18/07/2020

For many vehicle testing stations across the UK, the annual MOT test is a cornerstone of their business. However, despite its ubiquitous nature, the VAT treatment of MOT testing income remains a persistent source of confusion, leading to unnecessary stress and repeated scrutiny from HMRC. This article aims to demystify the rules surrounding MOT income, particularly its classification for VAT purposes, and provide clear guidance on how to report it correctly to avoid triggering those unwelcome inspection flags.

You’re not alone if you’ve found yourself caught between conflicting advice from HMRC inspectors and the automated systems that seem to have a mind of their own. The nuances of ‘outside the scope’ income, exempt supplies, and standard-rated services can create a challenging landscape for even the most diligent business owner. Let's delve into the specifics to ensure your garage's VAT affairs are as robust as the vehicles you inspect.

- Understanding MOT Testing and VAT in the UK

- The Nuances: 'Outside the Scope' vs. 'Exempt' vs. 'Standard Rated'

- HMRC's VAT Box Reporting – A Deep Dive into the Confusion

- Addressing Your Specific Queries

- 1. Is the inspector correct in suggesting out of scope VAT should be reported in Box 6?

- 2. If the inspector is not correct, how can my client and I make due representation to HMRC?

- 3. Is there a "notes" area on the HMRC computer which will show for my client when the "must inspect" flag is triggered?

- Recommendations for Garages with MOT Income

- Comparative Reporting Scenarios (Year 4 Example)

- Frequently Asked Questions (FAQs)

- Conclusion

Understanding MOT Testing and VAT in the UK

An MOT (Ministry of Transport) test is a mandatory annual inspection for most vehicles over three years old in the UK, ensuring they meet road safety and environmental standards. It is a statutory test, meaning it is required by law and is carried out by authorised testing stations on behalf of the Driver and Vehicle Standards Agency (DVSA), an executive agency of the Department for Transport. This statutory nature is absolutely crucial to its VAT treatment.

Unlike typical vehicle repairs, servicing, or the sale of parts, which are standard-rated for VAT (currently 20%), the income derived solely from conducting an MOT test is generally considered to be outside the scope of VAT. This means that no VAT is charged on the MOT fee itself, and it does not count towards your taxable turnover for VAT registration threshold purposes.

Why is it outside the scope? HMRC's long-standing position is that where a fee is charged by an approved body for a statutory test, and the primary purpose of that test is regulatory rather than the commercial supply of goods or services, then the fee falls outside the scope of VAT. The fee for an MOT test is fixed by law, and the service is primarily for public safety and regulatory compliance, not a commercial transaction in the traditional sense.

The Nuances: 'Outside the Scope' vs. 'Exempt' vs. 'Standard Rated'

To fully grasp the correct reporting for MOTs, it's essential to understand the distinctions between different types of supplies for VAT purposes:

Standard-Rated Supplies

These are the most common type of supply for most businesses. VAT is charged at the current standard rate (20%) on the selling price. Examples for a garage include vehicle servicing, repairs, parts sales, diagnostic work, and labour charges. You must account for this VAT to HMRC, and you can generally recover input VAT on related purchases.

Exempt Supplies

Exempt supplies are supplies of goods or services that are within the scope of VAT but are specifically exempt from it. No VAT is charged on these sales, and crucially, you generally cannot recover any input VAT on costs directly related to making these exempt supplies (unless partial exemption rules apply). While no VAT is charged, the value of exempt supplies *does* count towards your taxable turnover for VAT registration threshold purposes. A common example is rent from commercial property, as seen in your client's situation.

Outside the Scope (of VAT) Supplies

These are activities that are not considered to be a 'supply' for VAT purposes at all, according to UK VAT law. As such, no VAT is charged, and they do not count towards your taxable turnover for VAT registration. Since they are not supplies for VAT purposes, there's no question of input VAT recovery directly linked to them (though general overheads might still allow recovery if your business also makes taxable supplies). As established, MOT testing is the prime example for garages.

Here’s a comparative table to summarise these critical distinctions:

| Category | VAT Charged on Sale? | Counts Towards VAT Registration Threshold? | Input VAT Recovery on Related Costs? | Reporting in VAT Box 6? |

|---|---|---|---|---|

| Standard-Rated | Yes (20%) | Yes | Yes (subject to normal rules) | Yes |

| Exempt | No | Yes | Generally No (unless partial exemption applies) | Yes |

| Outside the Scope (e.g., MOTs) | No | No | Yes (if also making taxable supplies) | Generally No (specifically for MOTs as per HMRC guidance) |

HMRC's VAT Box Reporting – A Deep Dive into the Confusion

Your client's predicament highlights a common point of contention: how to correctly report these different types of income on the VAT return, particularly in Boxes 1 and 6.

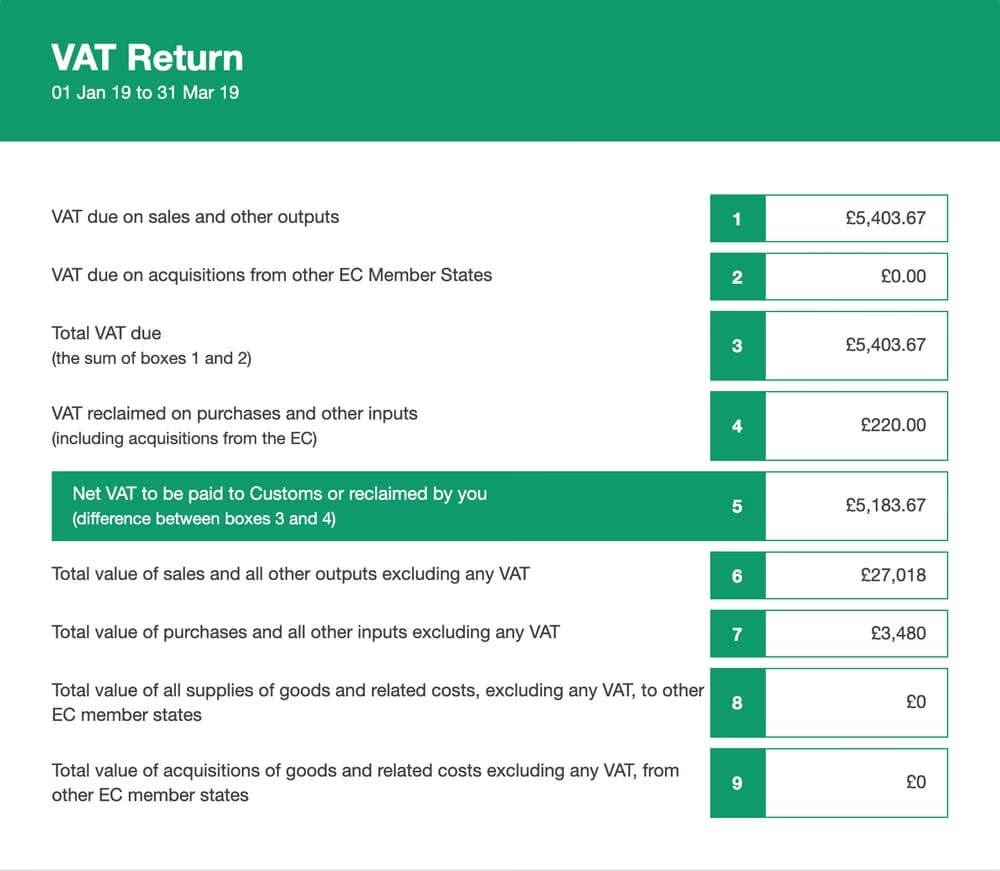

- Box 1: VAT due in this period on sales and other outputs. This box should contain the total VAT you owe to HMRC on all your standard-rated, reduced-rated, and zero-rated sales.

- Box 6: Total value of sales and other outputs excluding VAT. This box should reflect the total value of all your sales and other supplies, *excluding* any VAT. This includes standard-rated, zero-rated, and exempt supplies.

The core of the problem, as your client has experienced, arises when the value in Box 1 is not approximately 20% of the value in Box 6. HMRC’s automated systems are designed to flag such discrepancies, assuming that most businesses primarily deal with standard-rated supplies. However, businesses with significant exempt or outside the scope income will naturally show a lower Box 1 relative to Box 6, or even a Box 1 that seems disproportionately low if Box 6 is inflated by items that shouldn't be there.

Let's revisit the conflicting advice your client received:

- Inspection 2 (Exempt Income): The inspector recommended *not* reporting the £20K of exempt turnover (rent) in Box 6. This advice is generally incorrect. HMRC's official guidance (VAT Notice 700/12, section 3.5.5) explicitly states that the value of exempt supplies *should* be included in Box 6. Excluding it would understate your total output value.

- Inspection 3 (Exempt and Outside Scope Income): The inspector recommended *including both* the £20K exempt turnover and the £100K outside the scope MOT turnover in Box 6 with no VAT in Box 1. This advice is also problematic, specifically concerning the MOT income. While the exempt income should be in Box 6, the HMRC guidance specifically states that MOT tests should not be included in Box 6.

This is where the direct contradiction, and your client's stress, stems from. The definitive source for VAT reporting is VAT Notice 700/12, 'How to fill in and submit your VAT Return'. Section 3.5.5, which details what to include in Box 6, states:

“You must include: ... sales of goods and services that are exempt from VAT ...

Do not include: ... the value of MOT tests.”

This is a critical piece of information. Your client's MOT income, being outside the scope, should *not* be reported in Box 6 according to HMRC's published guidance. However, their exempt income (rent) *should* be included.

Addressing Your Specific Queries

1. Is the inspector correct in suggesting out of scope VAT should be reported in Box 6?

No, not for MOT tests. Based on the explicit instructions in VAT Notice 700/12, Section 3.5.5, the value of MOT tests should specifically *not* be included in Box 6. While some other forms of 'outside the scope' income (like certain non-business income or supplies made outside the UK) might be included in Box 6 depending on specific circumstances and how you calculate your VAT liability, for statutory MOT tests, the guidance is clear: exclude them.

Therefore, the advice from Inspector 3 to include the £100K MOT income in Box 6 is incorrect and, ironically, is likely to exacerbate the Box 1/Box 6 ratio issue that triggers the automated inspections.

2. If the inspector is not correct, how can my client and I make due representation to HMRC?

This is crucial. Your client should follow the official, published HMRC guidance. Here’s a recommended approach:

- Adhere strictly to VAT Notice 700/12: For future VAT returns, report the figures as follows:

- Box 1: VAT on standard-rated sales only.

- Box 6: Total of standard-rated sales *plus* exempt sales (e.g., rent). *Do not include the MOT income in Box 6.*

- Document Everything: Keep meticulous records of all communications with HMRC, including dates, names of inspectors, and the specific advice given.

- Formal Communication: If an inspection is triggered again, or if you wish to pre-emptively address the issue, write a formal letter or email to HMRC (or through your client's dedicated compliance officer if one exists). In this communication:

- Clearly state your client's business activities, differentiating between standard-rated, exempt, and outside the scope MOT income.

- Refer directly to VAT Notice 700/12, Section 3.5.5, explicitly quoting the part that states "Do not include: ... the value of MOT tests" in Box 6.

- Explain that your client is following this official guidance.

- Politely point out the conflicting advice received from previous inspectors (e.g., Inspector 2 regarding exempt income, Inspector 3 regarding MOT income).

- Request written confirmation from HMRC regarding the correct reporting methodology for MOT testing income in Box 6, specifically referencing your interpretation of Notice 700/12. This written confirmation will be invaluable for future reference.

- Professional Advice: Consider engaging a specialist VAT consultant. They can often communicate with HMRC on your behalf, citing specific legislation and guidance, and help to resolve such persistent issues more effectively.

By consistently following the correct published guidance and being prepared to defend it with clear documentation and references, you can demonstrate due diligence and hopefully resolve the recurring inspection cycle.

3. Is there a "notes" area on the HMRC computer which will show for my client when the "must inspect" flag is triggered?

Unfortunately, it is highly unlikely that there is a public-facing "notes" area on HMRC's computer system that would explain why a "must inspect" flag is triggered for your client, or that would allow you to input notes for their automated system. HMRC's internal systems for flagging and risk assessment are complex and proprietary. They are designed to identify anomalies based on algorithms, not necessarily to understand the specific nuances of every business model.

While an inspector might add notes to your client's record after an inspection, these are for internal use and do not typically alter the automated flagging system itself. The system will continue to compare Box 1 and Box 6 and flag discrepancies based on its programmed logic, regardless of prior inspection outcomes that found "no other issues."

The solution is not to try and 'game' the computer system by making Box 6 'fit' Box 1 (as Inspector 2 suggested), or by including items that shouldn't be there (as Inspector 3 suggested for MOTs). The solution is to report correctly according to the official guidance and then be prepared to clearly articulate and defend that correct reporting when an inspection inevitably occurs. The fact that previous inspections found no actual issues is a strong point in your client's favour, demonstrating that their underlying tax compliance is sound, even if the reporting triggers automated flags.

Recommendations for Garages with MOT Income

Given the recurring nature of these inspections, here are some practical recommendations for your client and other garages:

- Meticulous Record Keeping: Separate all income streams clearly. Ensure MOT income is distinct from repair work, servicing, and any other income (like rent). This makes it easier to justify your VAT return figures.

- Understand the Guidance: Regularly review HMRC guidance, especially VAT Notice 700/12, and any sector-specific notices. Tax rules can change, so staying informed is key.

- Proactive Communication: If your client anticipates a recurring flag due to their specific business model (high volume of outside the scope MOTs, significant exempt income), consider a proactive letter to HMRC, outlining their business model and how their VAT returns are prepared in accordance with official guidance. This might not stop the flags, but it prepares HMRC for what they will find.

- Internal Review: Regularly cross-check your VAT return figures against your underlying accounting records to ensure accuracy before submission.

- Don't Rely on Verbal Advice: Always seek written confirmation for any significant advice given by an HMRC inspector, especially if it contradicts published guidance or previous advice.

Comparative Reporting Scenarios (Year 4 Example)

Let's illustrate the financial figures provided for Year 4 (£60K Standard Rate, £20K Exempt, £100K MOTs) under different reporting scenarios, highlighting the impact on Box 1 and Box 6:

| Scenario | Standard Rate Sales | Exempt Sales (Rent) | Outside Scope (MOTs) | Box 1 (VAT Due) | Box 6 (Total Sales Ex-VAT) | Box 1 as % of Box 6 | HMRC Compliance (per 700/12) |

|---|---|---|---|---|---|---|---|

| 1. Inspector 2's Flawed Advice (Exclude exempt, 'make Box 6 fit Box 1') | £60,000 | £0 (excluded) | £0 (ignored) | £12,000 (£60k x 20%) | £60,000 | 20% | Incorrect (exempt should be in Box 6) |

| 2. Inspector 3's Flawed Advice (Include exempt & MOTs in Box 6) | £60,000 | £20,000 | £100,000 | £12,000 (£60k x 20%) | £180,000 (£60k+£20k+£100k) | 6.67% | Incorrect (MOTs should NOT be in Box 6) |

| 3. Correct Reporting (per VAT Notice 700/12) | £60,000 | £20,000 | £0 (excluded) | £12,000 (£60k x 20%) | £80,000 (£60k+£20k) | 15% | Correct |

As you can see from Scenario 3, even when correctly reported, Box 1 is 15% of Box 6, not 20%. This is the natural consequence of having significant exempt income and outside the scope income that correctly falls outside Box 6. The HMRC computer's algorithm, if solely looking for a 20% ratio, will flag this. However, this is the *correct* way to report, and your client should be prepared to explain this to HMRC.

Frequently Asked Questions (FAQs)

- Q: Do I charge VAT on MOT tests?

- A: No, the fee for an MOT test is generally considered outside the scope of VAT, so no VAT should be charged on it.

- Q: Should MOT income be included when calculating my business's taxable turnover for VAT registration?

- A: No, as MOT income is outside the scope of VAT, it does not count towards your taxable turnover for VAT registration threshold purposes.

- Q: Where do I report MOT income on my VAT return?

- A: According to VAT Notice 700/12, the value of MOT tests should specifically *not* be included in Box 6 (Total value of sales and other outputs excluding VAT). It is not reported in any box on the standard VAT return.

- Q: What if an HMRC inspector gives me advice that contradicts official guidance?

- A: Always prioritise official, published HMRC guidance. Politely point out the discrepancy, refer to the relevant notice (e.g., VAT Notice 700/12), and request clarification or confirmation in writing from HMRC. Do not simply follow verbal advice that contradicts published rules.

- Q: How can I minimise the risk of repeated HMRC inspections due to my MOT income?

- A: Ensure your accounting records are impeccable, clearly segregating all income types. File your VAT returns strictly according to published HMRC guidance. Be prepared to explain your methodology clearly and concisely, referencing official notices, should an inspection occur. Proactive communication with HMRC detailing your business model can also be beneficial.

Conclusion

The situation your client faces is a prime example of the challenges businesses encounter when automated systems meet complex tax rules. While the recurring inspections are undoubtedly frustrating and create unwarranted stress, the best defence is always accurate reporting based on official HMRC guidance. For MOT testing income, this means treating it as outside the scope of VAT and, crucially, *not* including its value in Box 6 of your VAT return.

By following the correct procedures, maintaining meticulous records, and being prepared to clearly articulate your compliance with VAT Notice 700/12, your client can navigate these challenges. While you may not be able to stop the automated flags entirely, you can ensure that each inspection confirms what you already know: your client's business is compliant, even if its unique income structure occasionally perplexes the HMRC computer.

If you want to read more articles similar to Navigating VAT on MOT Testing Income for UK Garages, you can visit the Automotive category.