22/12/2018

What is a Car Finance Agreement?

Purchasing a vehicle is a significant investment, and for many, it's not a purchase made outright. This is where a car finance agreement comes into play. Essentially, a car finance agreement is a contract between you and a lender (often a bank, credit union, or dealership's finance arm) that allows you to borrow money to buy a car. You then repay this borrowed amount, plus interest and any associated fees, over a set period, typically in monthly instalments. It's a common and accessible way to own a vehicle, but understanding the intricacies of these agreements is crucial to ensure you're getting the best deal and avoiding potential pitfalls.

Types of Car Finance Agreements

The world of car finance isn't a one-size-fits-all affair. Several types of agreements cater to different needs and financial situations. The most prevalent are:

1. Hire Purchase (HP) Agreements

Hire Purchase is a popular method, particularly in the UK. With an HP agreement, you'll typically pay an initial deposit, followed by fixed monthly payments over a period of 1 to 5 years. At the end of the term, you'll usually have a small 'option to purchase' fee to pay, after which you own the car outright. The car is technically 'hired' to you during the agreement, and you don't own it until the final payment is made.

2. Personal Contract Purchase (PCP) Agreements

PCP is another common choice, especially for those who like to change their car regularly. A PCP agreement works slightly differently. Your monthly payments are typically lower than with HP because they are based on the car's depreciation (the difference between its initial value and its predicted value at the end of the contract), rather than the full purchase price. At the end of the PCP term, you have three main options:

- Pay the Guaranteed Future Value (GFV): This is a lump sum amount, determined at the start of the contract, that you pay to own the car outright.

- Part-exchange the car: If the car's market value is higher than the GFV, you can use this equity as a deposit for a new car.

- Return the car: If you don't want to keep the car and haven't exceeded mileage or damage limits, you can simply hand it back to the finance company with nothing further to pay (subject to terms and conditions).

PCP can offer flexibility but requires careful consideration of mileage limits and condition requirements to avoid excess charges.

3. Personal Loans

You can also obtain a personal loan from a bank or building society and use the funds to purchase a car outright. In this scenario, the car isn't directly tied to the loan agreement as security. This gives you more freedom in choosing your car and lender, but loan terms and interest rates can vary significantly. You are the outright owner of the car from the moment of purchase.

Key Terms to Understand in a Car Finance Agreement

Before you sign on the dotted line, it's vital to grasp the key terminology used in these contracts:

| Term | Meaning |

|---|---|

| Principal Amount | The total amount of money you are borrowing to buy the car. |

| Interest Rate (APR) | The annual percentage rate charged by the lender. This is a crucial figure as it significantly impacts the total cost of your loan. Comparison is key here. |

| Loan Term | The duration of the agreement, usually expressed in months or years. A longer term often means lower monthly payments but a higher total interest cost. |

| Monthly Instalment | The fixed amount you pay to the lender each month. |

| Deposit | The initial sum of money you pay upfront, reducing the amount you need to borrow. A larger deposit can lead to lower monthly payments and a lower overall interest cost. |

| Guaranteed Future Value (GFV) | The pre-agreed value of the car at the end of a PCP agreement. |

| Option to Purchase Fee | A small fee paid at the end of an HP agreement to take full ownership of the car. |

| Mileage Allowance | The maximum number of miles you can drive per year under a PCP or lease agreement without incurring penalties. |

| Excess Mileage Charge | A fee charged for exceeding the agreed mileage allowance. |

| Early Repayment Clause | Details on whether and how you can repay the loan early, and any associated fees. |

What to Consider Before Signing

Securing car finance is a significant commitment. Here are some essential factors to weigh up:

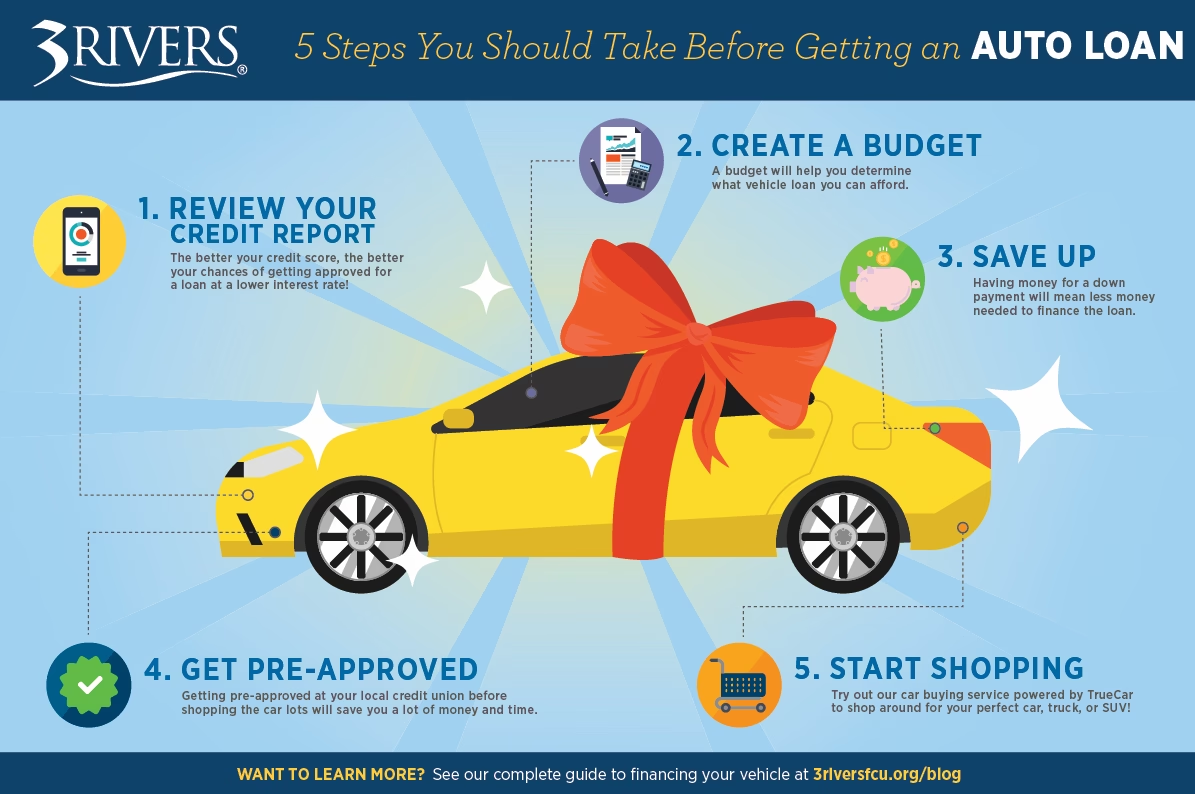

- Your Budget: Be realistic about what you can afford. Factor in not just the monthly payments but also insurance, road tax, fuel, and maintenance. Use an online car finance calculator to get a clearer picture.

- The Total Cost: Don't just focus on the monthly payment. Calculate the total amount you'll repay, including interest and fees, over the entire term. Compare the APRs offered by different lenders.

- Your Credit Score: Your credit history will heavily influence the interest rates you're offered. A good credit score generally means better terms. If your credit score isn't ideal, you might need to explore specialist lenders or consider a co-signer.

- The Contract Length: A longer contract means lower monthly payments but you'll pay more interest over time. A shorter contract means higher monthly payments but less interest overall.

- Mileage Restrictions (for PCP): If you opt for PCP, be honest about your annual mileage. Exceeding the limit can lead to significant charges.

- Car Condition and Mileage Limits (for PCP/HP): Understand the requirements for returning the car at the end of the contract, particularly regarding wear and tear and mileage.

- Early Repayment Options: Check if you can pay off the finance early without incurring hefty penalties, should your financial situation change.

- Read the Small Print: Always read the entire agreement carefully. If anything is unclear, ask for clarification from the lender. Don't feel pressured into signing.

Securing the Best Deal

To ensure you're getting the most favourable car finance deal, consider these steps:

- Shop Around: Don't accept the first offer you receive. Compare quotes from multiple lenders, including banks, credit unions, and dealership finance departments.

- Get a Quote Before Visiting the Dealership: Knowing your borrowing capacity beforehand gives you more negotiating power.

- Improve Your Credit Score: If possible, take steps to improve your credit score before applying for finance.

- Negotiate: Don't be afraid to negotiate on the interest rate or other terms, especially if you have a good credit history.

- Consider a Larger Deposit: A bigger upfront payment can reduce the amount you borrow and potentially secure a better interest rate.

Frequently Asked Questions

Can I get car finance with bad credit?

Yes, it's often possible to get car finance with bad credit, but you may face higher interest rates and stricter terms. Some lenders specialise in bad credit car finance. It's essential to research and compare options carefully.

What happens if I miss a payment?

Missing a payment can have serious consequences, including late fees, damage to your credit score, and in severe cases, the lender may repossess the vehicle. It's crucial to communicate with your lender immediately if you anticipate difficulty making a payment.

Can I pay off my car finance early?

Most car finance agreements allow for early repayment, but you should check the terms and conditions for any potential fees or penalties. You are generally entitled to a 'settlement figure' from the lender, which is the total amount you owe to clear the debt.

What is the difference between HP and PCP?

The main difference lies in ownership and how payments are calculated. With HP, your payments build towards outright ownership. With PCP, your payments are based on depreciation, and you have options at the end of the term, including returning the car without full ownership.

Is car finance the same as a car loan?

While often used interchangeably, a car finance agreement usually refers to specific contracts like HP and PCP where the car itself is often used as security. A personal loan for a car is a more general loan, where the car isn't necessarily tied to the loan as collateral.

In conclusion, a car finance agreement is a tool that can help you drive away in your desired vehicle. By understanding the different types of agreements, the key terms, and what to look out for, you can navigate the process with confidence and secure a deal that suits your financial circumstances. Always prioritise understanding the full cost and your obligations before committing.

If you want to read more articles similar to Understanding Car Finance Agreements, you can visit the Automotive category.