22/03/2007

Navigating the world of car insurance can often feel like a complex journey, but what if you only need cover for a short period? Whether you're borrowing a friend's car, test-driving a potential new purchase, or simply need to move a SORNed vehicle, traditional annual policies aren't always the most practical or economical solution. This is where temporary car insurance steps in, offering a flexible and immediate answer to your short-term driving needs in the UK.

- What Exactly is Temporary Car Insurance?

- Which Insurers Offer Temporary Car Insurance in the UK?

- Do You Really Need Temporary Car Insurance? Understanding Your Options

- How Much Does Temporary Car Insurance Cost?

- Tips for Getting Cheap Temporary Car Insurance

- Can You Get Temporary Car Insurance Without a Main Policy?

- Can You Tax Your Car if You Have Temporary Car Insurance?

- Temporary Car Insurance for Young Drivers

- Driving in Europe with Temporary Car Insurance

- Frequently Asked Questions About Temporary Car Insurance

What Exactly is Temporary Car Insurance?

Temporary car insurance provides immediate, short-term cover for driving a vehicle, be it one you own or someone else's. Unlike standard annual policies, temporary cover offers remarkable flexibility, allowing you to choose the exact duration you need – typically ranging from as little as an hour to several months. A significant advantage is that this type of cover is usually fully comprehensive, mirroring the robust protection offered by a standard policy. This means you're covered for damage to your vehicle, third-party vehicles, fire, and theft, offering peace of mind even for brief periods.

Common Scenarios Where Temporary Cover Shines:

- Helping a Friend or Family Member: If you need to drive a loved one's car to assist them, perhaps for a trip to the hospital or moving house, temporary insurance ensures you're legally covered without affecting their existing policy.

- Learning to Drive: While specialist learner driver policies exist, temporary cover can be a great option for additional practice in a family member's car, providing comprehensive cover for that specific period.

- Buying or Selling a Car: Test-driving a vehicle you're considering purchasing, or letting a potential buyer take your car for a spin, becomes straightforward with temporary insurance. It ensures both parties are protected during the trial period.

- Occasional Use of a Second Car or SORNed Vehicle: For cars that are typically off the road (SORNed - Statutory Off Road Notification) but occasionally need to be moved or used, temporary cover provides the necessary legal insurance without the commitment of an annual policy.

- Sharing Driving Duties on a Long Journey: If you're embarking on a long drive with a friend and want to share the wheel, temporary cover allows you to drive their car legally and safely.

- Emergency Situations: In unforeseen circumstances where you urgently need to drive someone else's car, temporary insurance can be set up quickly to get you on the road.

Which Insurers Offer Temporary Car Insurance in the UK?

The market for temporary car insurance has grown significantly, with several reputable insurers offering these flexible policies. While comparison sites are an excellent starting point for finding competitive quotes, it's also wise to check directly with individual firms, as prices can sometimes differ. It’s crucial to compare not just the premium, but also the terms, conditions, and the excess amount – the portion of any claim you have to pay yourself.

Here's a snapshot of some providers offering temporary car insurance, alongside key details to help you compare:

| Brand | How to Take Out Insurance | Maximum Cover Length Available | Minimum Age | Maximum Age | Standard Excess | Maximum Vehicle Value |

|---|---|---|---|---|---|---|

| Cuvva | Provider site | 28 days | 19 | 65 | Varies | £60,000 |

| Day Insure by Aviva | Provider site | 30 days | 18 | 75 | £250 | £50,000 |

| GoShorty | Provider site | 28 days | 19 | 75 | Varies | £60,000 |

| Tempcover | Provider site | 28 days | 17 | 78 | Varies | £65,000 |

| Veygo by Admiral | Provider site | 60 days | 17 | 75 | Varies | Varies |

| Safely Insured | Provider site | 84 days | 18 | 75 | £100 | £65,000 |

Table notes: Information correct as of January 2025. Please note that terms, conditions, and availability can change, so always verify details directly with the insurer.

Do You Really Need Temporary Car Insurance? Understanding Your Options

Before jumping into a temporary policy, it's worth assessing if it's genuinely the best option for your circumstances. Many drivers with an existing annual car insurance policy might already have some form of cover for driving other cars under what's known as the 'Driving Other Cars' (DOC) clause. However, this cover is often highly restricted and rarely offers the same level of protection as a temporary comprehensive policy.

Driving Other Cars (DOC) Clause: What You Need to Know

If your main policy includes DOC, it typically provides third-party only cover when you drive a vehicle not owned by you. This means that in the event of an accident, only damage to the other vehicle or property, and injuries to third parties, would be covered. Any damage to the car you are driving would not be covered. Crucially, there are often significant exclusions:

- Age Restrictions: Drivers under the age of 25 are very rarely covered by the DOC clause.

- Occupation Exclusions: Certain occupations might also exclude you from this cover.

- Vehicle Type: Not all types of vehicles may be covered.

- Permission: You must always have the vehicle owner's explicit permission.

Given these limitations, relying solely on your DOC clause can be risky. For comprehensive protection and peace of mind, especially when driving someone else's valuable vehicle, a dedicated temporary policy is almost always the safer bet.

Adding Yourself as a Named Driver: A Long-Term Solution

Another alternative is to be added as a named driver to the vehicle owner's existing annual policy. This can be a cost-effective long-term solution if you plan to drive the car regularly. However, it usually involves an administrative fee (averaging around £20), and crucially, any claims made while you are driving could impact the main policyholder's no-claims discount. For very short periods, from an hour to a few days, buying separate temporary cover is likely to be cheaper and avoids the risk of jeopardising someone else's valuable no-claims bonus.

How Much Does Temporary Car Insurance Cost?

The cost of temporary car insurance, much like standard annual policies, is determined by a variety of factors. Insurers assess the level of risk based on:

- Your Age: Younger and less experienced drivers typically face higher premiums.

- Your Occupation: Certain professions are deemed higher risk than others.

- Your Location: Postcodes with higher crime rates or accident statistics can increase costs.

- Driving History: Your driving record, including any convictions or previous claims, will influence the price.

- Vehicle Details: The make, model, age, and value of the car you wish to insure play a significant role. More powerful or expensive cars generally cost more to insure.

- Duration of Cover: Naturally, the longer you need cover, the higher the total cost will be.

For short durations, typically a few days or weeks, a temporary policy often presents better value than the combined cost and hassle of adjusting an existing policy or being added as a named driver. However, there's a tipping point. The longer you require cover, the closer you get to a scenario where an annual policy becomes more financially viable. This threshold is reached even faster if the alternative is paying to become a named driver on someone else's policy, considering the administrative fees and potential impact on their no-claims discount.

It's also essential to scrutinise what you're getting for your money. Temporary policies sometimes come with higher excesses than standard policies. A higher excess means you'll have to pay more out of your own pocket in the event of a claim, so always ensure the excess amount is affordable for you.

Tips for Getting Cheap Temporary Car Insurance

While the factors above influence your premium, there are strategies you can employ to secure the most competitive rates for temporary cover:

- Shop Around Extensively: Don't settle for the first quote. Use multiple price comparison websites, as different sites may work with different panels of insurers. Furthermore, check the websites of insurers not listed on comparison sites, as direct quotes can sometimes be more competitive.

- Only Buy What You Need: Many insurers offer temporary insurance by the hour, day, or week. Be precise about the duration you require and avoid purchasing more cover than necessary. Even an extra day can add to the cost.

- Consider a Higher Excess: Opting for a higher voluntary excess can lower your premium. However, ensure that the chosen excess amount is genuinely affordable for you in the event of an accident. It's a balance between a lower premium now and potentially higher out-of-pocket costs later.

- Consult an Independent Insurance Broker: For more complex situations or if you're struggling to find suitable cover, an independent insurance broker can be invaluable. They have access to a wider range of policies and can scour the market on your behalf, often identifying tailored solutions that might not be available directly to the public. They can also offer expert advice on the best match for your specific circumstances.

- Maintain a Clean Driving Record: While not a quick fix for temporary insurance, a clean driving record with no convictions or claims will always result in lower premiums across all types of car insurance.

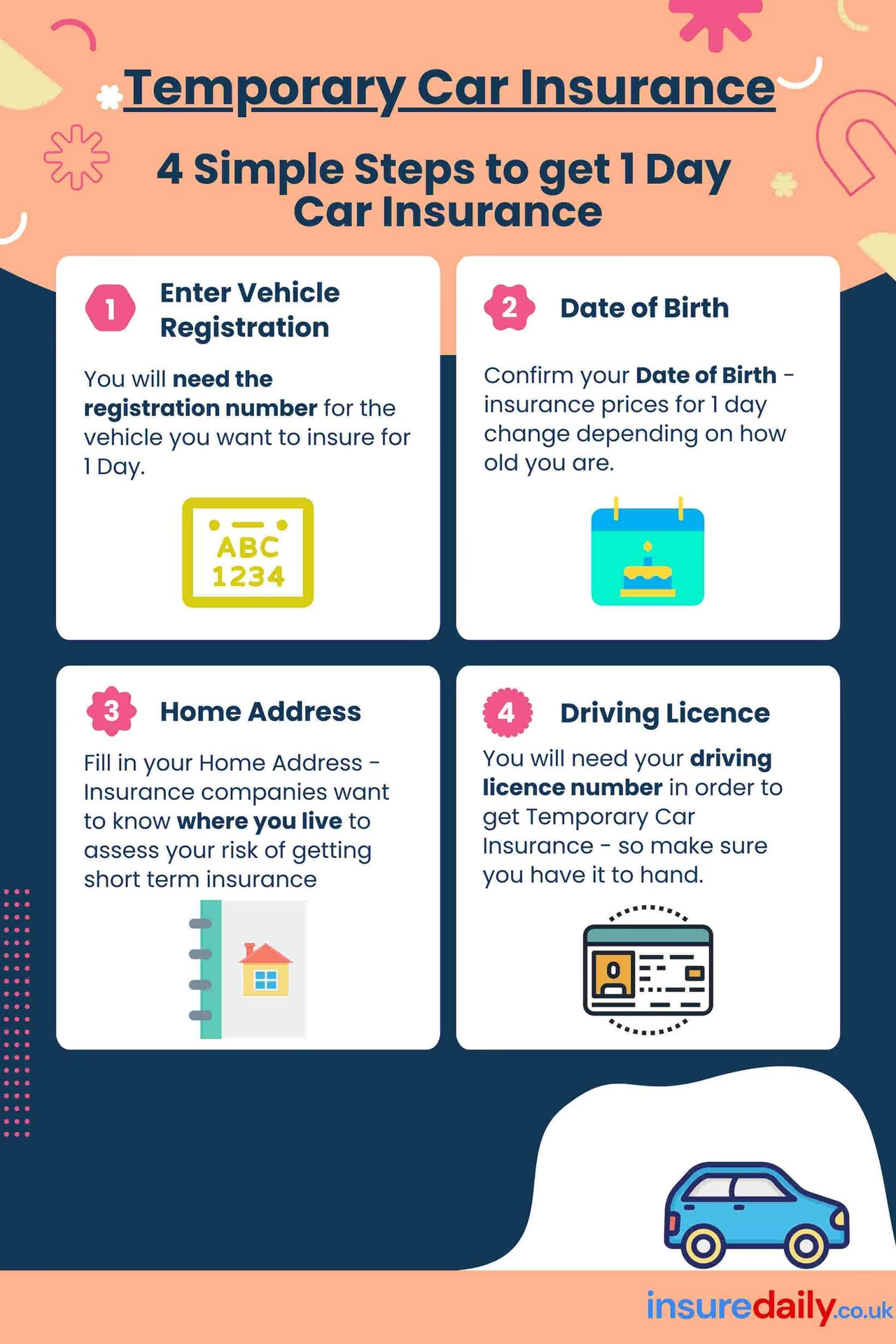

Can You Get Temporary Car Insurance Without a Main Policy?

Absolutely, yes. One of the significant advantages of temporary car insurance is that you do not need to hold an existing annual car insurance policy to take one out. This makes it an ideal solution for individuals who don't own a car, or who rely on public transport but occasionally need to drive a friend's or family member's vehicle.

The primary requirements for purchasing temporary cover are:

- A valid UK driving licence.

- If you are borrowing the vehicle, explicit permission from the vehicle's owner.

- The vehicle must be roadworthy and have a valid MOT (if required for its age).

Can You Tax Your Car if You Have Temporary Car Insurance?

Yes, you can. When you purchase any form of car insurance in the UK, including temporary policies, your insurer is legally required to add your details to the Motor Insurance Database (MIB). The MIB is a central digital register of all insured vehicles in the UK, and it operates in the same way for temporary cover as it does for standard annual policies.

This is a critical point because you cannot pay for Vehicle Excise Duty (VED), commonly known as car tax, on a vehicle that is not insured. When you attempt to tax your vehicle online or at a Post Office, a real-time check is made against the MIB to confirm that the vehicle has valid insurance in place. As long as your temporary insurance details are successfully registered on the MIB, you will be able to proceed with taxing your vehicle without any issues.

Temporary Car Insurance for Young Drivers

As with all forms of car insurance, age is a significant factor in determining premiums for temporary cover. Drivers under the age of 25, often considered higher risk due to less driving experience, are likely to face considerably higher costs. Insurers assess young drivers as more prone to accidents, leading to elevated premiums across the board.

If you're a young driver looking to insure someone else's car for a short period, it's particularly important to compare the cost of temporary car insurance quotes with the alternative of being added as a named driver on the car owner's annual insurance. For very short durations (a few hours to a day), temporary cover might still be more cost-effective. However, for periods exceeding a week, temporary car insurance can quickly become very expensive for young drivers, making the named driver option potentially more appealing despite the administrative fees.

Young drivers should also explore options like black box car insurance for their own vehicles, as this can significantly reduce annual premiums by monitoring driving habits.

Driving in Europe with Temporary Car Insurance

Planning a trip across the English Channel and need temporary cover? Most temporary car insurance policies will provide some level of cover for drivers taking their vehicles to continental Europe. However, it's crucial to understand that this often comes with a reduced level of protection, frequently defaulting to third-party cover only.

This means that while you would be covered for damage or injury caused to other vehicles or individuals, any damage to your own vehicle would not be covered. If you require comprehensive cover for your European travels, you must double-check your policy's terms and conditions or contact your insurer directly before you travel.

If your current temporary policy doesn't offer sufficient European cover for your needs, your insurer may be willing to upgrade your policy or sell you specific European travel cover for an additional charge. Alternatively, it might be more cost-effective to purchase a separate temporary car insurance policy specifically designed for European driving from a different insurer. Always compare options to ensure you have adequate protection for your journey abroad.

Frequently Asked Questions About Temporary Car Insurance

- What is the shortest period I can get temporary car insurance for?

- Many providers offer temporary cover for as little as one hour, making it incredibly flexible for very brief needs.

- Is temporary car insurance always comprehensive?

- While most reputable temporary car insurance policies offer fully comprehensive cover, it's essential to always check the policy details before purchasing. Some may offer third-party, fire, and theft, or even just third-party cover, especially if it's an extension of an existing policy's DOC clause for European travel.

- Can I use temporary insurance for business purposes?

- This depends entirely on the insurer and the specific policy. Many standard temporary policies are for social, domestic, and pleasure use only. If you need to use the vehicle for business, you must declare this when getting a quote and ensure the policy explicitly states that it covers business use. Failure to do so could invalidate your insurance.

- What happens if I have an accident with temporary car insurance?

- If you have an accident, you should follow the same procedures as with any standard insurance policy: ensure everyone is safe, exchange details with the other party, gather evidence (photos, witness details), and contact your temporary insurer as soon as possible to report the incident. Remember your excess will apply.

- Can I extend my temporary car insurance policy?

- Many providers allow you to extend your cover if you need it for longer than initially planned. However, it's often easier and sometimes more cost-effective to purchase a new policy for the extended period, especially if the original policy was for a very short duration. Always check with your provider about their extension process and pricing.

- Do I need to inform the vehicle owner if I take out temporary insurance on their car?

- Yes, absolutely. You must have the vehicle owner's explicit permission to drive their car and to take out temporary insurance on it. While the policy covers you, it's a courtesy and a legal necessity to ensure they are aware and agreeable.

- Does temporary insurance affect the vehicle owner's no-claims discount?

- No, this is one of the key benefits. Since temporary car insurance is a standalone policy taken out in your name, any claim made on it will affect your own driving record and no-claims history (if you have one), but it will not impact the vehicle owner's separate annual policy or their no-claims discount.

If you want to read more articles similar to Temporary Car Insurance UK: Your Short-Term Cover, you can visit the Insurance category.