07/07/2006

- Understanding Your Tesco Bank Car Insurance Renewal

- The Renewal Process: What to Anticipate

- Benefits of Renewing with Tesco Bank

- Is Your Renewal Quote the Best Deal? The Importance of Comparison

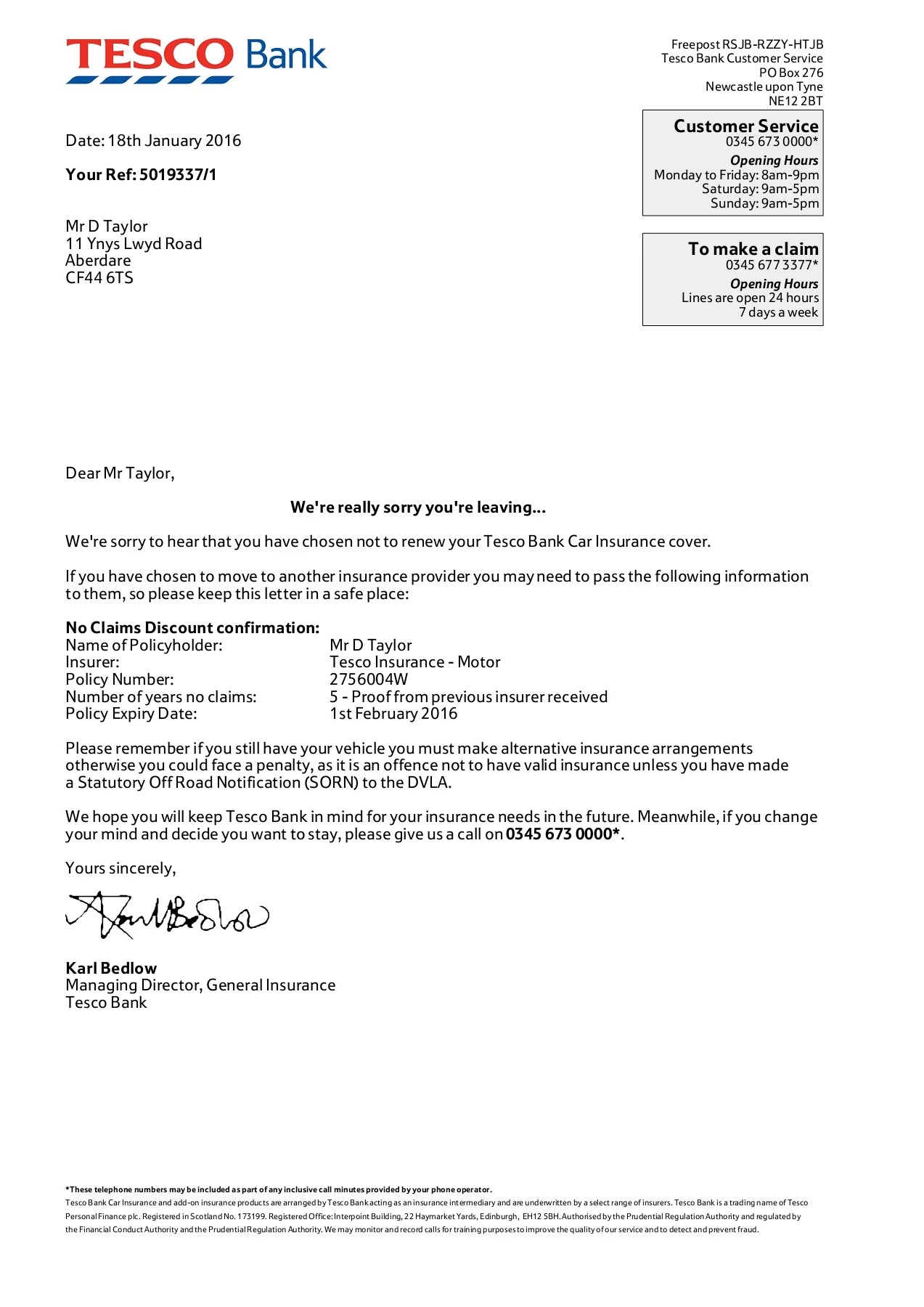

- What Happens If You Don't Renew?

- Making Changes to Your Policy Upon Renewal

- Table: Tesco Bank Renewal vs. Comparison Quotes

- Frequently Asked Questions (FAQs)

- Conclusion

Understanding Your Tesco Bank Car Insurance Renewal

Renewing your car insurance is a crucial step in ensuring you remain legally covered on the road. If you're a Tesco Bank customer, you might be wondering what happens when your policy is due for renewal. This guide will walk you through the process, highlighting key aspects to consider, potential benefits of sticking with Tesco Bank, and important factors to weigh before you commit to another year of cover. From understanding price changes to ensuring you're still getting the best deal, we've got you covered.

The Renewal Process: What to Anticipate

Tesco Bank, like most insurers, will typically send you a renewal invitation well in advance of your policy's expiry date. This invitation usually contains your renewal quote, which is the price you'll pay for the next 12 months if you choose to renew. It's vital to review this document carefully. Don't just assume the price will be the same or even lower than your previous year's premium. Insurers use a complex algorithm that considers various factors, including your claims history, driving behaviour, the car you drive, and even changes in the market and regulatory environment. Therefore, your renewal quote can fluctuate.

Key information to look for in your renewal invitation:

- Your new premium: This is the most obvious and important figure. Compare it to what you paid last year.

- Policy details: Ensure that your personal details, vehicle information, and the level of cover remain accurate. Any changes might affect your premium or the validity of your policy.

- No-claims discount (NCD): Verify that your NCD has been applied correctly. A higher NCD generally leads to a lower premium.

- Excess levels: Check the voluntary and compulsory excess amounts. Increasing your voluntary excess can sometimes lower your premium, but it means you'll pay more if you need to make a claim.

- Cover options: Review the types of cover included (e.g., comprehensive, third-party, fire and theft) and any optional extras you may have added.

Benefits of Renewing with Tesco Bank

Sticking with your current insurer can offer convenience, but it's essential to assess whether it's also the most cost-effective and suitable option. Tesco Bank often promotes loyalty benefits and a streamlined renewal process for its existing customers. If you've had a good experience with their customer service and haven't had any major issues with your policy, renewing might seem like the easiest path.

Some potential benefits of renewing with Tesco Bank might include:

- Convenience: The renewal process is often simplified, requiring minimal effort from your side if your circumstances haven't changed.

- Potential loyalty discounts: While not always explicitly stated, insurers may sometimes offer preferential rates to loyal customers.

- Familiarity: You're already acquainted with their policy terms, claims process, and customer service.

- Clubcard points: Tesco Bank often offers Clubcard points on their insurance products, which can be a valuable perk for regular Tesco shoppers. Accumulating points can lead to savings on groceries or other Tesco purchases.

Is Your Renewal Quote the Best Deal? The Importance of Comparison

This is perhaps the most critical aspect of the renewal process. While renewing with Tesco Bank might be convenient, it's highly unlikely to be the absolute cheapest or best-value option available. Insurers often price their policies to attract new customers, which can mean that renewal quotes are higher than what new customers might be offered for a similar level of cover. This is often referred to as the "loyalty penalty".

Therefore, it is strongly recommended that you compare your Tesco Bank renewal quote with those from other insurance providers. Use comparison websites or contact other insurers directly to get quotes for the exact same level of cover. This will give you a clear picture of the market rates and help you determine if you can get a better deal elsewhere.

Factors to consider when comparing quotes:

- Price: The most obvious factor, but not the only one.

- Level of cover: Ensure you're comparing like for like. Don't be tempted by a cheaper policy that offers significantly less protection.

- Excess: A lower premium might come with a higher excess, making it more expensive to claim.

- Policy exclusions: Read the small print to understand what is and isn't covered.

- Customer reviews and ratings: Look at independent reviews to gauge the insurer's reputation for customer service and claims handling.

- Optional extras: Consider if you need additional cover like breakdown assistance, legal protection, or a courtesy car, and compare the cost of these.

What Happens If You Don't Renew?

If your Tesco Bank car insurance policy expires and you haven't renewed it, your vehicle will be uninsured. Driving an uninsured vehicle is illegal in the UK and can lead to severe penalties, including:

- An £800 fine (or more if taken to court).

- Having your vehicle seized by the police.

- Penalty points on your driving licence.

- A driving ban.

- Difficulty getting insurance in the future.

It is absolutely essential to have continuous car insurance cover. If you decide not to renew with Tesco Bank, ensure you have a new policy in place before your current one expires.

Making Changes to Your Policy Upon Renewal

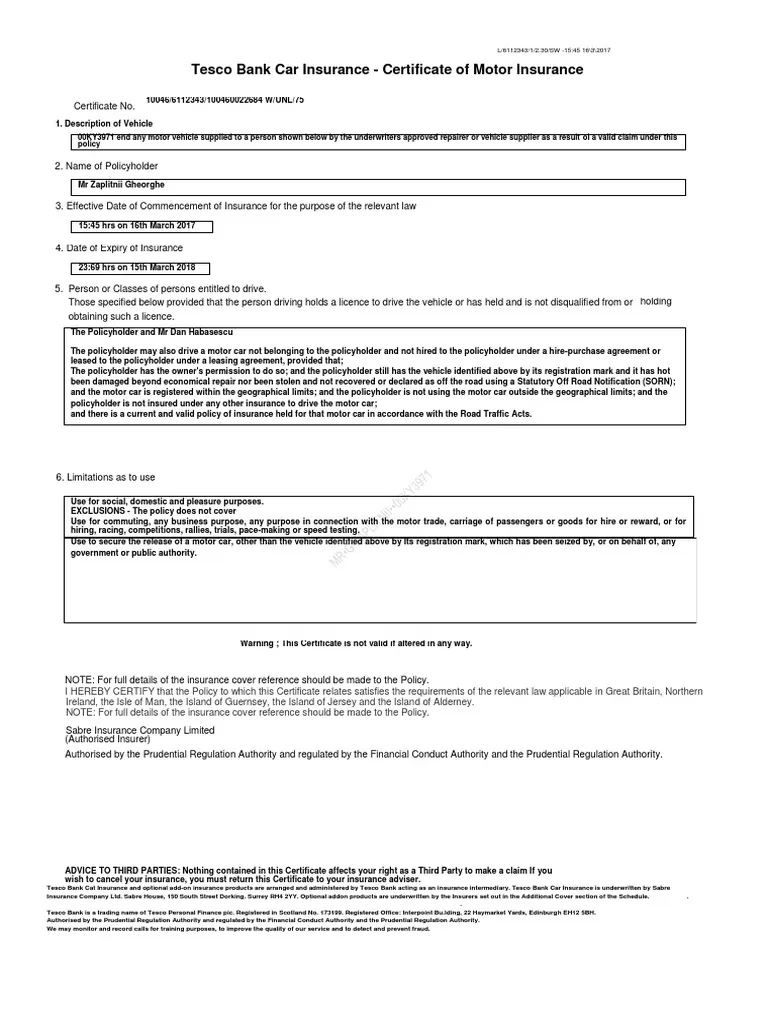

The renewal period is also an opportune time to update your policy if your circumstances have changed. Informing your insurer of any changes is crucial for maintaining valid cover. Changes you might need to declare include:

- Change of address: Even a slight change in your postcode can affect your premium.

- Change of vehicle: If you've bought a new car.

- Change of occupation: Some occupations are considered higher risk than others.

- Changes to your vehicle: Modifications like a new stereo, alloy wheels, or performance enhancements.

- Changes to drivers: Adding or removing drivers from the policy.

- Annual mileage: If your estimated annual mileage has significantly increased or decreased.

Failing to declare relevant changes can invalidate your insurance, meaning any claims made might not be paid out, and you could face prosecution.

Table: Tesco Bank Renewal vs. Comparison Quotes

To illustrate the importance of comparison, consider this hypothetical scenario:

| Feature | Tesco Bank Renewal Quote | Best Comparison Quote |

|---|---|---|

| Annual Premium | £550 | £420 |

| Voluntary Excess | £250 | £300 |

| Comprehensive Cover | Yes | Yes |

| Breakdown Cover | Included | Optional Extra (+ £50) |

| Clubcard Points | Earned | N/A |

| Overall Cost Saving | N/A | £130 (plus potential for points) |

In this example, while Tesco Bank offers a familiar service and Clubcard points, switching could save you £130 annually, even with an additional cost for breakdown cover. This highlights the potential financial benefit of shopping around.

Frequently Asked Questions (FAQs)

Q1: What if I'm not happy with my Tesco Bank renewal quote?

If you find your renewal quote is too high or doesn't meet your needs, you have the option not to renew and to seek cover elsewhere. Make sure to arrange your new policy to start immediately after your current one ends to avoid any lapse in cover.

Q2: Can I cancel my Tesco Bank policy if I renew and then find a better deal?

Yes, you generally have a cooling-off period (usually 14 days) after renewing your policy during which you can cancel and receive a refund, minus any administrative fees or pro-rata costs for the time you've been covered. However, check your policy documents for specific terms.

Q3: Do I need to tell Tesco Bank if I've had claims or convictions since last year?

Absolutely. You must declare any new claims, accidents, or driving convictions to your insurer. Failure to do so could invalidate your policy.

Q4: What is a cooling-off period?

A cooling-off period is a set number of days after purchasing or renewing a policy during which you can cancel without penalty (though some insurers may charge a small administration fee). It's a statutory right for most insurance policies bought remotely.

Q5: How far in advance should I start looking for car insurance?

It's generally advisable to start shopping around for car insurance about 21 days before your current policy expires. This is often cited as the 'sweet spot' for finding the best prices.

Conclusion

Renewing your Tesco Bank car insurance policy can be a straightforward process, but it's crucial to approach it with a proactive mindset. Always review your renewal invitation thoroughly, understand the changes in your premium, and, most importantly, compare your quote with those from other insurers. While loyalty has its merits, ensuring you have the most suitable and cost-effective cover for your needs should be your priority. By taking the time to compare and update your details, you can drive with confidence, knowing you're protected and getting the best possible value for your money.

If you want to read more articles similar to Tesco Bank Car Insurance Renewal: What to Expect, you can visit the Insurance category.