04/11/2024

In the fast-paced world of modern motoring, flexibility is key. Not every driving scenario demands a full year's commitment to an insurance policy. Sometimes, you just need cover for a few hours, a day, or a couple of weeks. This is where temporary car insurance, often referred to as short-term car insurance, truly shines. It's a convenient, pay-as-you-drive solution designed to meet those specific, transient needs without the financial burden or long-term ties of an annual policy. Whether you're borrowing a friend's car, test-driving a potential new purchase, or simply need to get a freshly acquired vehicle home, understanding how long this type of cover lasts and its myriad benefits is crucial for any responsible driver in the UK.

- How Long Does Temporary Car Insurance Last?

- Why Opt for Short-Term Car Insurance?

- How Does Short-Term Car Insurance Work?

- Key Considerations When Choosing Temporary Cover

- Temporary vs. Annual Car Insurance: A Quick Comparison

- Frequently Asked Questions (FAQs)

- Can I extend my temporary car insurance policy?

- What if I need cover for more than 28-30 days?

- Do I need to own the car to get temporary insurance?

- Is temporary insurance always fully comprehensive?

- What documents are required to get cover?

- Will taking out a temporary policy affect my main annual policy?

- Conclusion

How Long Does Temporary Car Insurance Last?

The primary appeal of temporary car insurance lies in its highly flexible duration. Unlike traditional annual policies, which typically lock you into a 12-month contract, short-term cover is designed to be precisely that – short term. The typical duration for temporary car insurance policies in the UK can range from as little as one hour up to a maximum of 28 to 30 days. This variability ensures that you only pay for the exact amount of cover you need, making it an incredibly cost-effective option for specific scenarios.

While some providers might offer cover for a full calendar month (30 or 31 days), the most common maximum period you'll encounter is 28 days. Once this period expires, your temporary insurance will cease, and you will no longer be legally permitted to drive the vehicle on public roads. It's absolutely vital to be aware of your policy's end date to avoid inadvertently driving uninsured, which carries severe penalties, including fines, points on your licence, and even vehicle impoundment.

The beauty of this short-term approach is that it caters to a wide array of situations where a full year's policy would be excessive or impractical. For instance, if you're helping a friend move house and need to drive their van for just a few hours, or if you're taking a new car for an extended test drive over a weekend, an hourly or daily policy is perfectly suited. For longer, but still temporary, needs – such as covering a vehicle while waiting for an annual policy to start, or if you're visiting family and need to share driving duties for a few weeks – the 28-day option provides ample protection.

Why Opt for Short-Term Car Insurance?

The benefits of temporary car insurance extend far beyond its flexible duration. It offers a unique blend of convenience, affordability, and peace of mind for drivers facing non-standard motoring situations. Here's a deeper look into why this type of cover is becoming increasingly popular:

Unmatched Flexibility and Convenience

Temporary policies are built around the concept of 'pay as you drive' or 'pay as you need'. This means you're not tied into a long-term commitment. You can arrange cover online quickly, often in just minutes, and receive your policy documents straight away via email. This instant access is invaluable when you need to get on the road without delay, whether it's an impromptu road trip or an urgent errand.

Cost-Effectiveness

Why pay for a full year of insurance when you only need cover for a day or a week? Temporary insurance allows you to only pay for the precise amount of time you require. This can lead to significant savings compared to the pro-rata cost of cancelling and re-starting an annual policy, or the risk of driving uninsured.

Protecting Your No-Claims Discount (NCD)

One of the most significant advantages of using a separate temporary policy is that it typically operates independently of your main annual car insurance. This means that if you need to make a claim on your temporary policy, it generally will not affect the hard-earned no-claims discount on your primary vehicle's insurance. This can save you a substantial amount on future premiums, making temporary cover a smart choice for borrowing cars or other short-term uses.

Ideal for Diverse Scenarios

Short-term car insurance is incredibly versatile, fitting a multitude of situations where annual cover isn't practical:

- Borrowing a Car: If you need to borrow a friend or family member's car for a day, a weekend, or even a few hours, a temporary policy covers you without impacting their insurance or NCD.

- Test Drives: When test-driving a car from a private seller, their insurance won't cover you. A temporary policy ensures you're legally insured for the drive.

- New Car Collection: Just bought a car and need to drive it home before your annual policy starts? A short-term policy provides immediate cover.

- Shared Driving: On a long road trip or holiday, if you're sharing driving duties, a temporary policy can cover the additional driver without adding them permanently to the main policy.

- Gap Cover: Sometimes there's a delay between selling your old car and insuring your new one, or between cancelling one annual policy and starting another. Temporary cover bridges this gap seamlessly.

- Learning to Drive: Some temporary policies are specifically designed for learner drivers practicing in a friend's or family member's car.

- Emergency Situations: If your own car breaks down and you need to use a different vehicle for a short period.

How Does Short-Term Car Insurance Work?

Getting temporary car insurance is designed to be a straightforward, hassle-free process. Most providers, such as MotorEasy, offer an entirely online application system that can be completed in just a few minutes. Here's a general overview of how it typically works:

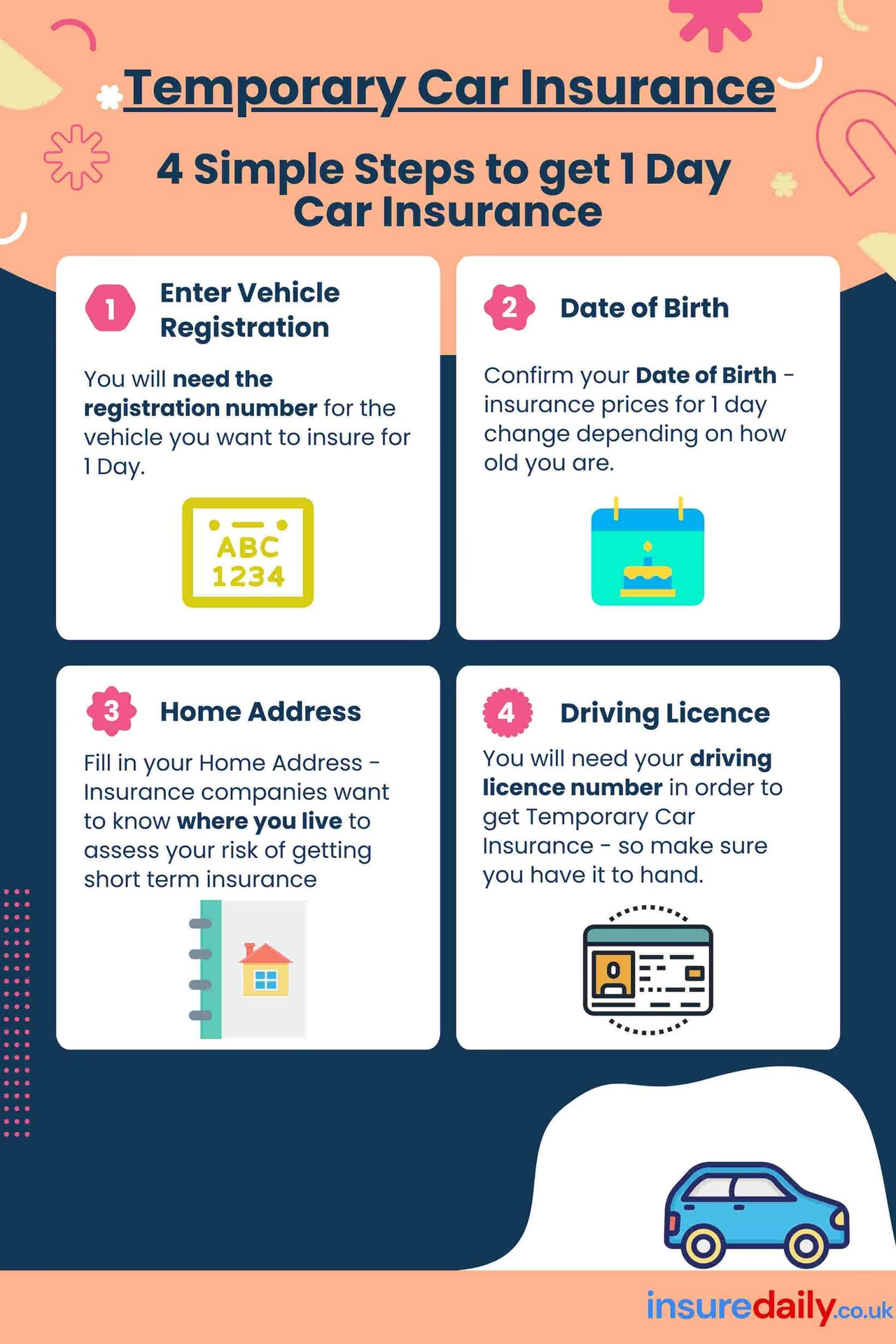

- Get a Quote: You'll enter details about yourself (age, driving history, address), the vehicle you wish to insure (registration number, make, model), and the exact duration you require cover for (e.g., 24 hours, 7 days, 28 days).

- Review Options: The system will provide you with a quote based on the information provided. Policies are usually comprehensive, offering the highest level of protection, though it's always wise to confirm the level of cover.

- Confirm Details: Once you're happy with the quote, you'll confirm your details and make payment.

- Instant Documents: Upon successful payment, your policy documents are typically emailed to you straight away. This means you can be insured and legally on the road within minutes of completing the process.

It's important to note that while the process is quick, you'll still need to meet certain eligibility criteria, which can vary by provider. Common criteria include minimum age requirements (often 18 or 19, sometimes higher for certain vehicles), maximum age limits, and a clean driving record (few or no penalty points, no serious convictions).

Key Considerations When Choosing Temporary Cover

While temporary car insurance offers unparalleled convenience, it's essential to consider a few key aspects to ensure you get the right policy for your needs:

- Eligibility Criteria: Always check the age limits and driving history requirements. Some insurers might not cover younger drivers or those with a history of claims or serious convictions.

- Vehicle Restrictions: While most standard cars are covered, some high-value, high-performance, or modified vehicles might not be eligible for temporary insurance. Vans are often covered, but again, specific restrictions may apply.

- Level of Cover: Most temporary policies offer fully comprehensive cover, which protects you, the vehicle you're driving, and any third parties involved in an accident. However, always verify this before purchasing.

- Excess: Be aware of the excess amount you would need to pay in the event of a claim. This is the first part of any claim that you are responsible for.

- Policy Exclusions: Read the terms and conditions carefully. Some policies might have specific exclusions, such as not covering business use, or not covering damage if the vehicle is left unattended for extended periods.

Temporary vs. Annual Car Insurance: A Quick Comparison

Understanding the fundamental differences between these two types of policies can help you make an informed decision:

| Feature | Temporary Car Insurance | Annual Car Insurance |

|---|---|---|

| Duration | 1 hour to 28-30 days | Typically 12 months |

| Cost Model | Pay-as-you-need; often daily/hourly rates | Fixed annual premium, paid upfront or monthly |

| Flexibility | High; instant, short-term cover | Low; long-term commitment |

| No-Claims Discount (NCD) Impact | Generally protects NCD on main policy | NCD can be affected by claims |

| Ideal Use | Borrowing, test drives, gap cover, shared trips, emergencies | Primary vehicle ownership, daily commuting |

| Cancellation | Expires automatically; no cancellation fees | May incur cancellation fees if ended early |

| Administration | Quick online process, instant documents | More detailed application, regular renewals |

Frequently Asked Questions (FAQs)

Can I extend my temporary car insurance policy?

Generally, temporary policies are designed for a fixed period and cannot be directly extended. If you need cover for longer than your initial policy, you would typically need to purchase a new temporary policy. It's crucial to do this before your existing cover expires to avoid any lapse in insurance.

What if I need cover for more than 28-30 days?

If your driving needs extend beyond the typical 28-30 day maximum for temporary insurance, it's usually more cost-effective and practical to consider an annual policy. While you could technically purchase consecutive temporary policies, this often becomes more expensive than a standard annual policy over a longer period. Some insurers might also have limits on how many consecutive temporary policies you can take out.

Do I need to own the car to get temporary insurance?

No, one of the main benefits of temporary car insurance is that it allows you to drive a vehicle you don't own. This makes it ideal for borrowing cars from friends or family, or for test-driving vehicles you're considering buying.

Is temporary insurance always fully comprehensive?

While many temporary car insurance policies offer fully comprehensive cover as standard, it's not universally guaranteed. Always check the policy details before purchasing to confirm the level of cover provided. Comprehensive cover is generally recommended as it offers the broadest protection.

What documents are required to get cover?

Typically, you'll need your driving licence details, vehicle registration number, and personal details (name, address, date of birth). The process is designed to be quick and paperless, with documents usually sent via email.

Will taking out a temporary policy affect my main annual policy?

One of the significant advantages is that temporary car insurance usually operates independently. This means that a claim made on a temporary policy should not affect the no-claims discount on your main annual car insurance policy. However, you should always inform your main insurer if you are driving another vehicle, especially if it's for an extended period, though this is primarily for their records and not usually a requirement for temporary cover itself.

Conclusion

Temporary car insurance is a modern, flexible, and highly practical solution for a multitude of short-term driving needs in the UK. From an hour to a full month, it provides tailored protection without the commitment or cost of an annual policy. It safeguards your no-claims discount, offers instant cover, and caters to specific situations like borrowing a vehicle or collecting a new purchase. By understanding its duration limits, benefits, and how it works, you can confidently choose the right cover for your momentary motoring adventures, ensuring you're always legally insured and driving with peace of mind.

If you want to read more articles similar to Temporary Car Insurance: Your Flexible Motoring Solution, you can visit the Insurance category.