02/12/2020

Navigating the intricacies of Value Added Tax (VAT) can often feel like a complex undertaking, especially when it pertains to the day-to-day running costs of a vehicle. For many businesses and individuals alike, understanding what VAT is reclaimable on vehicle maintenance and repairs is crucial for accurate financial record-keeping and maximising tax efficiency. This article aims to shed light on the common queries surrounding VAT on vehicle-related expenses, particularly focusing on MOT tests, servicing, and other associated costs within the UK tax system. We’ll delve into the nuances of VAT rates, how to correctly record expenses, and what documentation is necessary to make a valid VAT claim.

Understanding VAT Rates and Reclaims

In the United Kingdom, VAT is a consumption tax levied on most goods and services. For businesses registered for VAT, there's an opportunity to reclaim the VAT paid on eligible business expenses. However, not all expenses qualify for reclaim, and the rate of VAT applied can vary.

The standard rate of VAT in the UK is currently 20%. However, certain goods and services are subject to a reduced rate of 5% or are zero-rated (0%). For vehicle maintenance, the standard 20% rate typically applies to repairs, parts, and servicing where VAT is itemised on the invoice. It's imperative to distinguish between these rates when preparing your VAT returns.

MOT Tests and VAT

A common point of confusion arises with MOT tests. A standard MOT test is considered a service, and the fee for the MOT itself is exempt from VAT. This means that if you receive an invoice solely for an MOT test, no VAT will be charged, and therefore, no VAT can be reclaimed on that specific service. However, if your vehicle fails its MOT and requires repairs, the parts and labour for these repairs will typically be subject to the standard 20% VAT rate, provided the garage is VAT registered and charges VAT.

For instance, if a garage performs an MOT and charges £54.85 (the maximum for a car), this amount would be gross and no VAT is reclaimable. If the car then requires a new exhaust system, and the invoice shows £100 net for the exhaust parts and labour, plus £20 VAT, then the total cost is £120. In this scenario, the £20 VAT can be reclaimed if your business is VAT registered.

Servicing and Repairs

Routine servicing and general repairs to your vehicle are usually subject to the standard 20% VAT rate. When you take your vehicle for a service or repair, ensure you obtain a detailed VAT invoice. This invoice must clearly show the garage's VAT registration number, the net amount of the service, the VAT charged, and the gross total. Without a valid VAT invoice, you will not be able to reclaim the VAT paid.

The ability to reclaim VAT on vehicle expenses is generally limited to vehicles used for business purposes. If a vehicle is used for both business and private use, the VAT reclaim may need to be apportioned. For cars, VAT on leasing or hiring costs is often restricted, and VAT on the purchase of a car is generally not reclaimable for most businesses, unless it's a commercial vehicle specifically purchased for resale or hire.

Subcontractors and VAT Registration

When engaging with subcontractors for vehicle-related services, their VAT status is paramount. If a subcontractor is not VAT registered, they cannot charge VAT on their services. In such cases, their invoices will not show any VAT, and consequently, there is no VAT to reclaim. When recording these expenses in your VAT return, they are typically included in the figures for total expenses (Box 7) but do not contribute to the VAT reclaimable amount.

Let's consider the scenario you presented:

| Expense Type | VAT Status | Gross Amount | VAT Element |

|---|---|---|---|

| General Expenses | Standard Rated | £100 | £20 (assuming 20% VAT) |

| Van MOT | Exempt | £100 | £0 |

| Post Office | Exempt | £100 | £0 |

| Subcontractor 1 (Not VAT Reg) | Not Applicable | £100 | £0 |

| Subcontractor 2 (Not VAT Reg) | Not Applicable | £100 | £0 |

| Subcontractor 3 (Not VAT Reg) | Not Applicable | £100 | £0 |

In this example, the total expenses incurred that are not VAT registered or are VAT exempt amount to £500 (£100 + £100 + £100 + £100 + £100). The VAT reclaimable would be £20 from the 'General Expenses' if they were subject to VAT and you have a valid VAT invoice.

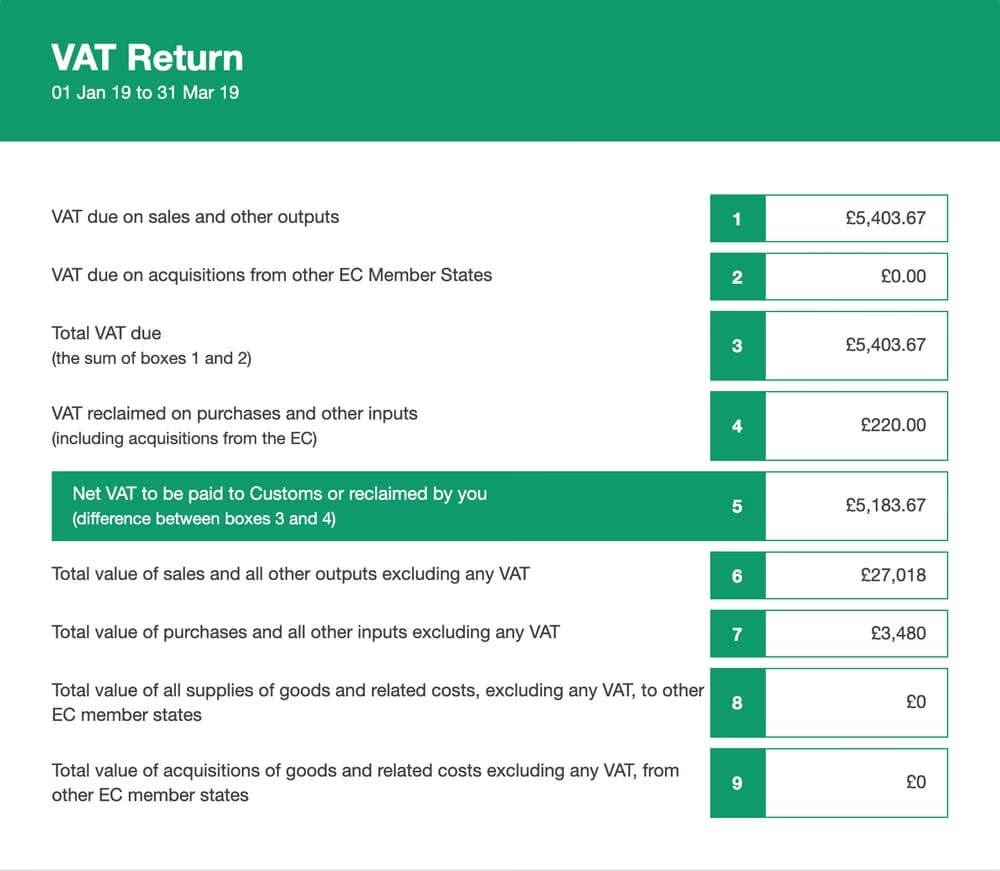

The figure entered in Box 7 of the VAT return represents the total value of all taxable and exempt supplies (excluding zero-rated supplies and capital expenditure) that your business has purchased. If your 'General Expenses' were £100 net, with £20 VAT, the total value of that expense for Box 7 would be £120. The Van MOT and Post Office expenses, being exempt, would also be included in Box 7 at their gross value (£100 each). Similarly, the payments to non-VAT registered subcontractors would be included at their gross value (£100 each).

Therefore, the total for Box 7, based on your fictitious figures, would be: £120 (General Expenses) + £100 (Van MOT) + £100 (Post Office) + £100 (Subcontractor 1) + £100 (Subcontractor 2) + £100 (Subcontractor 3) = £620. The figure of £300 you mentioned for Box 7 would only be correct if those were the only expenses and they were all net amounts with no VAT charged or exempt supplies, which is unlikely in this scenario.

Key Considerations for VAT Reclaims

1. VAT Registration Threshold

Your business must be VAT registered to reclaim VAT. The threshold for mandatory VAT registration in the UK changes periodically, so it’s important to stay updated with HMRC’s current thresholds. If your turnover is below the threshold, you can choose to register voluntarily.

2. Business Use

VAT can generally only be reclaimed on expenses that are wholly and exclusively for business purposes. If a vehicle is used for both business and private mileage, you may only be able to reclaim a portion of the VAT, or in some cases, none at all, depending on the specific circumstances and HMRC guidelines.

3. Documentation is King

As mentioned, a valid VAT invoice is essential. This document should include:

- Your supplier's (e.g., garage's) VAT registration number (usually a 9-digit UK VAT number like GB123456789 or 123456789).

- The invoice date.

- A description of the goods or services provided.

- The price, excluding VAT (net value).

- The rate of VAT applicable.

- The amount of VAT charged.

- The total amount payable, including VAT (gross value).

You can check the validity of a VAT number on the official GOV.UK website.

4. Different VAT Rates

Be aware of the different VAT rates. While most vehicle maintenance falls under the standard 20% rate, specific items or services might have different treatments. For example, certain vehicle adaptations for disabled drivers might have a reduced VAT rate. Always check your invoice carefully.

5. Record Keeping

Maintain meticulous records of all vehicle expenses and associated VAT invoices. This will not only help when preparing your VAT returns but also in case of an HMRC inquiry. Digital record-keeping systems can be very beneficial.

Frequently Asked Questions (FAQs)

Q1: Can I reclaim VAT on the purchase of a car for my business?

A1: Generally, no. VAT on the purchase of cars is usually not reclaimable for most businesses, unless it's a commercial vehicle, such as a van, specifically bought for business use or for resale, and even then, there are specific rules. VAT on car leasing or contract hire may be partially reclaimable.

Q2: My garage charged me VAT on an MOT, is this correct?

A2: No, the MOT test itself is an exempt supply and should not have VAT charged on it. If repairs were also carried out, VAT would apply to those parts and labour, but not the MOT fee itself. You should query this with the garage.

Q3: I use my car for both business and personal travel. How much VAT can I reclaim on fuel and servicing?

A3: If a vehicle is used for mixed purposes, you can generally only reclaim VAT on the business proportion of the expenses. HMRC has specific methods for calculating this, often involving mileage logs. For fuel, if you pay for fuel yourself and the vehicle is used for mixed purposes, you can claim a mileage allowance for business use, and HMRC sets specific VAT amounts per business mile. Alternatively, if the business pays for all fuel, you may have to apportion VAT based on estimated business use.

Q4: What if my supplier is not VAT registered?

A4: If your supplier is not VAT registered, they cannot charge you VAT. You will pay the gross amount they quote, and you cannot reclaim any VAT on that transaction. Their invoices will not show a VAT number.

Q5: What is a reduced VAT rate?

A5: A reduced VAT rate is a lower rate of VAT, currently 5% in the UK, applied to certain specific goods and services. While most vehicle maintenance falls under the standard 20% rate, it's always wise to check your invoices for any applicable reduced rates, though these are uncommon for typical car repairs.

In conclusion, while the prospect of reclaiming VAT on vehicle maintenance can offer significant financial benefits, it requires a thorough understanding of the rules and meticulous record-keeping. Always ensure you receive valid VAT invoices, are aware of the VAT status of your suppliers, and correctly apportion expenses for business use. By adhering to these principles, businesses can effectively manage their VAT obligations and optimise their financial performance.

If you want to read more articles similar to VAT on Vehicle Maintenance, you can visit the Automotive category.