24/07/2020

Experiencing a car accident can be incredibly unsettling, and discovering your beloved vehicle has been declared a 'total loss' adds another layer of stress. This often means the damage is so extensive that the cost to repair it outweighs its market value, leaving you needing a new set of wheels. Beyond the immediate practicalities, a total loss declaration can significantly impact your car insurance premiums, with the specifics largely depending on whether you were deemed at fault for the incident and your past claims history. Understanding these dynamics is crucial for navigating the aftermath and preparing for future insurance costs.

- Understanding 'Total Loss' and Your Compensation

- The Impact on Your Insurance Premiums

- The Immediate Aftermath: What to Do After an Accident

- Reporting Your Accident: Insurers and Police

- Frequently Asked Questions About Total Loss and Insurance

- Q1: How long does it take for an insurer to declare a car a total loss?

- Q2: Can I keep my car if it's declared a total loss?

- Q3: Will my no-claims bonus be affected by a total loss claim?

- Q4: What if I owe more on my car finance than the actual cash value?

- Q5: How long do I have to make a car insurance claim after an accident?

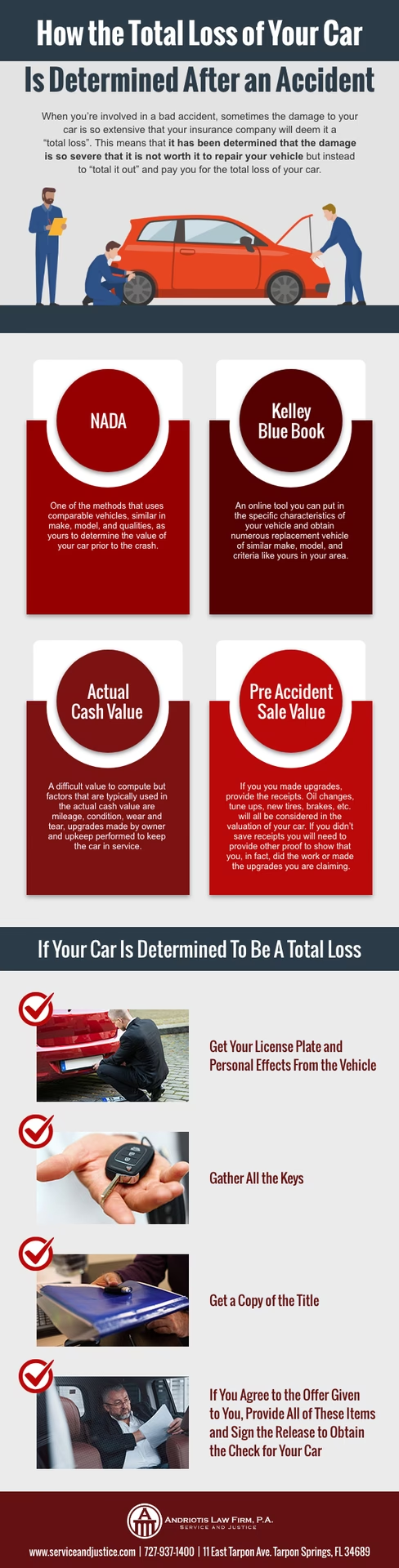

Understanding 'Total Loss' and Your Compensation

When your insurer declares your vehicle a total loss, it generally means that the economic cost of repairing the damage exceeds the vehicle's market value at the time of the accident. This threshold varies between insurers, but it's fundamentally a financial decision based on repair estimates versus the car's worth. You will typically be compensated based on the vehicle's actual cash value (ACV), which is its current market value just before the accident, minus any depreciation. Each insurance company employs its own methodology for determining this value, often using market data for similar vehicles.

It's important to differentiate between the cost of repair and the ACV. Even if repairs are technically possible, if they are economically unviable compared to replacing the vehicle, it will be written off. This ensures that insurers aren't paying more to fix a car than it would cost to buy an equivalent replacement.

One of the most pressing concerns after a total loss is how it will affect your future insurance premiums. Several factors come into play, and their weighting can vary significantly between different insurance providers.

Were You At Fault?

A primary determinant in whether your premium will increase is whether you were found to be at fault for the accident. If you were not responsible for the collision, the likelihood of a significant premium hike is generally lower. However, if you were deemed to be at fault, you can almost certainly expect your premium to rise. Insurers view at-fault accidents as a greater indication of risk, and this is directly reflected in your subsequent policy costs. For instance, being struck while stationary at a stop sign will typically have a less severe impact on your premium than if you were responsible for the collision.

Severity and Frequency of Claims

A total loss inherently implies extensive damage and a substantial payout from your insurer. Some insurers consider the magnitude of the claim when assessing future rates, meaning a total loss could increase your chances of a premium increase simply due to the high cost involved. Furthermore, if this isn't your first accident or claim, insurers may begin to categorise you as a higher risk. A history of frequent claims, particularly if coupled with a total loss, could lead to your insurer considering cancelling your coverage upon renewal. Should this occur, you might find yourself needing to seek 'high-risk' coverage, which is considerably more expensive.

Accident Forgiveness

Many car insurance providers offer 'accident forgiveness' programmes, especially for loyal customers. This typically means the company will not apply a surcharge to your premium after your first at-fault accident, provided you meet certain criteria, such as having been insured with them for a specified period. While this can save you from an immediate premium hike, it's crucial to understand that subsequent at-fault accidents will likely lead to surcharges. Moreover, even a 'forgiven' accident is still considered by the insurer when assessing your overall risk profile, potentially making future cancellations more probable if you continue to have accidents.

Here's a comparison of how different scenarios typically affect your insurance premium:

| Scenario | Typical Premium Impact | Reasoning |

|---|---|---|

| Not At Fault - First Claim | Minimal or no increase | Other party's insurer covers costs; you're not seen as a higher risk. |

| Not At Fault - Multiple Claims | Potential moderate increase | Frequent claims, even non-fault, can indicate higher exposure to risk. |

| At Fault - First Claim (with forgiveness) | No immediate increase (due to forgiveness) | Insurer waives surcharge for first incident, but risk profile noted. |

| At Fault - First Claim (without forgiveness) | Significant increase | You are responsible; seen as higher risk. |

| At Fault - Subsequent Claims | Substantial increase or potential cancellation | Pattern of risky behaviour; leads to higher risk classification. |

The Immediate Aftermath: What to Do After an Accident

Regardless of whether your vehicle is a total loss, the immediate steps following an accident are critical for your safety and for any subsequent insurance claims. Staying calm and following a structured approach can make a significant difference.

Prioritise Safety and Check for Injuries

Your first priority is always safety. Check yourself for injuries before attending to any passengers or third parties. Ensure it's safe to exit your vehicle. If anyone is injured, or if the road is blocked by debris or vehicles, or if an animal has been killed or injured (such as a dog or farm animal), you must call 999 for immediate assistance. For less urgent situations, such as needing to report an accident where no one is injured, you should call 101.

Exchange Details with Other Parties

It is a legal requirement to stop after an accident, no matter how minor. You must exchange details with any other drivers involved. This includes:

- Your car insurance policy numbers

- Number plates of all vehicles involved

- Drivers' full names, addresses, and phone numbers

- Details of the registered keeper, if different from the driver

Even if you both agree not to make a claim at the scene, having this information is vital in case circumstances change later.

Record Details of the Accident Scene

Gather as much information as possible. Take photos and videos of the scene, including damage to all vehicles, road markings, signs, and any relevant surroundings. Make detailed written notes of:

- The exact time and date of the accident

- Weather and traffic conditions

- The quality and state of the road

- A clear description of what happened, possibly with sketches

- Vehicle type, colour, make, model, and registration of all vehicles

- Estimated speed and direction of other vehicles

- The other car’s condition before the accident (if visible)

- Number of passengers in the other vehicle

- Details about the other driver (description, contact info)

- Any witnesses' contact details or locations of CCTV cameras

- Any visible injuries or property damage

- Confirmation of any dash cam footage that could serve as evidence

A Crucial Tip: Do Not Apologise!

It is natural to express concern or empathy after an accident, but you must avoid saying "I'm sorry" or anything that could be construed as an admission of fault. While legally you're not accepting responsibility by apologising, the other party or their insurer could try to use it against you later. Let the insurance companies determine fault between themselves; it's their job to investigate and negotiate.

Reporting Your Accident: Insurers and Police

Reporting an accident correctly and promptly is paramount, even if you don't intend to make a claim yourself.

Report to Your Insurer

You should always report an accident to your insurer, regardless of whether you plan to claim. This is a condition of most insurance policies. The other driver might decide to make a claim against you, and if your insurer isn't aware, it could complicate matters or even invalidate your policy. Furthermore, your insurer needs to reassess your risk profile, which is likely to impact your premium at renewal, even if no claim is made. Ideally, you should report the accident within 24 hours. Most insurers have a specific timeframe within which accidents must be reported, so check your policy wording.

Report to the Police

You are legally required to report an accident to the police if:

- Anyone is injured.

- You didn't exchange details at the scene (e.g., if the other driver left, or you hit a parked car).

- You believe a crime has been committed (e.g., 'crash-for-cash' scam, uninsured driver, driver under influence, aggressive behaviour).

If you need to report to the police, use the non-emergency number 101, and do so within 24 hours of the incident. Failing to stop and report an accident (a 'hit-and-run') can lead to severe penalties, including fines, points on your licence, or even a driving ban under the Road Traffic Act.

Frequently Asked Questions About Total Loss and Insurance

Q1: How long does it take for an insurer to declare a car a total loss?

The timeframe can vary, but it typically depends on how quickly the damage assessment can be completed and the repair estimates gathered. This process can take anywhere from a few days to a couple of weeks after the accident has been reported and the vehicle inspected.

Q2: Can I keep my car if it's declared a total loss?

In some cases, yes. If you wish to keep your vehicle, the insurer will deduct the salvage value (what the car is worth as scrap or for parts) from your payout. You will then usually receive a 'Category S' (structural damage) or 'Category N' (non-structural damage) marker for the vehicle, meaning it will need to be repaired to a roadworthy standard and re-registered before it can be driven again. This can be a complex process and is not always advisable.

Q3: Will my no-claims bonus be affected by a total loss claim?

If you were at fault, your no-claims bonus (NCB) will almost certainly be affected, unless you have NCB protection or accident forgiveness. If you were not at fault, your NCB should remain intact, as your insurer will recover costs from the at-fault party's insurer.

Q4: What if I owe more on my car finance than the actual cash value?

This is known as being 'upside down' or having 'negative equity'. Your insurer will only pay out the actual cash value of the car. If this amount is less than what you owe on your finance agreement, you will be responsible for paying the difference. This is where 'Guaranteed Asset Protection' (GAP) insurance can be invaluable, as it covers the shortfall between the ACV payout and the outstanding finance.

Q5: How long do I have to make a car insurance claim after an accident?

While you should report the accident to your insurer as soon as possible (ideally within 24 hours), the time limit for making a formal claim can be longer. For property damage claims, it's usually within a few months. For personal injury claims, you typically have up to three years from the date of the accident to make a claim, though it's always best to act promptly while details are fresh.

Navigating a total loss scenario can be challenging, but by understanding the process, your responsibilities, and the potential impacts on your insurance, you can approach the situation with greater confidence and ensure the best possible outcome.

If you want to read more articles similar to Car Total Loss: Impact on Your UK Insurance, you can visit the Insurance category.