12/12/2025

Right, listen up, because buying a gaff, whether it's a terraced house in Kuala Lumpur or a bungalow near the coast, is a massive undertaking. It's exhilarating, no doubt, a real milestone for many of us. But let's be honest, it can also feel like trying to fix a leaky engine with a blindfold on if you don't know your way around the financial bits and bobs. One of the biggest head-scratchers for folks looking to buy property in Malaysia often revolves around the legal fees and, more specifically, the stamp duty for the Memorandum of Transfer (MOT).

You see, it's not just about the down payment. There's a whole raft of associated costs that can, frankly, make your head spin if you're not prepared. We're talking lawyer fees, various disbursements, and that rather significant chunk of change known as stamp duty. Fear not, though, mate! This guide is here to strip away the jargon and lay out precisely what you need to know to budget effectively, ensuring your home-buying journey is more of a leisurely cruise than a white-knuckle ride.

- The Core Agreements: Your Property's Paperwork Trail

- Decoding the Costs: Legal Fees & Disbursements

- The Elephant in the Room: Stamp Duty for Memorandum of Transfer (MOT)

- Putting It All Together: A Typical Quotation Breakdown

- Navigating the Process: Tips for a Smoother Ride

- Frequently Asked Questions (FAQs)

- Conclusion

The Core Agreements: Your Property's Paperwork Trail

Before we dive into the nitty-gritty of costs, it's crucial to understand the foundational documents that underpin any property purchase in Malaysia. These are your main legal anchors, setting out the terms and conditions of your new abode.

The Sale and Purchase Agreement (SPA)

Think of the Sale and Purchase Agreement, or SPA, as the blueprint for your new home. This is the very first official document you'll sign, whether you're buying from an individual seller or a large property developer. It legally binds both the purchaser (that's you!) and the seller, outlining everything from the property's description and the agreed-upon price to the completion timelines and any specific conditions of the sale. It's absolutely vital to have this checked over thoroughly by a qualified solicitor before you put pen to paper.

Choosing Your Legal Eagle: A Crucial Decision

Now, when it comes to lawyers, you've got a bit of a choice, depending on who you're buying from:

- Buying from an Individual Seller: If you're acquiring a pre-owned property, you've got the freedom to pick your own lawyer. Our advice? It's often smarter and more efficient to appoint a law firm that's already on the panel of your chosen bank for the housing loan. Why? Because having the same firm handle both your SPA and your loan agreement streamlines communication and often speeds up the entire process. Bank panel lawyers also tend to be highly reputable, having met stringent criteria set by the financial institutions.

- Buying from a Developer: This is a slightly different kettle of fish. Developers often have their preferred panel of lawyers, and they might even offer incentives or rebates if you use their chosen firm. While you might feel a bit nudged, it's generally accepted practice here. Again, if you're taking out a loan, it's still wise to try and appoint the same lawyer for the loan agreement to keep things running smoothly.

The Loan Agreement: Your Financial Backbone

If you're like most of us and need a bit of financial backing to purchase your property, then the Loan Agreement comes into play. This is a separate legal contract between you and your bank, detailing the terms and conditions of your housing loan. It specifies the loan amount, interest rates, repayment schedule, and any collateral involved. Just like the SPA, this document requires careful review by your solicitor.

For cash buyers, it's a simpler affair; you'll only need to focus on the SPA, as there's no bank loan involved to complicate matters.

Decoding the Costs: Legal Fees & Disbursements

Beyond the property price itself, the first major category of expenses you'll encounter are the legal fees and associated disbursements. These are the charges for the professional services provided by your solicitor.

What Are Legal Fees?

Legal fees are essentially the charges for engaging legal assistance throughout the property purchase process. This covers a wide range of services, including:

- Drafting and reviewing the SPA.

- Drafting and reviewing the Loan Agreement (if applicable).

- Conducting necessary legal searches on the property (e.g., land title searches, bankruptcy searches).

- Advising you on your rights and obligations.

- Liaising with the seller's lawyers, the developer, and the bank.

- Preparing all necessary documentation for stamp duty assessment and property registration.

The legal fees for both the SPA and the Loan Agreement are typically calculated based on a tiered scale, often a percentage of the property's purchase price or the loan amount. While the exact rates can vary slightly between firms, they generally follow a standard guideline set by the Malaysian Bar Council.

Disbursement Fees: The Bits and Bobs

Alongside the solicitor's professional fee, you'll also see 'disbursement fees' on your quotation. These aren't fees for the lawyer's time, but rather out-of-pocket expenses that the lawyer incurs on your behalf to complete the transaction. Think of them as the administrative charges and official costs necessary to get the job done. Common disbursement fees include:

- Stamp duty for the SPA and Loan Agreement (separate from the MOT stamp duty).

- Registration fees for the transfer of ownership.

- Land search fees.

- Bankruptcy search fees.

- Printing and photocopying charges.

- Travel expenses (if applicable).

- Affirmation fees for statutory declarations.

- Valuation report fees (for the bank loan).

It's important to get a detailed breakdown of these disbursements from your lawyer so you know exactly what you're paying for.

Service Tax (SST)

And let's not forget the 8% SST, or Service Tax, on those legal fees – a standard bit of kit in Malaysia. This is applied to the professional legal fees, not the disbursements or stamp duty directly, but it's an important part of the overall cost calculation.

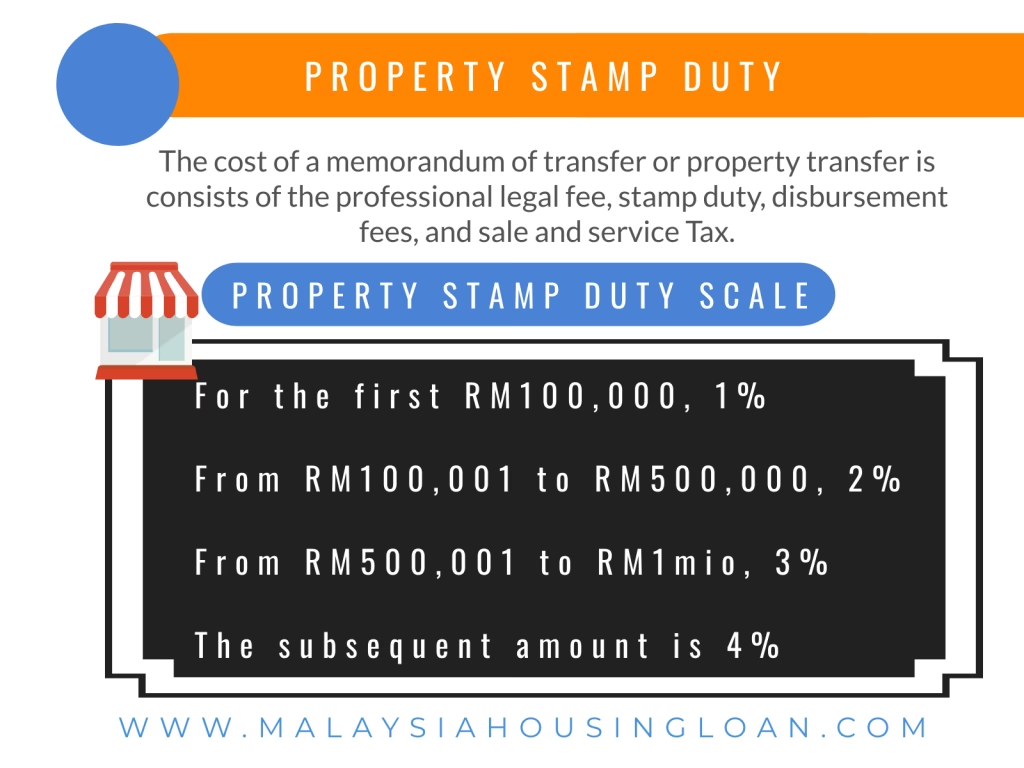

The Elephant in the Room: Stamp Duty for Memorandum of Transfer (MOT)

This is where a significant chunk of your budget will go, so pay close attention. The Memorandum of Transfer, or MOT, is the official document that legally transfers the ownership of the property from the seller to you. It's the final piece of the puzzle that makes you the rightful owner in the eyes of the law, and without it, you're not officially on the title.

This isn't just a bit of paperwork; it's a crucial step that comes with a significant cost attached: stamp duty. The stamp duty for the MOT is calculated based on the property's purchase price or market value (whichever is higher) and follows a tiered system. This means the percentage you pay decreases as the property value increases, up to a certain point.

Illustrative Stamp Duty Rates for Memorandum of Transfer (MOT)

Please note: The rates provided below are for illustrative purposes only and are subject to change by the Malaysian government. Always consult with your solicitor or the Inland Revenue Board of Malaysia (LHDN) for the most current and accurate figures.

| Property Value (RM) | Stamp Duty Rate |

|---|---|

| First RM100,000 | 1% |

| Next RM400,000 (RM100,001 to RM500,000) | 2% |

| Next RM500,000 (RM500,001 to RM1,000,000) | 3% |

| Above RM1,000,000 | 4% |

Let's do a quick example to show you how this works. Say you're buying a property for RM750,000:

- First RM100,000: RM100,000 x 1% = RM1,000

- Next RM400,000 (up to RM500,000): RM400,000 x 2% = RM8,000

- Remaining RM250,000 (from RM500,001 to RM750,000): RM250,000 x 3% = RM7,500

- Total Stamp Duty for MOT: RM1,000 + RM8,000 + RM7,500 = RM16,500

As you can see, this can be a hefty sum, making it one of the most significant upfront costs beyond your down payment. It's vital to factor this into your budget from the very beginning.

Stamp Duty for Loan Agreement

In addition to the MOT, your Loan Agreement also incurs stamp duty. This is typically a flat rate of 0.5% of the total loan amount. While less substantial than the MOT stamp duty, it's still another cost to account for.

Putting It All Together: A Typical Quotation Breakdown

When you receive a quotation from your lawyer, it will typically break down the costs into these main categories:

- Legal Fees (SPA): Based on the property purchase price.

- Legal Fees (Loan Agreement): Based on the loan amount.

- Disbursement Fees: A comprehensive list of all out-of-pocket expenses.

- Service Tax (SST): 8% applied to the legal fees.

- Stamp Duty (MOT): Calculated based on the tiered system for the property value.

- Stamp Duty (Loan Agreement): 0.5% of the loan amount.

By understanding each component, you'll be able to scrutinise the quotation effectively and ensure there are no surprises down the line. Always ask your lawyer to clarify anything you don't understand.

Buying a house is a big deal, and a little preparation goes a long way. Here are a few pointers to help you keep things on the straight and narrow:

- Budget Meticulously: Don't just focus on the property price. Account for the down payment, legal fees, stamp duty, valuation fees, and even potential renovation costs. Having a clear financial picture from the outset will save you a lot of stress.

- Choose Your Lawyer Wisely: A good, reputable solicitor is worth their weight in gold. They'll guide you through the complexities, protect your interests, and ensure all the paperwork is spot on. Don't simply go for the cheapest option; look for experience and reliability.

- Ask Questions: If something's unclear, ask! Your lawyer is there to explain things. There are no silly questions when it comes to such a significant investment.

- Don't Rush: Take your time to understand all the documents before signing. Once you've committed, it can be difficult and costly to back out.

Frequently Asked Questions (FAQs)

What exactly is the Memorandum of Transfer (MOT)?

The MOT is the legal document that officially records the change of ownership of a property. Once it's stamped and registered with the Land Office, the property's title is legally transferred from the seller to you, making you the new legal owner.

Are there any exemptions or rebates for stamp duty?

Yes, sometimes! The Malaysian government occasionally introduces stamp duty exemptions or rebates, especially for first-time homebuyers or for properties within certain price ranges. These schemes are typically announced during budget speeches. It's crucial to check with the Inland Revenue Board of Malaysia (LHDN) or your solicitor for any current incentives that might apply to your purchase. For instance, there have been schemes that offer full or partial exemptions for first-time buyers on properties up to a certain value.

Why is it better to use the bank's panel lawyer?

Using a lawyer from your bank's panel can significantly streamline the process. Since the lawyer is already familiar with the bank's procedures and requirements for loan documentation, it reduces the back-and-forth communication and potential delays that can occur when two different law firms are involved. This efficiency often translates to a faster loan disbursement and overall property transfer.

What are 'disbursements' on a legal bill?

Disbursements are the out-of-pocket expenses incurred by your lawyer on your behalf during the transaction. They are not part of the lawyer's professional fees but are necessary costs for things like land searches, bankruptcy searches, registration fees, printing, and various official charges that need to be paid to government bodies or third parties to complete the property transfer.

Does the stamp duty rate ever change?

Yes, the stamp duty rates are determined by the Malaysian government and can be revised during annual budget announcements or special policy changes. It's always important to confirm the current rates with your legal professional or the relevant government body at the time of your property purchase.

Is the 8% SST fixed on legal fees?

The Service Tax (SST) rate on legal services is set by the Malaysian government. While it has been 8% for some time, like any tax, it can be subject to change by legislative amendment. Your legal quotation will reflect the prevailing rate at the time of billing.

Conclusion

So, there you have it, a comprehensive look at the financial bits and bobs involved in buying a property in Malaysia, with a particular focus on that significant stamp duty for the Memorandum of Transfer. Understanding these costs upfront is half the battle won. It allows you to budget effectively, avoid nasty surprises, and approach your property purchase with confidence.

Remember, while the numbers might seem daunting at first glance, breaking them down into manageable chunks, much like servicing a car, makes the whole process far less intimidating. Arm yourself with this knowledge, work closely with a trusted solicitor, and you'll be well on your way to getting the keys to your new Malaysian home without any unexpected potholes on the road.

If you want to read more articles similar to Navigating Property Costs in Malaysia: MOT & More, you can visit the Automotive category.