26/04/2001

Understanding if Your Car is a Write-Off

It's a dreaded moment for any car owner: the possibility that their beloved vehicle has been deemed a 'write-off'. This term, often used by insurance companies, signifies that the cost to repair your car after an accident or damage exceeds its market value. It's a complex process, and understanding the criteria can help you navigate the situation. This article will delve into what constitutes a write-off, the different categories, how insurance companies make their decisions, and what your options are.

What Exactly is a 'Write-Off'?

A car write-off, also known as a total loss, occurs when the expense of repairing the vehicle to a roadworthy condition is more than the car's pre-accident value. This valuation is typically based on the market price of a similar vehicle just before the incident. Insurance companies use this as a benchmark to decide whether to repair the car or pay out its value. It's not solely about the severity of the visible damage; internal structural damage or even extensive water ingress can also lead to a write-off, even if the car appears superficially intact.

The Two Categories of Write-Offs

Insurance companies classify write-offs into two main categories:

Category A: Scrapped Vehicles

Vehicles in Category A are so severely damaged that they must be scrapped. This means they cannot be repaired and must be dismantled for parts, with the shell crushed. Examples of damage that would typically fall into this category include:

- Major structural damage (e.g., chassis severely compromised).

- Extensive fire damage.

- Significant flood damage where the vehicle has been submerged.

- Damage from severe accidents that render the car irreparable.

Category A vehicles are never allowed back on the road. Any parts salvaged must be destroyed, not reused.

Category B: Repairable, But Not Economically Viable

In Category B, the car is also deemed a write-off, but it's not as catastrophic as Category A. These vehicles have sustained significant damage, but some parts may be salvageable. The vehicle itself cannot be repaired and put back on the road, but its usable parts can be removed and sold. The remaining shell must still be scrapped. Common reasons for a Category B write-off include:

- Moderate to severe accident damage, but not compromising the entire structure.

- Damage that would cost more to repair than the car's value, but the vehicle isn't a total write-off in terms of structural integrity.

- Damage that might not be immediately obvious but is extensive, such as significant electrical system damage.

The key difference is that while the car as a whole is a write-off, certain components might be deemed safe and reusable by authorised dismantlers.

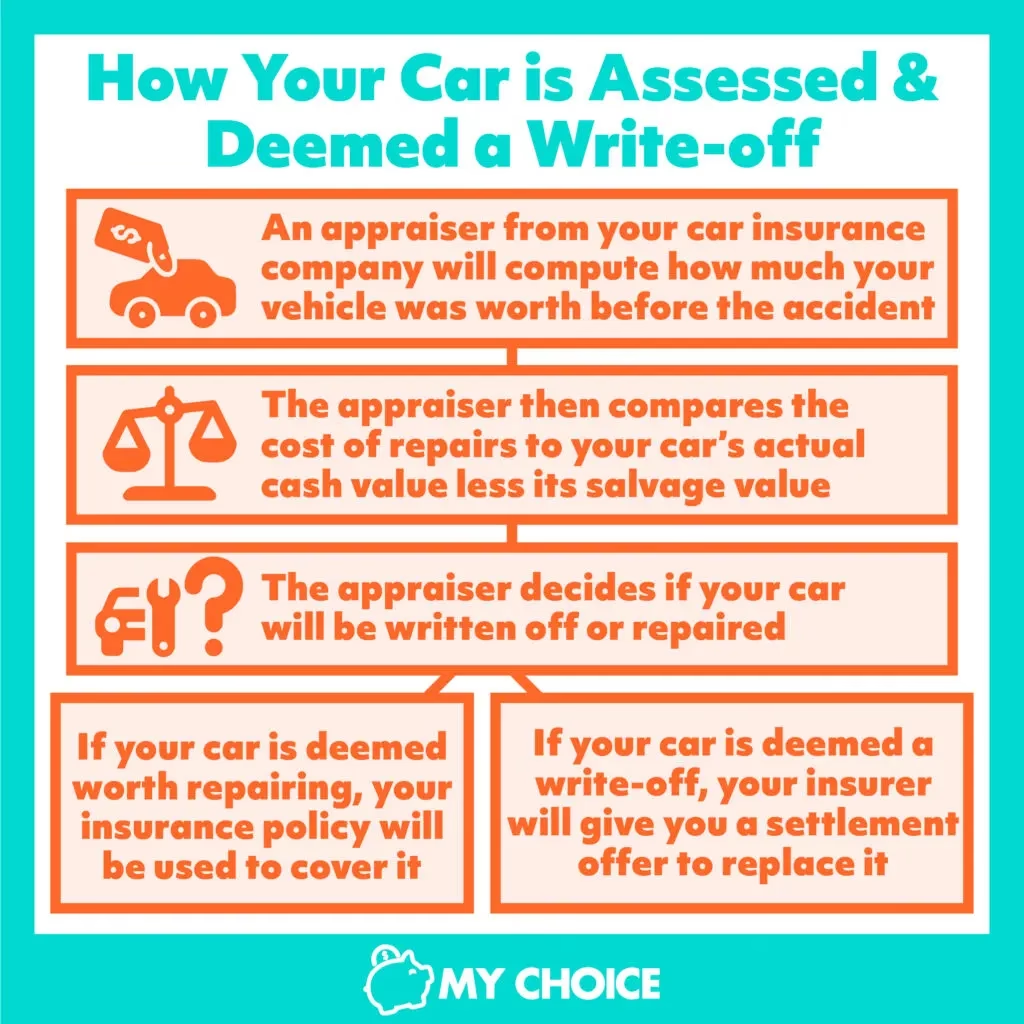

How Insurance Companies Determine a Write-Off

The process usually begins after an accident or incident that damages your vehicle. Your insurance company will typically:

- Initial Assessment: An assessor will inspect the damage. This might be a physical inspection or, increasingly, a virtual assessment using photos and videos.

- Repair Estimate: They will obtain quotes from repairers to bring the car back to its pre-accident condition.

- Valuation: Simultaneously, they will determine the car's pre-accident market value. This involves researching the value of similar cars in similar condition, mileage, and age in your local area. They will consider factors like service history, MOT status, and any modifications.

Factor Impact on Valuation Age Older cars generally have lower values. Mileage Higher mileage typically reduces value. Condition Excellent condition increases value; wear and tear decreases it. Service History A comprehensive service history can boost value. Modifications Some modifications can increase value, others decrease it. - The 75% Rule (Common Guideline): While not a strict law, many insurers use a common guideline where if the repair costs exceed approximately 75% of the car's pre-accident value, they will likely declare it a write-off. This percentage can vary between insurers.

- Decision: If the repair costs are higher than the car's value (or the insurer's threshold), it will be classified as a write-off.

What Happens If Your Car is Declared a Write-Off?

Once your car is declared a write-off, you have a few options:

1. Accept the Insurance Payout

This is the most common outcome. The insurance company will offer you a settlement amount based on the car's pre-accident value. You will then need to hand over the vehicle to the insurer. They will usually arrange for it to be collected. You'll need to provide your V5C registration document (logbook) to them.

2. Keep the Written-Off Vehicle (Salvage)

In some cases, particularly with Category B write-offs, you may be allowed to keep the vehicle. If you choose this option, you will receive a payout from the insurer that is the car's market value minus its salvage value (what the insurer would get for selling the damaged car for parts). However, it's crucial to understand the implications:

- Category A: You cannot keep these vehicles.

- Category B: If you keep a Category B vehicle, you must ensure it is dismantled by an Authorised Treatment Facility (ATF). You will receive a Certificate of Destruction. You will also need to inform the DVLA that the vehicle has been scrapped. You cannot legally repair and drive a Category B vehicle.

It's important to note that keeping a written-off vehicle can significantly impact future insurance premiums, and you will need to prove it has been properly dismantled if it was Category B.

3. Challenge the Valuation

If you believe the insurance company's valuation of your car is too low, you have the right to challenge it. Gather evidence such as advertisements for similar vehicles, your car's service history, and details of any recent upgrades or modifications. You can negotiate with the insurer. If you still cannot agree, you can escalate the matter to the Financial Ombudsman Service.

Signs Your Car Might Be a Write-Off

While the final decision rests with the insurer, certain signs can indicate your car is likely to be a write-off:

- Extensive visible damage: Significant crumpling of the bodywork, especially in structural areas like the chassis, suspension mounting points, or A-pillars.

- Multiple airbags deployed: This indicates a significant impact and can lead to costly sensor and system replacements.

- Flood damage: If the car has been submerged in water, the electrical systems and internal components can suffer irreparable damage, even if it appears to dry out.

- Fire damage: Extensive fire can warp the chassis and melt critical components.

- The cost of repairs seems disproportionate to the car's age and value: Even if the damage isn't immediately catastrophic, if the parts and labour are very high relative to the car's worth, it's a strong indicator.

- The assessor's comments: Listen carefully to what the assessor says. Phrases like "beyond economical repair" or "uneconomical to repair" are clear indicators.

Frequently Asked Questions (FAQs)

Q1: Can I repair my car myself if it's a write-off?

If your car is Category A, absolutely not. If it's Category B, you can only keep it if it's dismantled by an Authorised Treatment Facility. You cannot legally repair and drive a Category B vehicle.

Q2: What if my car is written off but I still owe money on a finance agreement?

If you have finance on the car, your insurer will pay out the pre-accident value directly to the finance company. If the payout is less than the outstanding finance, you may still owe money to the finance company. This is where Guaranteed Asset Protection (GAP) insurance can be beneficial.

Q3: Can I buy my written-off car back?

Yes, you can often buy the salvage back from the insurance company, especially if it's a Category B write-off. You'll receive a payout minus the salvage value. However, you cannot put a Category A vehicle back on the road. For Category B, you'd need to arrange for it to be dismantled by an ATF.

Q4: What happens to my car insurance if my car is written off?

Your insurance policy typically ends once the claim is settled. You may be entitled to a refund for any unused premium, depending on your policy terms.

Q5: How long does the write-off process usually take?

The process can vary, but typically it takes anywhere from a few days to a couple of weeks, depending on the complexity of the valuation, available evidence, and how quickly you respond to the insurer's communications.

Conclusion

Knowing whether your car is a write-off is crucial for understanding your rights and options. By understanding the categories, the insurer's valuation process, and the implications of accepting a payout or keeping the salvage, you can make informed decisions. Always communicate clearly with your insurer and don't hesitate to challenge their assessment if you believe it's inaccurate. The goal is to ensure you are treated fairly and receive the compensation you are entitled to under your policy.

If you want to read more articles similar to Is My Car a Write-Off?, you can visit the Insurance category.