12/02/2024

Running a successful motor trade business in the UK involves a multitude of responsibilities, from managing inventory and sales to ensuring the safety and well-being of your staff. One of the most frequently asked questions for business owners is whether their motor trade insurance policy adequately covers all their employees. It's a critical query, as misunderstanding your coverage can lead to significant financial penalties, legal complications, and a tarnished reputation. This comprehensive guide will delve into the nuances of motor trade insurance, specifically focusing on how it relates to employee coverage, helping you navigate the complexities and ensure your business is fully protected.

- Understanding Motor Trade Insurance

- The Crucial Role of Employers' Liability Insurance

- Beyond Employers' Liability: How Other Coverages Interact with Employee Protection

- Tailoring Your Policy to Your Workforce

- Consequences of Inadequate Employee Cover

- Comparative Table: Employee-Related Coverages

- Frequently Asked Questions (FAQs)

- Q: Is Employers' Liability always required, even for very small motor trade businesses?

- Q: What if I only have one employee? Do I still need EL insurance?

- Q: Are temporary staff or apprentices covered by my motor trade insurance?

- Q: Does my motor trade policy cover employees driving their own cars for business?

- Q: What happens if an employee is injured and I don't have Employers' Liability insurance?

- Q: How often should I review my motor trade insurance policy?

Understanding Motor Trade Insurance

Before we delve into employee coverage, it's essential to grasp the fundamental nature of motor trade insurance. Unlike standard car insurance, motor trade insurance is a specialised policy designed for businesses involved in buying, selling, repairing, servicing, or valeting vehicles. It's not a one-size-fits-all product; instead, it's a flexible suite of coverages tailored to the unique risks faced by motor traders.

Typically, motor trade policies combine several types of cover under one umbrella:

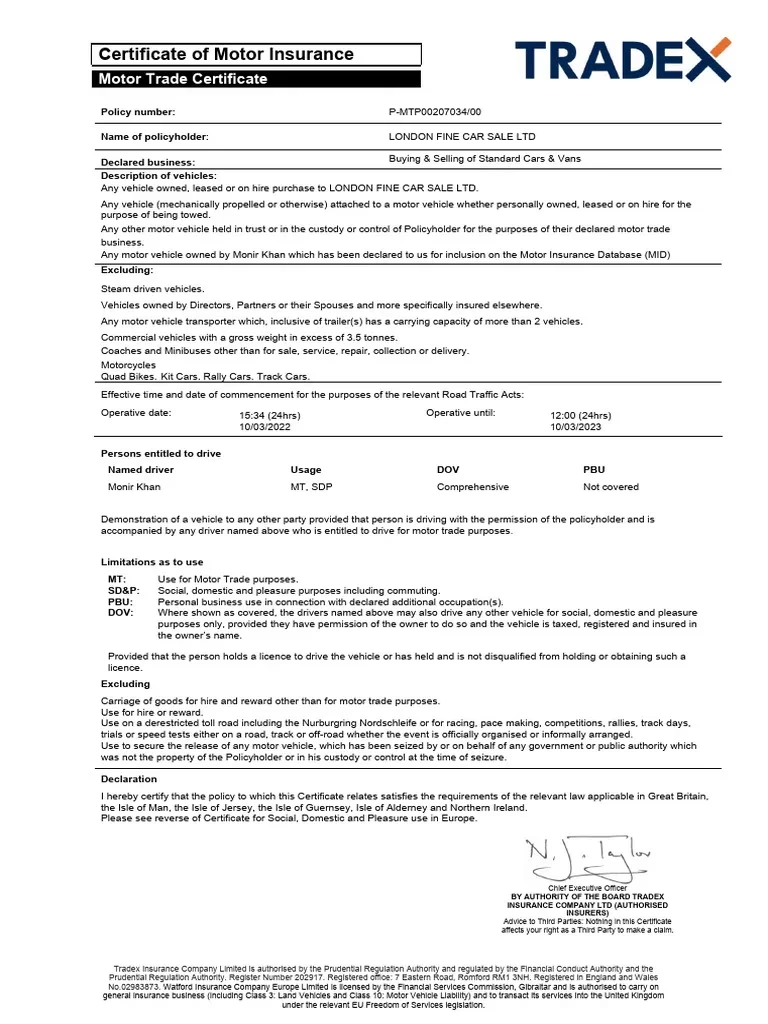

- Road Risk Insurance: This is often the core component, providing cover for vehicles being driven by the policyholder or named drivers (including employees) for business purposes. This could include test drives, vehicle collections and deliveries, or moving cars around a forecourt. It covers third-party liability, and often offers options for fire, theft, and accidental damage to the vehicles themselves.

- Combined/Premises Insurance: For businesses operating from a fixed location, this extends cover to the premises themselves. It can include protection for buildings, contents, tools, equipment, and stock vehicles against risks like fire, flood, and theft.

- Public Liability Insurance: This covers claims made by members of the public (non-employees) who suffer injury or property damage due to your business activities. For example, a customer slipping on a wet floor in your showroom or a stray tool damaging their car.

While these components are vital, they don't explicitly address the primary concern of employee protection in every scenario. This is where a specific type of insurance becomes paramount: Employers' Liability.

The Crucial Role of Employers' Liability Insurance

When it comes to covering your employees, the most critical piece of the puzzle is Employers' Liability (EL) insurance. In the UK, with very few exceptions, it is a legally required insurance for any business that employs one or more people. This isn't merely a recommendation; it's a statutory obligation under the Employers' Liability (Compulsory Insurance) Act 1969.

What Does Employers' Liability Cover?

Employers' Liability insurance protects your business against claims arising from employee injury or illness that occurs as a result of their work. If an employee suffers an injury or contracts an illness due to negligence on your part (e.g., unsafe working conditions, faulty equipment, inadequate training), EL insurance will cover the compensation costs and legal fees associated with that claim. This could range from a mechanic sustaining a back injury due to improper lifting techniques to an office worker developing carpal tunnel syndrome from an unergonomic workstation.

Who Counts as an 'Employee' for EL Purposes?

The definition of an 'employee' for Employers' Liability insurance is broader than you might initially think. It generally includes:

- Full-time and part-time staff

- Temporary staff and seasonal workers

- Apprentices and trainees

- Work experience students

- Volunteers working for your business

- Self-employed contractors who are working exclusively for you and under your direct supervision, effectively acting as an employee (though this can be a grey area and depends on the specific working relationship).

It's vital to understand that if someone is working for your business and you control their work, provide their equipment, and dictate their hours, they are likely considered an employee for EL purposes, regardless of their tax status (e.g., self-employed). This highlights the importance of due diligence in assessing all individuals working for your motor trade business.

Minimum Coverage and Penalties

The law requires you to have at least £5 million of EL cover, though most insurers provide £10 million as standard. Failure to have adequate Employers' Liability insurance can result in significant fines: up to £2,500 for every day you are not insured, and a further £1,000 fine if you do not display your EL certificate (which is also a legal requirement).

Beyond Employers' Liability: How Other Coverages Interact with Employee Protection

While EL is the cornerstone for employee injury/illness claims, other parts of your motor trade policy also contribute to a holistic approach to employee safety and business continuity.

Road Risk and Employees

If your employees drive vehicles as part of their job – be it test drives, vehicle movements, or collection/delivery services – your Road Risk insurance needs to cover them. This is typically achieved by adding them as 'named drivers' on the policy or opting for an 'any authorised driver' clause (though the latter often comes with age or experience restrictions). This ensures that if an employee causes an accident while driving a business vehicle, the insurance will cover third-party damages and potentially damage to the vehicle itself, depending on your chosen level of cover. It's crucial that any employee who drives for business purposes is properly covered under this section of your policy.

Public Liability vs. Employers' Liability

It's easy to confuse these two, but their distinction is crucial. Public Liability covers claims from *non-employees* (e.g., customers, visitors) who are injured or whose property is damaged due to your business operations. Employers' Liability specifically covers claims from *employees*. While both are vital for a motor trade business, they serve different purposes regarding who is protected.

Tools and Equipment Owned by Employees

Your combined or premises insurance will typically cover tools and equipment owned by the business. However, many mechanics and technicians own their own specialised tools. If these tools are essential for their work and are stored on your premises, you might be able to extend your business's tools and equipment cover to include them, or at least offer advice to your employees about their own personal tool insurance. This isn't directly employee 'coverage' in terms of injury, but it protects their means of earning a living, which contributes to overall staff welfare.

Personal Accident Cover

While not compulsory, some motor trade policies offer the option to add Personal Accident cover for the business owner or key employees. This provides a lump sum payment or weekly benefits in the event of specific injuries (e.g., loss of limb, sight) or temporary disablement, regardless of whether the business was at fault. This acts as an additional layer of financial peace of mind for the individual and their family, supplementing any EL claim process.

Tailoring Your Policy to Your Workforce

Given the varied nature of motor trade businesses, a 'one-size-fits-all' approach to insurance simply won't suffice. To ensure all your employees are adequately covered, you need a bespoke policy that reflects the specifics of your operation.

- Identify All 'Employees': Go beyond your formal payroll. Consider anyone who regularly performs work for your business under your direction, even if they are casual, temporary, or self-employed on paper.

- Assess Risks by Role: A mechanic faces different risks than an office administrator or a vehicle valeter. Discuss these varying risks with your insurer to ensure appropriate risk assessments and coverage are in place.

- Review Driving Needs: How many employees drive? What types of vehicles do they drive? How often? Ensure all drivers are named or covered under your Road Risk policy, meeting any age or claims history requirements.

- Communicate Changes: If you hire new staff, change roles, or expand your services (e.g., start offering mobile repairs), inform your insurer immediately. Your policy needs to evolve with your business.

Consequences of Inadequate Employee Cover

The ramifications of insufficient employee cover, particularly a lack of compulsory Employers' Liability insurance, can be severe:

- Hefty Fines: As mentioned, daily fines for not having EL insurance can quickly accumulate, becoming a significant financial burden.

- Legal Action and Compensation: If an employee is injured and you are found liable without EL insurance, your business will be directly responsible for all compensation payouts, legal fees, and medical costs. These can run into hundreds of thousands, or even millions, of pounds, potentially bankrupting your business.

- Reputational Damage: News of a business failing to protect its employees can severely damage its reputation, affecting customer trust, employee morale, and future recruitment efforts.

- Business Interruption: Dealing with major claims and legal battles can divert significant resources and attention away from running your core business, leading to operational inefficiencies and lost revenue.

| Coverage Type | Primary Purpose | Who Is Covered (Primarily) | Legal Requirement (UK) | Relevance to Motor Trade Employees |

|---|---|---|---|---|

| Employers' Liability | Covers claims from employees for work-related injury/illness. | All employees (broad definition). | Yes (Compulsory) | Essential for all motor trade businesses with staff. |

| Road Risk | Covers vehicles driven for business; third-party liability. | Policyholder, named drivers, authorised employees. | Yes (for driving activities) | Crucial for employees who drive customer vehicles or business vehicles. |

| Public Liability | Covers claims from the public (non-employees) for injury/damage. | Customers, visitors, general public. | No (Highly Recommended) | Protects against incidents involving customers or visitors on premises where employees work. |

| Tools & Equipment | Covers loss/damage to business tools and equipment. | Business assets; can sometimes extend to employee-owned tools. | No | Important for protecting the tools employees use to perform their jobs. |

| Personal Accident | Provides financial benefit for specific injuries/disability, regardless of fault. | Policyholder, named employees (optional). | No | An additional benefit for employees, offering financial security beyond EL. |

Frequently Asked Questions (FAQs)

Q: Is Employers' Liability always required, even for very small motor trade businesses?

A: Yes, with very few, highly specific exceptions (e.g., if you are the only employee and own 50% or more of the company, or if your employees are close family members in a non-limited company). For most motor trade businesses, if you have any employees, EL is a legal requirement.

Q: What if I only have one employee? Do I still need EL insurance?

A: Absolutely. The legal requirement applies from the moment you have your first employee, regardless of whether they are full-time, part-time, or temporary.

Q: Are temporary staff or apprentices covered by my motor trade insurance?

A: For Employers' Liability, yes, they are typically considered employees. For Road Risk, they would need to be specifically named on your policy or fall under an 'any authorised driver' clause, subject to the policy's terms and conditions.

Q: Does my motor trade policy cover employees driving their own cars for business?

A: Generally, your motor trade policy will only cover vehicles owned by the business or vehicles in your care, custody, or control (e.g., customer cars). If an employee uses their own vehicle for business purposes (e.g., running errands, visiting suppliers), their personal insurance policy must cover 'business use'. Your motor trade policy would not typically cover their personal vehicle in such a scenario, though Employers' Liability would still cover them for injuries sustained during their work.

Q: What happens if an employee is injured and I don't have Employers' Liability insurance?

A: You could face substantial fines from the Health and Safety Executive (HSE). More critically, if the employee makes a successful claim for compensation, your business would be personally liable for all legal costs, compensation payouts, and any associated damages, which could lead to severe financial distress or even bankruptcy.

Q: How often should I review my motor trade insurance policy?

A: You should review your policy at least annually upon renewal. However, it's also crucial to review it whenever there are significant changes to your business, such as hiring new staff, changing employee roles, expanding your services, acquiring new premises, or purchasing new equipment. Proactive communication with your insurer ensures continuous adequate coverage.

In conclusion, ensuring your motor trade insurance adequately covers all your employees is not just a matter of good business practice; it's a legal imperative in the UK. While Road Risk and Combined policies are vital for covering your vehicles and premises, Employers' Liability insurance is the non-negotiable cornerstone for protecting your staff and, by extension, your business, from the financial and legal fallout of workplace injuries or illnesses. Always conduct a thorough assessment of your workforce, understand the broad definition of 'employee' for insurance purposes, and work closely with a knowledgeable insurance broker to tailor a comprehensive policy that provides complete peace of mind for your motor trade operation.

If you want to read more articles similar to Motor Trade Insurance: Covering Your Employees?, you can visit the Insurance category.