17/11/2018

Dreaming of a brand-new car but hesitant about the hefty upfront cost? You're not alone. For many drivers across the United Kingdom, the idea of paying a large sum for a new vehicle can be daunting. That's precisely why Personal Contract Purchase, or PCP, has become the most popular and often one of the most affordable ways to get a gleaming new car on your driveway. But what exactly is a PCP deal, and how does it truly work?

PCP offers a flexible and appealing alternative to traditional car ownership. Instead of buying the car outright or taking out a standard loan for the full value, a PCP agreement allows you to pay for the car's depreciation over a set period, usually through manageable monthly payments. It’s a finance solution that provides significant flexibility at the end of the term, giving you options that cater to your evolving needs. Let's delve deeper into the mechanics of PCP and explore why it's become such a cornerstone of car finance in the UK.

- Understanding Personal Contract Purchase (PCP)

- The Mechanics of a PCP Deal: What Influences the Cost?

- Unlocking the Best PCP Deals: Incentives and Grants

- PCP vs. Other Car Finance Options

- The Downsides of PCP: What to Watch Out For

- Making Your PCP Deal More Affordable

- Understanding the 'Balloon Payment' (Guaranteed Future Value - GFV)

- Who Truly Owns the Car During a PCP Agreement?

- Maintenance and Repairs: Your Responsibilities

- Frequently Asked Questions (FAQs) About PCP Car Finance

Understanding Personal Contract Purchase (PCP)

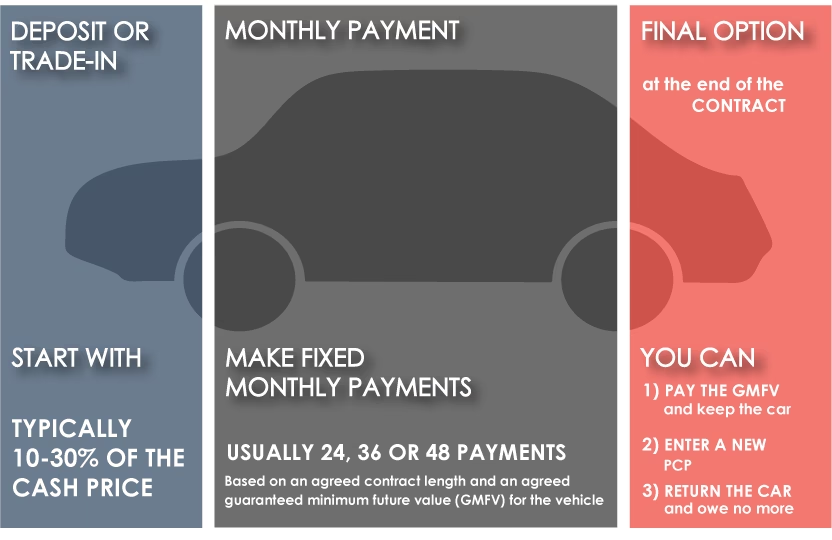

At its core, a Personal Contract Purchase is a type of car finance where you don't immediately own the car. Instead, you're essentially paying for the difference between the car's initial price and its predicted value at the end of the agreement. This predicted future value is known as the Guaranteed Future Value (GFV) or 'balloon payment'.

Here’s how it typically unfolds:

- Initial Deposit: You start by paying an upfront deposit. This can be a cash sum, the trade-in value of your current vehicle, or a combination of both. While there's no fixed amount, deposits are often around 10% of the car's value, though some deals may offer lower or even zero-deposit options.

- Monthly Payments: Over a set period, typically between two and five years, you make fixed monthly payments. These payments cover the cost of the car's depreciation during that time, plus interest. Because you're not paying off the full value of the car, these monthly instalments are generally lower than those for a Hire Purchase (HP) agreement for a car of similar value.

- End of Agreement Options: This is where PCP truly shines in terms of flexibility. When your contract term ends, you have three distinct choices:

- Return the Car: If you no longer need the car or want to avoid further payments, you can simply hand it back to the finance company. Provided the car is in good condition (within fair wear and tear guidelines) and you haven't exceeded your agreed mileage limit, there will be nothing more to pay.

- Buy the Car: If you've fallen in love with the car and wish to keep it, you can pay the outstanding Guaranteed Future Value (GFV). Once this final payment is made, ownership of the vehicle transfers to you.

- Part-Exchange for a New Car: This is a popular option for many. You can use any equity built up in the car (if its market value is higher than the GFV) as a deposit towards a brand-new PCP deal on a different vehicle. This allows you to drive a new car every few years without the hassle of selling your old one.

The Mechanics of a PCP Deal: What Influences the Cost?

Several critical factors determine the size of your monthly PCP payments. Understanding these can help you tailor a deal to your budget and needs:

- Cost of the Car: Naturally, a more expensive car will lead to higher monthly payments, as the depreciation amount will be greater.

- Length of the Agreement: A longer PCP term (e.g., five years instead of three) will spread the depreciation cost over more months, resulting in lower individual monthly payments. However, you'll pay interest for a longer period, which could mean a higher total cost over the entire agreement.

- Annual Mileage Allowance: This is a crucial aspect of PCP. When you sign the agreement, you'll commit to an annual mileage limit (e.g., 6,000, 10,000, or 15,000 miles per year). The lower the mileage allowance, the lower your monthly payments, as less mileage generally means less depreciation. Exceeding this limit can result in significant per-mile charges at the end of the contract, so be realistic about your driving habits.

- Guaranteed Future Value (GFV): The higher the GFV, the lower the amount of depreciation you need to cover, and thus, the lower your monthly payments. Cars that hold their value well tend to have more attractive PCP deals.

- Interest Rate (APR): The Annual Percentage Rate (APR) is the cost of borrowing money. A lower APR means less interest added to your payments. Your credit rating plays a significant role here; a lower credit score can lead to higher interest rates.

Unlocking the Best PCP Deals: Incentives and Grants

The popularity of PCP deals means car manufacturers and dealerships frequently offer attractive incentives to draw in customers. Keeping an eye out for these can significantly reduce your costs:

- 0% APR Deals: These are highly sought after as they mean you pay no interest on the financed amount. While they might require a higher deposit or be limited to specific models or terms, they represent excellent value. Many manufacturers, such as Fiat, Mazda, MG, and Tesla, have offered 0% APR on various models.

- Zero Deposit Deals: As the name suggests, these allow you to start a PCP agreement without an upfront deposit. While appealing, remember that monthly payments will likely be higher to compensate.

- Deposit Contributions: Manufacturers often contribute a sum of money towards your initial deposit, effectively reducing the amount you need to pay upfront or lowering your monthly payments. These can range from hundreds to thousands of pounds, making certain deals incredibly competitive. For instance, Audi, BMW, and Ford frequently offer substantial deposit contributions on popular models.

- Electric Car Grants and Incentives: With the UK's push towards electric vehicles (EVs), the government's Electric Car Grant provides a maximum of £3,750 off the On-The-Road (OTR) price for eligible new EVs costing £37,000 or less. Even if a car doesn't officially qualify, many carmakers, including Hyundai, Leapmotor, Skywell, and Volvo, offer their own equivalent "grants" or discounts to make EVs more accessible. These can significantly reduce the cost of transitioning to an electric car.

PCP vs. Other Car Finance Options

While PCP is popular, it's essential to understand how it compares to other common car finance methods to ensure you choose the right option for your circumstances.

| Feature | Personal Contract Purchase (PCP) | Hire Purchase (HP) | Personal Contract Hire (PCH) / Lease |

|---|---|---|---|

| Ownership | Option to own at end (after GFV payment). | Owns car automatically after final payment. | Never own the car; it's a long-term rental. |

| Monthly Payments | Lower, as you only pay for depreciation. | Higher, as you pay off the full car value. | Similar to PCP, covers depreciation. |

| Deposit | Required (typically 10%), but flexible. | Required (often higher than PCP). | Required (initial rental, typically 3-9 months' payments). |

| End of Term Options | Return, buy, or part-exchange for new. | Own the car. | Return the car. |

| Mileage Limits | Strict limits, excess charges apply. | No mileage limits (you own it). | Strict limits, excess charges apply. |

| Flexibility | High flexibility at end of term. | Geared towards ownership. | No ownership option, simple return. |

| Maintenance | Typically your responsibility. | Your responsibility. | Can be included in contract (servicing, tyres). |

The Downsides of PCP: What to Watch Out For

While PCP offers significant advantages, it's crucial to be aware of its potential drawbacks:

- No Automatic Ownership: Unlike Hire Purchase, you don't own the car until you make that final, often substantial, balloon payment. If you're set on owning the car, ensure you budget for this future lump sum.

- Mileage Penalties: Exceeding your agreed annual mileage limit can incur hefty charges per mile. Be accurate when estimating your yearly driving.

- Wear and Tear Charges: The car must be returned in a condition consistent with "fair wear and tear." Damage beyond this, such as significant dents, scratches, or interior damage, will result in additional charges. It's vital to review the fair wear and tear guidelines provided by your finance company.

- Higher Interest Rates for Lower Credit Scores: If you have a poor credit history, you might be offered a PCP deal with a much higher Annual Percentage Rate (APR), significantly increasing the total cost of the agreement.

- Early Termination Costs: Deciding to end your PCP agreement early can be expensive. You'll typically be liable for a significant portion of the remaining payments or a settlement figure, which can be a substantial outlay.

Making Your PCP Deal More Affordable

If you're looking to keep your monthly payments as low as possible, consider these strategies:

- Increase Your Deposit: The more you pay upfront, the less you need to finance, directly reducing your monthly payments.

- Look for Deposit Contributions: As mentioned, manufacturers often offer these. A £1,000 or £2,000 contribution can significantly impact your payments.

- Opt for a Longer Term: Spreading the cost over 4 or 5 years instead of 2 or 3 will lower monthly payments, but remember you'll pay interest for longer.

- Choose a Realistic Mileage Allowance: Be honest about how many miles you drive. While a lower mileage allowance means lower payments, the penalties for exceeding it can quickly negate any savings.

- Select a Car with Strong Residual Value: Cars that are known to hold their value well will have a higher GFV, meaning less depreciation for you to cover monthly. Research models that perform well in the used car market.

- Improve Your Credit Score: A better credit rating will qualify you for lower APRs, reducing the overall cost of your finance.

Understanding the 'Balloon Payment' (Guaranteed Future Value - GFV)

The Guaranteed Future Value (GFV), often referred to as the balloon payment, is a cornerstone of PCP finance. It's the estimated future value of the car at the end of your contract term, as agreed upon at the very start of your deal. This amount is guaranteed by the finance company, which protects you if the car's actual market value turns out to be lower than predicted.

The GFV is calculated based on several factors:

- Make and Model: Popular models with high demand tend to retain their value better.

- Length of the Agreement: The longer the term, the more the car is expected to depreciate, leading to a lower GFV.

- Agreed Annual Mileage: Higher mileage will lead to greater depreciation and thus a lower GFV.

- Market Conditions: While the GFV is guaranteed, general market trends for used cars are taken into account during its initial calculation.

It's crucial to understand this figure when you sign your PCP agreement, especially if you intend to buy the car at the end. Budgeting for this lump sum from the outset is essential to avoid disappointment if you can't afford it when the time comes.

Who Truly Owns the Car During a PCP Agreement?

This is a common point of confusion. For the entire duration of your Personal Contract Purchase agreement, the car is legally owned by the finance company. Even though you've paid a deposit and are making regular monthly payments, you do not hold the title to the vehicle. You are essentially leasing it with an option to purchase.

Ownership only transfers to you if, at the end of the agreement, you choose to pay the final balloon payment (GFV). Until that point, the finance company retains ownership. This is why mileage limits and fair wear and tear clauses are so important – you're using their asset.

Often, PCP deals are provided by the financial services arms of major car manufacturers (e.g., Ford Credit for a Ford, Volkswagen Financial Services for a VW). So, if you're driving a new car on PCP, it's likely that specific finance entity that owns your vehicle until you complete all payments.

Maintenance and Repairs: Your Responsibilities

When you enter into a PCP agreement, it's generally your responsibility as the driver to maintain the vehicle. This includes:

- Insurance: You must arrange and pay for comprehensive car insurance for the duration of the agreement.

- Regular Servicing: Adhering to the manufacturer's recommended service schedule is vital. Some PCP agreements might even specify that servicing must be carried out by an approved dealer or garage. Check your contract carefully. Some dealerships offer service packages that bundle the first few services into your monthly payments or as an upfront cost.

- Wear and Tear Items: Consumable items like tyres, brake pads, and wiper blades are your responsibility to replace as needed.

- Accident Damage: Any damage resulting from an accident would typically be covered by your car insurance. It's crucial to inform your PCP provider of any significant damage or repairs, as unauthorised work could affect the car's value and lead to charges when you return it.

The manufacturer's warranty will usually cover any mechanical faults that develop during the agreement period, providing peace of mind. However, always clarify the specifics of what's covered in your particular contract.

Frequently Asked Questions (FAQs) About PCP Car Finance

What is the cheapest car on a PCP deal in the UK?

Identifying the absolute "cheapest" car on a PCP deal is difficult as offers constantly change and depend on various factors like deposit, term, and mileage. However, smaller, more affordable models from brands like Dacia, Suzuki, MG, and Leapmotor often feature some of the lowest monthly payments, especially when paired with strong manufacturer deposit contributions or 0% APR deals. It's always best to compare current offers from multiple manufacturers and dealerships.

Should I buy a car from a PCP dealer?

PCP deals are predominantly offered by franchised car dealers and their associated finance companies. Buying from a PCP dealer means you're accessing the specific finance products and incentives (like 0% APR or large deposit contributions) directly from the manufacturer's network. This can often lead to better deals than trying to arrange third-party finance. It's advisable to compare these offers with independent finance providers, but for the best manufacturer incentives, a franchised dealer is usually the place to go.

How does the government Electric Car Grant work?

The UK Electric Car Grant is a government initiative designed to make new electric vehicles more affordable. It provides a discount of up to £3,750 off the On-The-Road (OTR) price of eligible new electric cars. To qualify, models must cost £37,000 or less and meet specific criteria. While the official grant applies to certain models, many carmakers now offer their own equivalent "EV grants" or enhanced deposit contributions to effectively provide a similar discount, even if the model doesn't officially qualify for the government scheme. This helps encourage the switch to electric driving.

How is the final payment to own the car calculated?

The final payment, known as the Guaranteed Future Value (GFV) or balloon payment, is pre-calculated and agreed upon at the start of your PCP contract. It represents the car's predicted residual value at the end of your term. Factors influencing this calculation include the car's make and model, how well it's expected to hold its value (its depreciation), the length of your finance agreement, and your agreed annual mileage allowance. This figure is fixed, providing certainty if you plan to buy the car.

Who pays for repairs on a car financed with PCP?

Generally, you, the driver, are responsible for the ongoing maintenance and repair costs of a car financed with PCP. This includes routine servicing, replacing wear-and-tear items like tyres and brakes, and paying for comprehensive insurance. If the car develops a mechanical fault, it would typically be covered by the manufacturer's warranty. Accident damage falls under your insurance policy. It's crucial to adhere to service schedules and address any damage promptly to avoid additional charges when returning the vehicle.

In conclusion, Personal Contract Purchase offers a compelling and flexible route to driving a new car, providing lower monthly payments compared to outright purchase or Hire Purchase, and a clear set of options at the end of the term. By understanding its mechanisms, being mindful of mileage and condition clauses, and actively seeking out the best deals and incentives, you can make PCP work effectively for your automotive needs in the UK. Always read the fine print and ensure the agreement aligns with your long-term plans.

If you want to read more articles similar to Your Definitive Guide to UK PCP Car Finance, you can visit the Automotive category.