be the final straw. An engine replacement on a 15-year-old car with 150,000 miles, for example, is far less justifiable than on a 5-year-old car with 50,000 miles.

Think about the car's maintenance history. Has it been regularly serviced? Have preventative measures been taken? A well-maintained older car can often surprise you with its longevity. Conversely, a car that has been neglected is more likely to present ongoing issues.

The Financial Implications: Repair vs. New Car Loan

This is where the numbers game gets serious. Let's compare:

- Cost of Repair: A one-off payment, however large, might still be less than the total cost of a new car over its lifetime, especially when you factor in depreciation.

- New Car Loan: This involves monthly payments, potentially for several years, plus interest. New cars also suffer from rapid depreciation – a significant loss in value the moment you drive them off the forecourt. This hidden cost is often overlooked but can be substantial.

- Insurance: New cars often have higher insurance premiums due to their higher value and the cost of parts.

- Road Tax & Fuel Efficiency: Newer cars generally boast better fuel economy and lower emissions, which can translate to cheaper road tax and lower running costs over time. This is a benefit to factor into your long-term calculations.

Consider your personal financial situation. Do you have savings to cover the repair without jeopardising your financial stability? Or would taking out a new car loan stretch your budget too thin? Remember that current market conditions for new cars might mean record-high prices, as mentioned in the prompt's context, making the decision even more complex.

Table: Repair vs. New Car vs. Used Car (Alternative)

| Factor | Repair Current Car | Buy New Car | Buy Quality Used Car |

|---|---|---|---|

| Initial Cost | One-off repair bill | High purchase price + loan interest | Lower purchase price + potential loan interest |

| Depreciation | Minimal if car is already old | Significant, especially in first 3 years | Less rapid than new, some already occurred |

| Reliability | Variable; depends on repair quality & car's overall health | High (warranty protection) | Good if researched well (e.g., approved used) |

| Warranty | None for existing components; repair might have limited warranty | Comprehensive manufacturer warranty | Often limited dealer warranty or none |

| Features/Tech | No upgrade | Latest safety, infotainment, efficiency tech | Potentially more modern than current car, but not cutting-edge |

| Running Costs | Potentially higher if other parts fail; fuel efficiency is static | Potentially lower fuel, tax, insurance initially | Variable; depends on age/model |

| Peace of Mind | Uncertainty about future repairs | High (new car smell, no immediate worries) | Reasonable if purchased from reputable source |

| Environmental Impact | Lower (extending vehicle life) | Higher (manufacturing new vehicle) | Lower (extending vehicle life) |

The 'Total Cost of Ownership' Perspective

Beyond the initial outlay, consider the total cost of ownership. This includes fuel, insurance, road tax, servicing, and potential future repairs. A new, more fuel-efficient car might save you money at the petrol pump, and lower emissions could mean cheaper road tax. However, the initial depreciation hit on a new car often outweighs these savings in the first few years. An older, repaired car, while perhaps not as efficient, has already absorbed most of its depreciation, making its 'true' running cost potentially lower.

Emotional Attachment and Practicality

Sometimes, the decision isn't purely financial. You might have an emotional attachment to your car, or it might perfectly suit your lifestyle (e.g., a large family car, a workhorse van). Replacing it with something similar could be difficult or more expensive than anticipated. On the other hand, a new car might offer features you genuinely need, such as improved safety systems, better fuel economy, or more space for a growing family. Don't underestimate the value of peace of mind that comes with a new car and its comprehensive warranty.

What About a Quality Used Car as an Alternative?

If buying a brand-new car feels too much of a stretch, and repairing your current vehicle seems like throwing good money after bad, consider a quality used car. This option often provides a middle ground, allowing you to upgrade to a more modern, reliable vehicle without incurring the significant depreciation of a brand-new model. Look for 'approved used' schemes from manufacturers, which often come with a warranty and a thorough inspection, offering a good balance of value and reliability.

Frequently Asked Questions (FAQs)

Q1: What is the '50% Rule' and should I always follow it?

The '50% Rule' suggests that if a repair costs more than 50% of your car's current market value, it's often more sensible to replace the car. While a useful guideline, it's not a strict rule. Factors like your car's overall condition, future reliability prospects, and your financial situation should also be considered. For a car you love and know well, a slightly higher percentage might be acceptable.

Q2: How can I accurately estimate future repair costs for my current car?

This is challenging but not impossible. Review your car's service history for recurring issues. Research common problems for your specific make and model as it ages. Consult a trusted mechanic for an honest assessment of potential future major repairs. While no one has a crystal ball, an informed guess is better than none.

Q3: Should I get multiple quotes for the repair?

Absolutely, yes. Repair costs can vary significantly between independent garages and main dealerships. Obtain at least two or three detailed quotes, ensuring they specify exactly what work will be done and what parts will be used. This can save you a substantial amount of money and give you a clearer picture of the repair's true cost.

Q4: How does car insurance factor into this decision?

A new car will almost certainly lead to higher insurance premiums due to its greater value. Your existing car, if repaired, will likely maintain its current insurance cost, assuming no major changes to its value or your driving history. Also, consider if the repair is due to an accident – your insurance might cover it, potentially making the repair option more attractive.

Q5: What if I can't afford either a major repair or a new car?

This is a tough situation. Explore financing options for the repair, if available, or consider selling your car 'as seen' for parts or to a specialist who might fix it cheaper. Public transport, car-sharing, or a much cheaper, older used car might be temporary solutions until your financial situation improves. Don't let a breakdown lead you into unmanageable debt.

Q6: How does depreciation affect my decision to buy new?

Depreciation is the silent killer of value. New cars lose a significant percentage of their value (often 15-20%) in the first year alone, and continue to depreciate rapidly for the first three years. This means a substantial portion of your monthly loan payment is effectively paying for a loss in value. An older car, even with a major repair, has already undergone most of its depreciation, making the cost of keeping it potentially more cost-effective in the long run from a depreciation standpoint.

Making Your Decision

Ultimately, the decision to repair or replace your car when faced with a hefty bill is deeply personal and depends on a multitude of factors. There's no single right answer for everyone. Take the time to crunch the numbers carefully, consider the future cost-effectiveness of your current vehicle, and be honest about your financial capabilities and motoring needs. Don't be swayed by emotion or the allure of a new car smell without first doing your homework. By thoroughly evaluating your options, you can make an informed choice that keeps you safely and affordably on the road for years to come.

If you want to read more articles similar to Fix It or Flick It: Your Car Dilemma, you can visit the Automotive category.