06/08/2013

Navigating the world of automotive ownership often brings forth the question of whether to invest in a vehicle service contract (VSC), sometimes referred to as an extended warranty. While the allure of protection against unexpected repair bills is undeniable, it's crucial to approach this decision with a clear understanding of what a VSC truly entails and whether it aligns with your individual needs and financial strategy. This article aims to demystify VSCs, providing you with the knowledge to determine if this form of coverage is a necessary addition to your automotive life, or simply an unnecessary expense.

What Exactly is a Vehicle Service Contract?

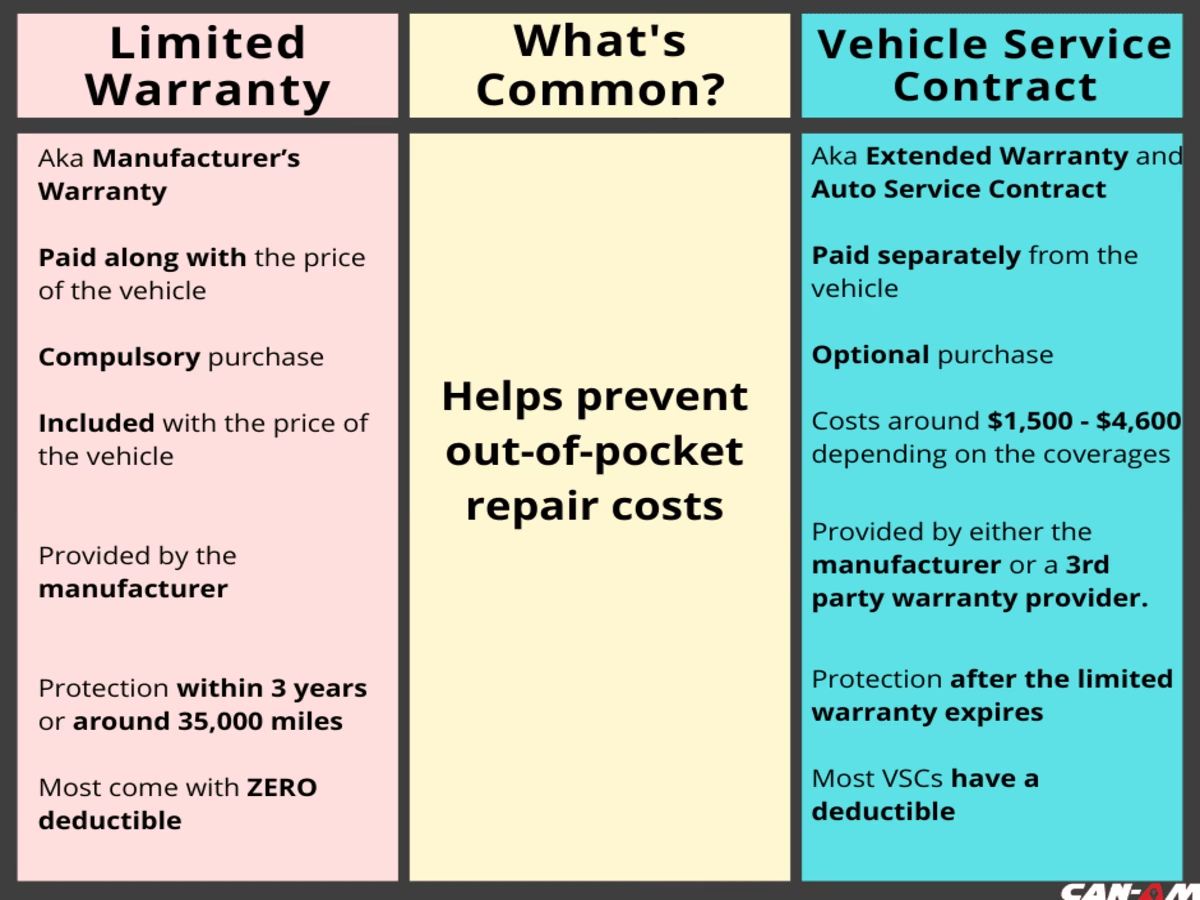

A vehicle service contract is essentially a service agreement between you and a third-party provider that agrees to cover the cost of certain repairs or replacements of vehicle components for a specified period or mileage. It's important to distinguish a VSC from a manufacturer's warranty. The manufacturer's warranty is included with the purchase of a new vehicle and covers defects in materials or workmanship. A VSC, on the other hand, is purchased separately and typically begins after the manufacturer's warranty expires. Think of it as an insurance policy for your car's mechanical parts, designed to mitigate the financial impact of breakdowns.

The Allure of Protection: Potential Benefits of a VSC

The primary appeal of a VSC lies in its promise of peace of mind. Owning a vehicle, especially as it ages, can be a significant financial commitment, and the prospect of facing a hefty repair bill for a major component like an engine or transmission can be daunting. A well-structured VSC can offer:

- Budgetary Predictability: By paying a fixed premium for the VSC, you can better budget for potential repair costs. Instead of a large, unexpected expense, you'll likely have a deductible to pay, making your out-of-pocket costs more manageable.

- Coverage for Major Components: Many VSCs offer coverage for a wide range of parts, including the engine, transmission, drive axle, and sometimes even more complex systems like air conditioning and electrical components. This can be particularly valuable for newer vehicles with sophisticated technology.

- Roadside Assistance and Other Perks: Some VSCs bundle additional benefits such as roadside assistance, towing, rental car reimbursement, and even trip interruption coverage, adding further value to the policy.

- Transferability: In many cases, VSCs are transferable to subsequent owners, which can enhance the resale value of your vehicle.

The Other Side of the Coin: Potential Downsides and Considerations

While the benefits are attractive, it's crucial to be aware of the potential drawbacks and to scrutinize any VSC offer carefully. Not all VSCs are created equal, and some can be more of a burden than a blessing. Here are key factors to consider:

Understanding Coverage Limitations: 'Cap on Components' vs. 'Cap on Policy'

One of the most critical distinctions to make is how the coverage is capped. A VSC that has a cap on the total policy means that once the total payout for repairs reaches a certain limit, the contract is exhausted, and you'll be responsible for any further costs. Conversely, a VSC with a cap on the components means that specific parts might have individual coverage limits, or certain parts might be excluded altogether. Always seek clarity on what is covered and what the limits are. A contract that covers specific components, with clear limits for each, can be more transparent than a general policy cap.

Consider the following comparison:

| Feature | 'Cap on Total Policy' VSC | 'Cap on Components' VSC |

|---|---|---|

| Maximum Payout | A single limit for all covered repairs. | Individual limits for specific components or a broader list of covered parts. |

| Risk of Exhaustion | Higher risk of exceeding the limit if multiple major repairs are needed. | Potentially lower risk of exceeding the limit if component limits are generous. |

| Transparency | Can be less transparent if the overall limit is reached quickly. | Generally more transparent regarding what each covered part is worth. |

Red Flags to Watch Out For When Purchasing a VSC

The VSC market can unfortunately attract unscrupulous sellers. Be vigilant and steer clear of providers who:

- Cannot provide all coverage information in writing, or require a substantial down payment upfront: Any reputable VSC provider will furnish you with a detailed contract outlining all terms, conditions, exclusions, and coverage limits in writing. A significant upfront payment, especially without a clear contract, is a major warning sign. Always insist on reviewing the full contract before committing.

- Focus solely on PRICE but not COVERAGE: While price is a factor, a VSC is about the quality and extent of the coverage it provides. If a seller relentlessly pushes a low price without explaining what is covered and what isn't, be suspicious. The cheapest option is rarely the best when it comes to protecting your vehicle.

- Ask for your birthdate or Social Security number too early: While some personal information is necessary for contract processing, providing sensitive data like your Social Security number or date of birth before you have a clear understanding of the contract and a commitment from the provider is risky. Reputable companies will typically only ask for this information once you've agreed to the terms and are ready to finalise the purchase.

- Will not pay up to the cash value of your vehicle: A good VSC should cover repairs up to the actual cash value (ACV) of your vehicle at the time of the breakdown. If a provider explicitly states they will not pay up to the ACV, it suggests their payouts might be capped at a lower, less favourable amount.

- Restrict repairs to only certain places: While some VSCs may have a network of approved repair facilities, a truly flexible contract should allow you to choose your preferred licensed repair shop, especially if you have a trusted mechanic. Being forced to use specific, potentially less reputable or conveniently located, repair centres can be a significant inconvenience.

- Prevent you from speaking with a live customer service representative: If you can't easily reach a human being to answer your questions or address your concerns, it's a strong indicator of poor customer service and potentially a lack of transparency. Seek out providers with accessible and responsive customer support.

Is a VSC Right for Your Vehicle?

The decision of whether a VSC is necessary depends heavily on several factors:

- Age and Mileage of Your Vehicle: Newer vehicles with low mileage are less likely to experience significant mechanical failures than older, high-mileage cars. If your car is still under its manufacturer's warranty, a VSC might be an unnecessary expense for now.

- Your Vehicle's Reliability Record: Some car models are known for their reliability, while others have a reputation for frequent and costly repairs. Research the specific make and model you own or are considering purchasing.

- Your Financial Situation and Risk Tolerance: Can you comfortably afford a significant repair bill if one arises? If the thought of a substantial, unexpected expense causes significant financial stress, a VSC might provide valuable peace of mind. Conversely, if you have a robust emergency fund and a high tolerance for risk, you might choose to self-insure.

- The Cost of the VSC vs. Potential Repair Costs: Compare the price of the VSC (including the deductible) against the potential cost of repairs for the components it covers. Use online resources and your mechanic's estimates to gauge this.

Making an Informed Decision: Key Questions to Ask

Before signing on the dotted line, arm yourself with information by asking potential VSC providers the following:

- What specific components are covered, and what are the exclusions?

- What is the duration and mileage limit of the contract?

- What is the deductible, and is it per repair visit or per covered component?

- Can I choose my preferred repair facility, or am I restricted to a network?

- What is the process for filing a claim?

- What is the company's history and reputation for handling claims?

- Will the contract pay up to the actual cash value of my vehicle?

- Is the contract transferable, and are there any fees associated with it?

Conclusion: A Calculated Choice

Ultimately, a vehicle service contract is not a one-size-fits-all solution. It's a financial product that can offer valuable protection, but only if you choose a reputable provider with a comprehensive and transparent contract. By understanding the nuances of coverage, being wary of red flags, and carefully assessing your own needs and financial circumstances, you can make an informed decision about whether a VSC is a necessary investment for your vehicle ownership journey. Do your homework, read the fine print, and prioritize coverage over a low price to ensure you're making a wise choice.

Frequently Asked Questions

Q1: Is a vehicle service contract the same as an extended warranty?

A1: While often used interchangeably, a vehicle service contract is a contract for services, whereas an extended warranty is a form of insurance. In practice, they serve a similar purpose of covering repairs after the manufacturer's warranty expires.

Q2: Should I buy a VSC when I buy a new car?

A2: It's often advisable to wait until closer to the expiration of your manufacturer's warranty. This gives you time to research VSC providers and compare offers, and new cars are generally less likely to need major repairs in their early years.

Q3: What happens if the VSC provider goes out of business?

A3: This is a valid concern. Some VSCs are backed by insurance policies, meaning an insurance company will cover claims if the VSC provider fails. Always inquire about this backing.

Q4: Can I cancel my VSC if I change my mind?

A4: Most VSCs allow cancellation, often with a prorated refund. However, there may be cancellation fees, so check the contract terms.

Q5: Does a VSC cover routine maintenance?

A5: Generally, no. VSCs typically cover unexpected mechanical breakdowns and part failures, not routine maintenance like oil changes, tyre rotations, or brake pad replacements.

If you want to read more articles similar to Vehicle Service Contracts: Are They Worth It?, you can visit the Automotive category.