03/11/2024

Embarking on the journey to purchase a new car is an exciting prospect, often accompanied by the need to secure financing. While the allure of a shiny new vehicle is undeniable, understanding the financial avenues available is crucial to making a sound decision. This guide will delve into the world of car finance, exploring the different options, their pros and cons, and how to navigate the process to secure the most favourable terms. We will specifically address whether personal loans are indeed a cost-effective method for car acquisition, and touch upon the general landscape of auto loan rates, even as we acknowledge that specific rates from institutions like Security Service Federal Credit Union are not directly available at this moment due to technical display issues.

Personal Loans vs. Traditional Auto Loans

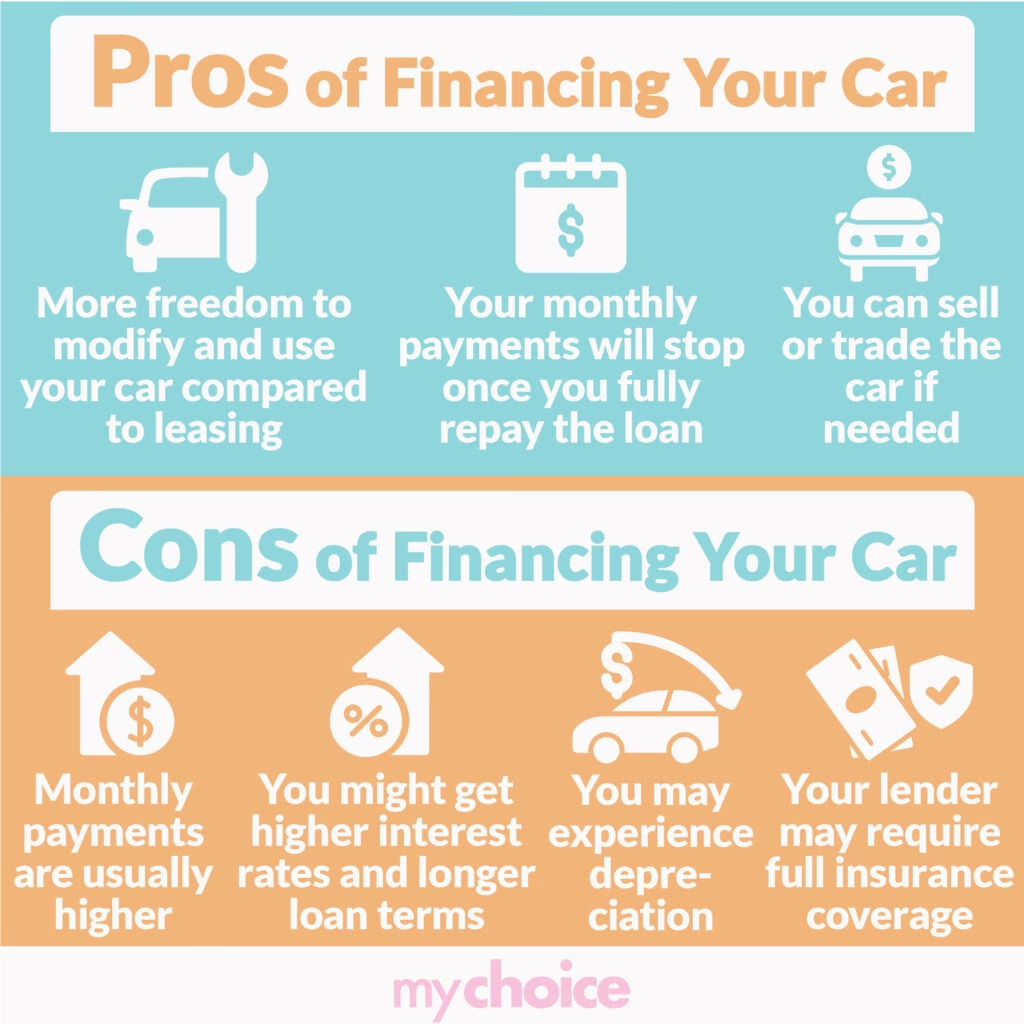

When considering how to fund your car purchase, two primary avenues typically emerge: personal loans and traditional auto loans. Both have their distinct characteristics, and understanding these differences is key to choosing the path that best suits your financial situation. Personal Loans: These are unsecured loans, meaning they are not backed by collateral. This often translates to potentially higher interest rates compared to secured loans. However, personal loans offer flexibility. The funds can be used for almost any purpose, including buying a car, and once disbursed, you can purchase the vehicle outright. The repayment terms are typically fixed, with a set monthly payment over a predetermined period. The recent observation that personal loan rates have doubled in the past two years, while concerning, still positions them as a potentially viable, albeit more expensive, option for car financing. Traditional Auto Loans: These loans are specifically designed for vehicle purchases and are secured by the car itself. This collateralisation generally allows lenders to offer lower interest rates than personal loans. The loan is tied directly to the vehicle, and if you default on payments, the lender has the right to repossess the car. Auto loans often come with longer repayment terms than personal loans, which can result in lower monthly payments but also mean paying more interest over the life of the loan. The interest rate is a critical factor in the overall cost of an auto loan.

Are Personal Loans the Cheapest Way to Buy a Car?

The question of whether personal loans are the cheapest way to buy a car is nuanced. As mentioned, personal loans generally carry higher interest rates than secured auto loans. However, the statement that they are "one of the cheapest ways to buy a car" suggests a specific context or a particular advantage that might be overlooked. This could be due to several factors: * Flexibility in Negotiation: Using a personal loan might give you more leverage when negotiating the price of the car with the dealership. You can approach the dealer as a "cash buyer," potentially securing a better deal on the vehicle itself, which could offset the higher interest rate of the personal loan. * Avoiding Dealership Financing Markups: Dealerships often act as intermediaries for auto loans, and they may add a markup to the interest rate offered by the lender. By securing a personal loan independently, you bypass this potential markup. * Specific Circumstances: For individuals with excellent credit scores and a strong financial history, a personal loan might be offered at a competitive rate that rivals or even undercuts some auto loan offers, especially if their credit history doesn't perfectly align with typical auto loan requirements. To determine the most cost-effective method, it's essential to compare the total cost of borrowing, which includes the interest paid over the loan's duration. This involves calculating: * The interest rate offered for the auto loan. * The interest rate offered for the personal loan. * The loan term for both options. * Any associated fees. Utilising a Loans Eligibility Calculator, as suggested, is a prudent step. These tools can help you estimate your borrowing capacity and potential interest rates based on your credit profile, allowing for a more informed comparison.

When you're looking to finance a car, understanding auto loan rates is paramount. These rates are influenced by a multitude of factors, primarily your creditworthiness. * Credit Score: This is arguably the most significant determinant of your auto loan interest rate. A higher credit score indicates a lower risk to the lender, typically resulting in lower interest rates. Conversely, a lower credit score will likely lead to higher rates. * Loan Term: Longer loan terms often come with higher interest rates because the lender is exposed to risk for a longer period. Shorter terms usually have lower rates but result in higher monthly payments. * Down Payment: A larger down payment reduces the amount you need to borrow, which can sometimes lead to a more favourable interest rate. It also signifies a lower loan-to-value (LTV) ratio, which lenders view favourably. * Vehicle Age and Type: New cars typically have lower interest rates than used cars, as they are generally considered less risky. The loan-to-value ratio on new cars is often more favourable for lenders. * Lender Type: Different lenders, including credit unions, banks, and online lenders, will offer varying rates based on their own operational costs and risk appetites.

Credit Unions as a Financing Option

Credit unions, like Security Service Federal Credit Union, are member-owned financial cooperatives. They often offer competitive rates and more personalised service compared to traditional banks. While we encountered a technical issue preventing us from displaying specific auto loan rates from Security Service Federal Credit Union, it is common for credit unions to provide: * Lower Interest Rates: Due to their non-profit status and member-centric approach, credit unions can often pass savings onto their members in the form of lower interest rates on loans. * Flexible Terms: They may offer more flexible repayment terms and loan structures to accommodate their members' needs. * Lower Fees: Credit unions are also known for having fewer and lower fees associated with their loan products. If you are a member or eligible to join a credit union, it is always advisable to explore their auto loan offerings. You can typically find information on their websites or by contacting their member services.

Key Considerations When Applying for a Loan

When you're ready to apply for a car loan, keep these essential points in mind: 1. Shop Around: Don't settle for the first offer you receive. Compare rates and terms from multiple lenders, including banks, credit unions, and online lenders. 2. Know Your Credit Score: Before you start applying, check your credit score. This will give you a realistic idea of the rates you can expect. 3. Get Pre-Approved: Obtaining pre-approval for an auto loan before visiting a dealership gives you a clear budget and strengthens your negotiation position. 4. Read the Fine Print: Understand all the terms and conditions of the loan, including any hidden fees or penalties for early repayment. 5. Consider the Total Cost: Look beyond the monthly payment. Calculate the total amount you will repay, including interest and fees, over the entire loan term.

Frequently Asked Questions

Q1: What is the best way to finance a car?A1: The "best" way depends on your individual financial situation. Generally, a traditional auto loan from a reputable lender, like a credit union or bank, often offers the most competitive rates because it is secured by the vehicle. However, if you can secure a personal loan with a very low interest rate and prefer the flexibility, or if it allows you to negotiate a better car price, it can also be a viable option. Always compare the total cost of borrowing. Q2: Can I get an auto loan with bad credit?A2: Yes, it is often possible to get an auto loan with bad credit, but you should expect higher interest rates and potentially shorter loan terms. Some lenders specialise in bad credit auto loans. You might also consider saving for a larger down payment or looking for a co-signer with good credit to improve your chances of approval and secure a better rate. Q3: How much car can I afford?A3: A common guideline is the 20/4/10 rule: make a down payment of at least 20%, finance the car for no more than 4 years, and ensure your total monthly vehicle expenses (loan payment, insurance, fuel) do not exceed 10% of your gross monthly income. Using a car affordability calculator can provide a more personalised estimate. Q4: What are the typical interest rates for auto loans?A4: Interest rates vary significantly based on credit score, loan term, and market conditions. For borrowers with excellent credit, rates can be as low as 3-5%. For those with average or below-average credit, rates can range from 7% to over 20%. It's crucial to check current rates from various lenders. Q5: Should I choose a fixed or variable interest rate for my car loan?A5: Fixed interest rates offer predictability, meaning your monthly payments will remain the same throughout the loan term. Variable rates may start lower but can increase over time if market interest rates rise, making your payments higher. For most car buyers, a fixed-rate loan provides greater peace of mind and budget stability. In conclusion, while the specific rates from Security Service Federal Credit Union were inaccessible at the time of this writing, the principles of securing automotive finance remain consistent. By understanding the differences between loan types, carefully evaluating interest rates and terms, and shopping around, you can make an informed decision that helps you drive away in your new car with financial confidence. Always prioritise comparing the overall cost of the loan to ensure you're getting the best deal possible.

If you want to read more articles similar to Securing Your Next Motor: A Guide, you can visit the Automotive category.