29/05/2007

Understanding Your Tesco Car Insurance Policy

Owning a car in the UK is a necessity for many, and with it comes the legal requirement to have adequate car insurance. Tesco Bank offers a comprehensive range of car insurance policies designed to provide peace of mind on the road. However, like any financial product, understanding the ins and outs of your policy can sometimes feel a little daunting. This guide aims to demystify your Tesco car insurance, covering key aspects from identifying your policy to understanding the complaint resolution process.

Identifying Your Tesco Car Insurance Policy

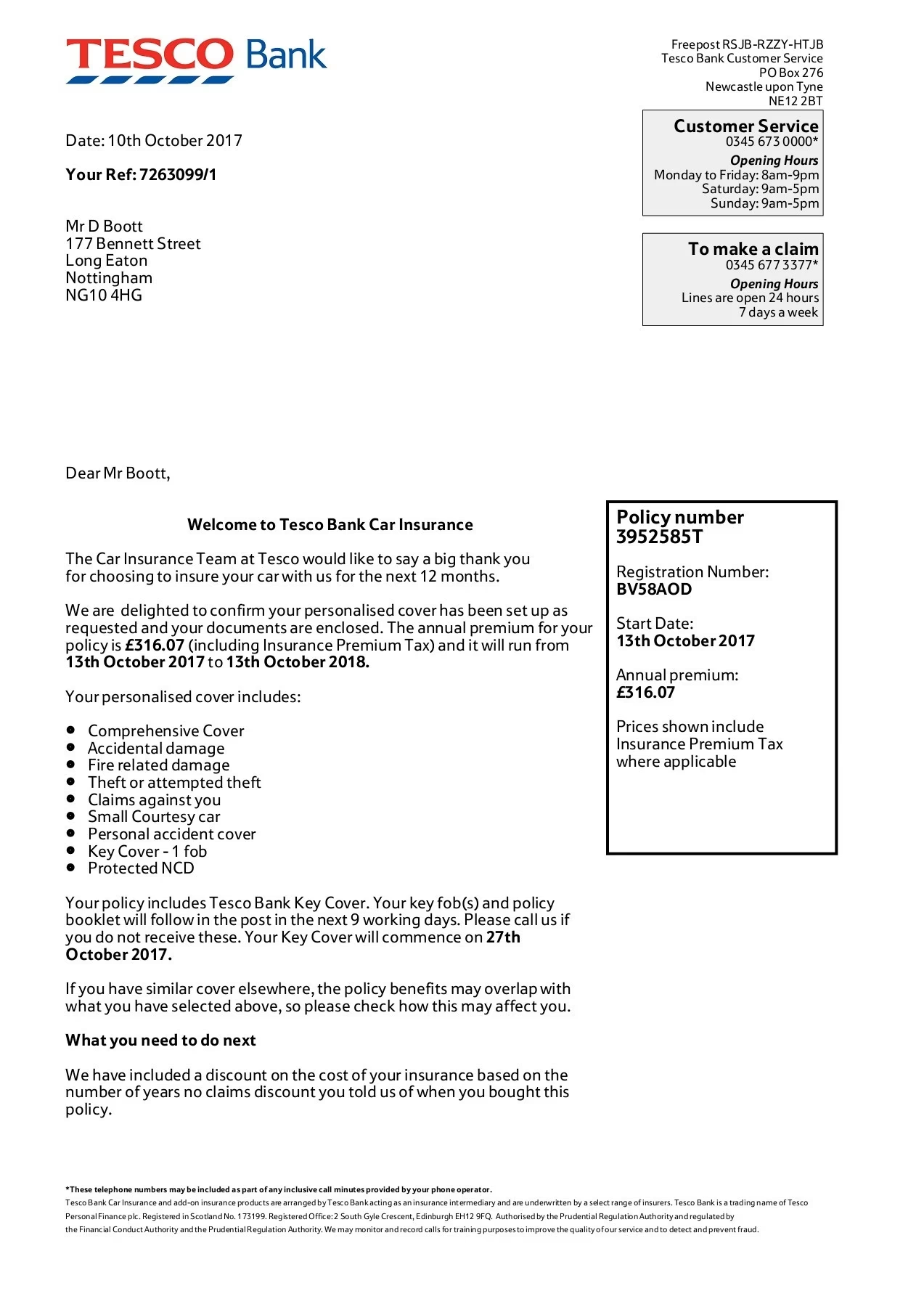

The first step to managing your car insurance is knowing how to identify your specific policy. When you take out a policy with Tesco Bank, you'll receive a Policy Schedule and Policy Wording document. These are crucial documents that contain all the essential information about your cover.

Your Policy Schedule will typically include:

- Your policy number: This is a unique identifier for your insurance. Keep it handy for any communication with Tesco Bank.

- Details of the insured vehicle: Make, model, registration number, and any modifications.

- Details of the insured drivers: Names, dates of birth, driving history, and occupation.

- The level of cover: Such as Comprehensive, Third Party, Fire and Theft, or Third Party Only.

- The period of insurance: The start and end dates of your policy.

- The premium: The amount you pay for your insurance.

- Any excess amounts: The amount you'll have to pay towards a claim.

- Any named drivers or additional drivers.

The Policy Wording document provides a more detailed explanation of what is and isn't covered by your policy, including definitions of terms used, conditions, and exclusions. It's essential to read both documents thoroughly to understand your rights and responsibilities.

If you've misplaced these documents, don't worry. You can usually access them by logging into your Tesco Bank online account or by contacting their customer service team. Having your personal details and vehicle registration number ready will help them locate your policy quickly.

How to Pay for Your Tesco Car Insurance Policy

Tesco Bank offers flexible payment options to suit your needs. The most common methods include:

- Annual Payment: You can pay the entire premium upfront for the year. This is often the most cost-effective option, as it may include a discount compared to monthly payments. You can typically pay this via debit card, credit card, or bank transfer.

- Monthly Payments: For those who prefer to spread the cost, Tesco Bank offers monthly payment plans. These are usually paid via Direct Debit. It's important to note that monthly payments may include an interest charge, making the overall cost slightly higher than an annual payment.

When setting up your policy, you'll be guided through the payment process. Ensure you have your preferred payment method details to hand. If you opt for monthly payments, you'll need to set up a Direct Debit, which involves authorising Tesco Bank to collect regular payments from your bank account.

Important Consideration: If you choose to pay by Direct Debit and miss a payment, it can have significant consequences. Your insurance cover could be cancelled, which is illegal if you continue to drive. It's crucial to ensure you have sufficient funds in your account on the agreed payment dates.

Making a Complaint: Your Rights and Process

While Tesco Bank strives to provide excellent service, there may be instances where you need to make a complaint. Understanding the process ensures your concerns are addressed effectively and fairly.

The Complaint Resolution Timeline

Tesco Bank aims to resolve complaints as quickly as possible. The timeline for resolution typically follows these stages:

- Within 4 Business Days (Summary Resolution): If your complaint is resolved within four business days, Tesco Bank will send you a 'Summary Resolution' communication via text, email, or letter. This will include information about the Financial Ombudsman Service (FOS).

- Within 2 Weeks: In most cases, complaints are resolved within two weeks. If it takes longer, you will be updated on the progress and an estimated resolution time.

- Within 5 Weeks: If a resolution hasn't been reached within five weeks, you will receive another update. At this stage, you may become eligible to refer your complaint to the FOS.

- Within 8 Weeks: While not ideal, complex issues might require more time. If it takes longer than eight weeks, Tesco Bank will either request more time or issue a 'Final Response'. Again, you may be eligible to contact the FOS.

What Happens if Agreement Cannot Be Reached?

If Tesco Bank and you cannot agree on a resolution, Tesco Bank will issue a Final Response letter. This letter will clearly state their position on your complaint. Crucially, it will also advise you on how to contact the Financial Ombudsman Service (FOS) if you wish for them to review your case.

The Financial Ombudsman Service (FOS)

The FOS is a free and independent service that can help resolve disputes between consumers and financial businesses. They can look into most financial complaints, although there are some limitations. You can obtain further information directly from the FOS.

Tesco Bank is committed to resolving complaints fairly and internally. If you are unhappy with the suggested resolution, or if eight weeks have passed since you first raised your complaint, you have the right to escalate the matter to the FOS.

Important Note on Time Limits: If you decide to take your complaint to the FOS, you must usually do so within six months of the date of the Final Response letter you receive from Tesco Bank. Missing this deadline could mean you lose your right to their assistance.

Frequently Asked Questions

| Question | Answer |

| How do I find my policy number? | Your policy number is clearly stated on your Policy Schedule document. If you can't find it, log in to your Tesco Bank online account or contact customer services. |

| Can I change my payment method? | Yes, you can usually change your payment method. Contact Tesco Bank customer services to discuss your options. You may need to do this well before your next payment is due. |

| What should I do if I miss a payment? | Contact Tesco Bank immediately to discuss the missed payment. Failure to do so could lead to your policy being cancelled, leaving you uninsured. |

| What is the excess on my policy? | The excess is the amount you agree to pay towards any claim. Your specific excess amount is detailed in your Policy Schedule. There may be different excess amounts for different types of claims (e.g., windscreen claims). |

| When should I contact the Financial Ombudsman Service? | You can contact the FOS if you are unhappy with Tesco Bank's final response to your complaint, or if eight weeks have passed without a resolution. Remember the six-month deadline from the final response. |

Conclusion

Managing your Tesco car insurance policy is straightforward when you know where to find the information you need. By familiarising yourself with your Policy Schedule and Wording, understanding your payment options, and knowing the process for making a complaint, you can ensure you're adequately covered and your concerns are addressed. Remember, your insurance documents are your best resource, and Tesco Bank's customer service team is there to help if you have any questions or require assistance.

If you want to read more articles similar to Tesco Car Insurance: Your Policy Explained, you can visit the Insurance category.